Google's Gemini 3 has proven a big winner for GOOGL shares, but the company's vast AI infrastructure also benefits these three tech stocks..... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Dan Schmidt

After years of being considered a laggard in the AI gold rush, Alphabet Inc. (NASDAQ: GOOGL) turned the market on its head and put OpenAI on the defensive for the first time since ChatGPT launched in 2022. Alphabet is challenging OpenAI and shaking up the AI ecosystem—and if it continues to pull ahead in this race, it won’t just be GOOGL investors that benefit. Why Alphabet Has Dominated in 2025 It wasn’t long ago that Alphabet was in danger of falling behind the pack of AI hyperscalers. ChatGPT was going to replace Google Search, no one wanted autonomous vehicles, and the looming threat of regulatory scrutiny placed an invisible put option on the stock. But in 2025, the company delivered wins across all fronts: - Antitrust Lawsuit Resolved: In September, a judge’s ruling in the Department of Justice's antitrust case gave GOOGL stock a major boost. While Google must end exclusive search contracts, the judge ruled against breaking up the company. Crucially, Chrome and Android will remain under Alphabet, removing a key bear-case argument. Shares soared 9% on the day of the announcement.

- Gemini 3 Impresses: On Nov. 18, the company released Gemini 3, the most powerful and accurate version of its AI model to date. Not only did the model impress reviewers more than OpenAI’s latest model, but it was trained entirely on Google’s Tensor Processing Units (TPUs) rather than outsourced Graphics Processing Units (GPUs) from NVIDIA Corp. (NASDAQ: NVDA). We’ll discuss the significance of this development in a minute.

- Waymo Blows Away Competition: A recent opinion article in The NY Times highlights changing attitudes toward driverless cars. Waymo has long claimed its autonomous vehicles would become safer than human drivers, and it appears it now has data backing these claims. Additionally, the service is expanding to more cities, lapping competition from Tesla Inc.'s (NASDAQ: TSLA) RoboTaxi.

Investors have certainly taken notice—just look at GOOGL's outperformance relative to other stocks in the OpenAI universe, especially Oracle Corp. (NYSE: ORCL).

3 Stocks to Piggyback on Google’s Success Alphabet’s AI success doesn’t happen in a vacuum. Several public companies are deeply integrated into Google’s infrastructure—and as Gemini adoption grows, these suppliers could see breakout growth. Broadcom: Exclusive Chip Provider for Gemini You can’t discuss the success of Gemini without mentioning Broadcom Inc. (NASDAQ: AVGO), the semiconductor designer with the inside track to Google’s AI infrastructure. Above, we noted that Gemini was trained on the company’s own TPU chips rather than NVIDIA GPUs. TPUs are like stripped-down versions of GPUs, bare-bones chips without the ability to handle complex tasks like graphics rendering or crypto mining. The result is a less flexible, but more efficient chip, which is perfect for Gemini’s purposes. Where does Broadcom come in? Google can design the TPU, but it lacks the expertise (and patents) to build the physical chips. Broadcom is the exclusive partner helping Google oversee the fabrication process and earns revenue for each chip used in a Gemini data center. AVGO shares are up more than 60% year-to-date (YTD), and the company reported record revenue in its Q3 2025 earnings release and boosted its fiscal 2026 outlook despite weak revenue from non-AI sources. TTM Technologies: PCBs Designed for High-Density TPUs Ever crack your smartphone so badly you can see the little green board inside? That’s a printed circuit board (PCB), one of the primary components in any electrical device. PCBs can be programmed for a near-infinite array of tasks, but AI hyperscalers like Google require very dense, advanced boards specifically designed to handle the enormous heat that servers produce. TTM Technologies Inc. (NASDAQ: TTMI) is a leading manufacturer of advanced PCBs, and its unique designs can be customized to integrate Google’s TPU chips. Aggressive data center expansion has created strong demand for the company’s PCBs, and the stock has soared nearly 170% so far this year. But despite the parabolic gains, fundamental and technical trends point to further upside. The company’s backlog is approaching $1.5 billion, and management reiterated its $730 million to $770 million Q4 revenue guidance despite margin headwinds from opening a new facility in Malaysia. Celestica: Server Racks and Switches for Google Data Centers Finally, we have the hardware provider for Google’s AI infrastructure. “Picks and shovels” plays are often popular investments during sector-specific bull runs, but Celestica Inc. (NYSE: CLS) offers a more targeted solution. The company, which manufactures customized server racks and Ethernet switches, has become one of Google’s preferred hardware providers. Celestica assembles and ships the Trillium TPU racks used in Gemini data centers, and its relationship with the tech giant has sent the three-decade-old company’s shares to unprecedented heights (up over 220% YTD). Buying a stock already up 220% takes gumption, but the company's 2026 revenue guidance projections target $16 billion in sales, a 55% year-over-year increase from 2025. Celestica may still have room to grow if demand for AI infrastructure holds steady.  Read This Story Online Read This Story Online |  |

| Written by Thomas Hughes

As central as NVIDIA (NASDAQ: NVDA) is to the AI-driven semiconductor supercycle, it is not the only semiconductor stock set to benefit. While AI, GPUs, and data center capabilities are at the core of the movement, they are impacting various sectors across the economy and are complemented by steady industrial demands. The industrial chip market has been under pressure for years due to supply imbalances stemming from the COVID-19 pandemic and subsequent post-pandemic supply-chain disruptions. The story at the end of 2025 is that demand is improving and growing in critical markets, including telecom and automotive, with AI underpinning the long-term outlook. Advancing and evolving AI means the evolution of all things technological, a cycle that will play out over years, if not decades. A look at the Philadelphia Semiconductor Index (NASDAQ: SOXX) reveals a market in rally mode, poised to set new highs by the end of 2025. While the action is underpinned by NVIDIA’s consensus analysts' forecast for a 45% upside as of early December, it is not the only stock driving the action.

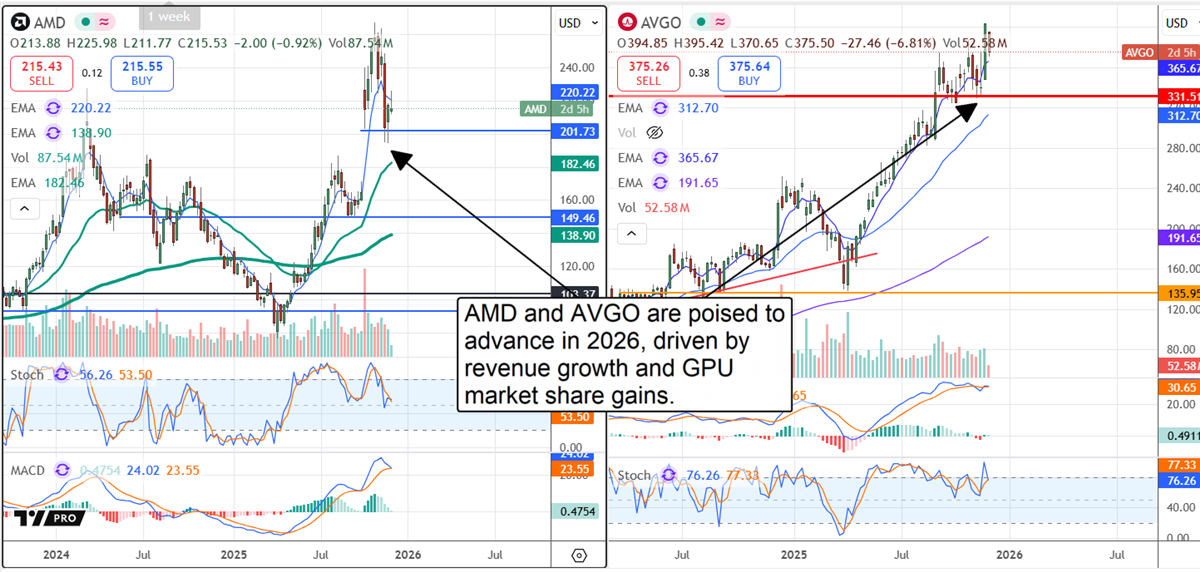

Broadcom and Advanced Micro Devices Are the Top 2 Semiconductor Stocks to Own in 2026 In fact, unlike the S&P 500 index, NVIDIA is only the third-largest holding, with Broadcom (NASDAQ: AVGO) and Advanced Micro Devices (NASDAQ: AMD) making up larger portions of the fund. This reflects the broader strength across the semiconductor sector, where AI-driven demand is fueling growth for multiple companies—not just NVIDIA. Both AVGO and AMD are well-positioned in the race to dominate GPU technologies, which are central to AI, data center expansion, and advanced computing workloads. Broadcom’s leadership in networking and custom silicon, paired with AMD’s progress in GPU and CPU architecture, supports analyst expectations for significant market share gains and revenue acceleration by 2026. While NVIDIA continues to draw headlines—including for its $2 billion investment in chip design innovation—these two companies also play foundational roles in building the infrastructure behind AI. Although AVGO and AMD currently lead the fund’s allocations, other semiconductor stocks are strategically aligned with the same long-term demand drivers. Several are well-positioned to benefit from continued AI adoption, industrial recovery, and expanding chip applications across telecom and automotive markets.

Top-Three Micron Technology’s Outlook Swells on Product Demand and Pricing Micron Technology (NASDAQ: MU) is critical to the AI industry because of its position in the HBM market. HBM, specifically HBM3 and the subsequent HBM4 architecture, is vital for AI and datacenter operations and in high demand. Each GPU, whether sold by NVIDIA, Broadcom, or Advanced Micro Devices, uses multiple stacks of HBM chipsets, making the market highly in demand. The takeaway in December is that demand is driving shortages that affect adjacent HMB markets, including automotive, telecom, and gaming/graphics, and prices are rising. The impact on Micron is accelerating growth and explosive margins, as evidenced by the fiscal Q4 release. Revenue growth accelerated sequentially by nearly 1,000 basis points to 46%, before the latest round of price increases took effect and is expected to remain strong. Analysts have been lifting their forecasts for calendar 2026 and now expect a 50% revenue growth and 100% earnings growth. Analysts have also been raising their stock price targets, pointing to another 50% upside for this market.

Fourth-Place Marvell Technology to Experience Material Strength for 2 Years Marvell Technology (NASDAQ: MRVL) affirmed its place in the AI ecosystem with its Q3 fiscal year 2026 earnings report. The report was better than expected and was compounded by robust guidance, spurring an equally strong response from the analysts. Not only were results underpinned by a solid 38% increase in the Datacenter-specific business, but its Networking and Communications businesses grew by much stronger amounts. The critical detail is the guidance, which expects robust growth to continue in the current quarter, and the cash flow it produces. Marvell puts its cash to good use, maintaining a fortress balance sheet, investing in growth, and returning capital to investors. Capital returns are substantial, but the token dividend is reliable, and share buybacks reduce the count quarterly. The Q3 activity reduced the share count by approximately 0.75% and is expected to continue in the upcoming quarters. Analysts are lifting their stock price targets following the release and point to a 30% to 40% upside at the high end.

Fifth-Place Analog Devices Growth Is Accelerating Analog Devices (NASDAQ: ADI) was among the first industrial semiconductor manufacturers to indicate the industry's bottom. That occurred earlier in calendar 2025 and has accelerated since. Revenue growth accelerated sequentially, and year-over-year (YOY) in fiscal Q4 2025, and the guidance for 2026 is strong. The company forecasts YOY growth to accelerate again in Q1 and may be cautious in its estimates. Other pertinent details include significant margin expansion, expectations for additional improvement, and cash flow, which supports dividends and share buybacks. Analog Devices' capital return is more substantial than Marvell's, although the upside potential, as indicated by analyst trends, is less. The dividend yields about 1.4% as of early December, and buyback activity reduced the count by more than 1% for the quarter.

Read This Story Online |  Trump's Next Export Ban Could Reshape the Global Economy

It's not semiconductors, AI chips or quantum computers. But none of those technologies can exist without it. On January 19th, 2026, Trump is expected to ban exports of something every tech company desperately needs—forcing them all to relocate to U.S. soil. See what he's about to ban here… |

| Written by Chris Markoch

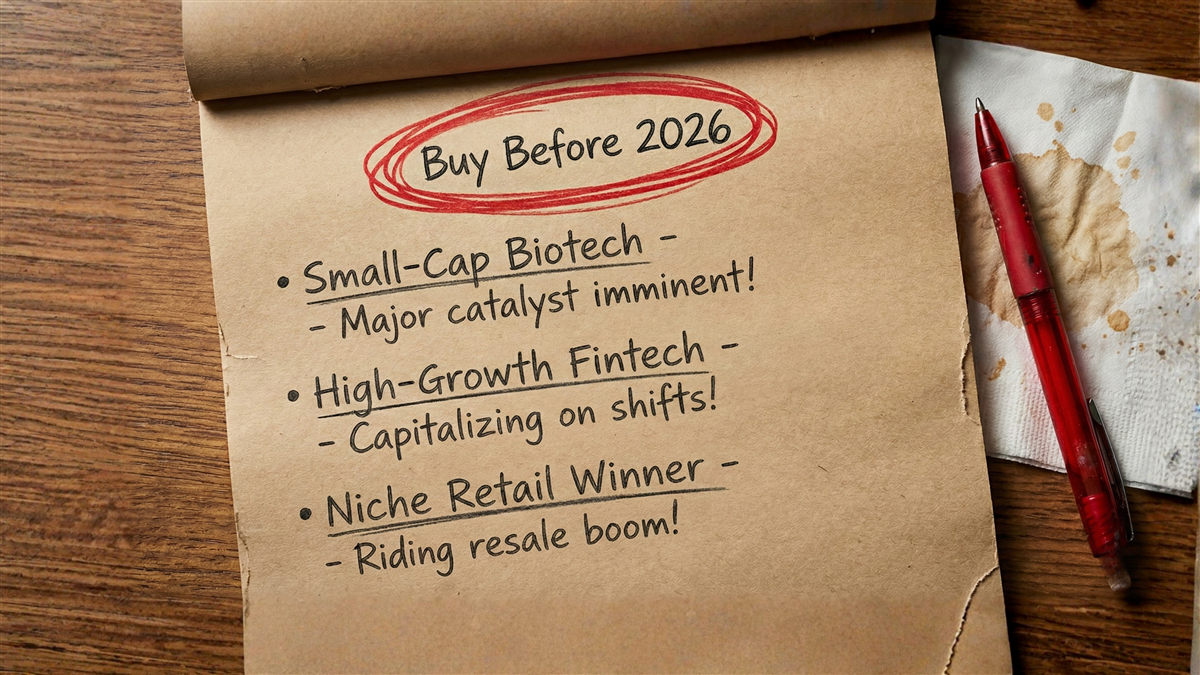

Many investors have profited from the artificial intelligence (AI) trade in 2025. But there have been several up-and-coming stocks in other sectors that have posted impressive gains this year. The three stocks in this article are still small stocks; the largest market cap is just over $4 billion. However, they’ve made strong moves and proven the idea that time in the market is better than trying to time the market. That said, if investors could see the future with absolute clarity, investing would be easy. Unfortunately, the future is rarely clear, and a bullish outcome is not inevitable. But the charts speak for themselves. Investors who bought these stocks and had the patience to hold them through some rough times are reaping the benefits today. Better still, the stocks may not be done moving higher. Biotech Breakthrough: A Small Cap With a Big 2026 FDA Catalyst Celcuity Inc. (NASDAQ: CELC) is a clinical-stage biotechnology company that recently delivered positive clinical data for its first-in-class PI3K/mTOR inhibitor that targets HR+/HER2 - metastatic breast cancer. The company’s pivotal Phase 3 VIKTORIA trial is underway, and there is a belief that the company could receive U.S. Food & Drug Administration (FDA) approval in 2026. Investors have been front-running those results, pushing CELC stock up over 660%, with almost the entirety of those gains occurring since the end of July. At $99.30 as of this writing, the stock is within 3% of its consensus price target. However, Jeffries raised its price target on the stock to $134 from $108 on Dec. 2. The biggest risk investors face is the financial cost of the commercialization phase. However, in its most recent earnings report, Celcuity showed a reinforced balance sheet with $455 million in cash, cash equivalents, and short-term investments. That was up about 72% year-over-year (YOY), and management believes that will be sufficient until the commercialization phase begins. Fintech Disruptor Turning Revenue Growth Into Real Momentum At a time when banks have less to offer many consumers, it’s easy to make the case for Dave Inc. (NASDAQ: DAVE). This is a Los Angeles-based financial technology (fintech) company known for its Dave app. The Dave app provides affordable, transparent financial tools that help its users, many of whom are living paycheck to paycheck, avoid overdraft fees, budget more effectively, and get access to short-term cash when needed. The company recently reported a 64% YOY increase in revenue and an 85% beat in adjusted earnings per share (EPS). DAVE stock is up 120% in 2025, and analysts believe it’s got much more room to move higher. As of this writing, the stock is trading at $208.24, and the consensus price target is $304.25. That’s an upside of more than 46%. Some investors could be getting nervous about the company’s forward price-to-earnings (P/E) ratio of around 119x. However, analysts are forecasting earnings growth of over 117% in the next 12 months. That kind of growth will easily allow for growth into that valuation. Resale Retail Winner Riding a Massive Consumer Shift It's been another rough year for consumer staples stocks, but ThreadUp Inc. (NASDAQ: TDUP) has been a notable exception. TDUP stock is up over 430% in 2025, and that’s despite a sell-off of over 29% in the three months ending Dec. 1. The company operates as an online consignment store, which makes it the right stock at a time when many consumer budgets continue to be stretched. The thrift and resale market was a $49 billion industry in 2024 and is expected to grow to $74 billion by 2029. TDUP stock is the smallest of the three stocks on this list, and short interest of over 17% means that traders are active. That said, the company’s Q3 earnings report showed strong YOY revenue growth and, more importantly, a record in new buyer acquisition and a 37% YOY increase in orders. Admittedly, this could be a short-term play. However, the younger generation that makes up ThredUp’s core market will likely feel pinched for some time, which is likely why analysts give TDUP stock a consensus price target of $12.50, representing a 68% gain from its closing price on Dec. 1. Read This Story Online |  |

| More Stories |

| |

|

|