From our partners at Paradigm Press Below is an important message from one of our highly valued sponsors. Please read it carefully as they have some special information to share with you.

The #1 AI Investment

Elon + Nvidia =

Dear Reader,

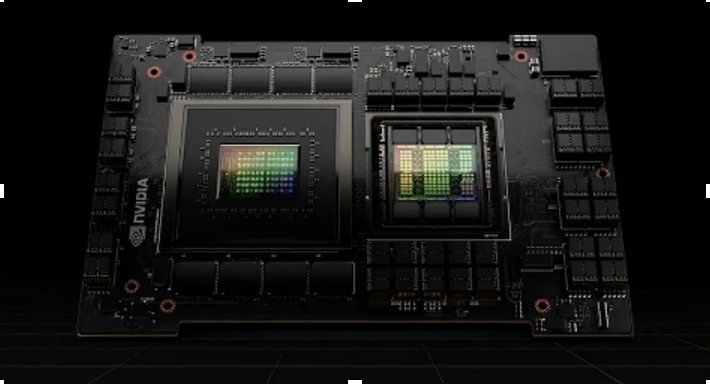

Do you see this weird looking device?

This is Nvidia’s holy grail.

It contains over 3 terabytes of memory…

80 billion transistors…

And can perform over 60 trillion calculations… per second.

This single computer chip goes for $25,000 a pop.

And now…

Elon Musk…

The world’s richest man…

Alongside Nvidia’s CEO Jensen Huang…

Are about to crank it up to 1 million.

At a remote facility in Memphis Tennessee…

You two of them have teamed up with an emerging tech titan…

To build the most advanced AI machine on the planet…

Powered by 1 million of these advanced AI chips.

This Will Unlock the TRUE Power of Artificial Intelligence!

But before you rush out to buy shares of Tesla or Nvidia…

There’s another investment you must consider.

You see, there is ONE company…

That Elon … and Nvidia…

And 98% of the Fortune 500…

Are ALL working with…

To prepare for AI 2.0.

Nvidia’s CEO has even said – this company is ESSENTIAL to their ongoing expansion.

>>>See how you can invest in this revolutionary company today.

Elon is expanding this project RAPIDLY…

And just announced a second AI computer…

That will need this company in order to build.

This may be the single greatest way to build wealth from the AI bull market.

But you must take action immediately.

AI is quickly becoming one of the MAIN focuses in Trump’s new administration…

And once Wall Street sees what this AI can really do — it will be too late.

>>>Go here to learn how to invest in Elon new AI venture.

Regards,

James Altucher

Editor, Paradigm Press

Additional Reading from MarketBeat Abbott Laboratories' October Price Plunge Is a Signal to BuyWritten by Thomas Hughes. Published 10/17/2025.

Key Points - Abbott Laboratories' Q3 results did not catalyze a rally but also did not provide a reason to sell.

- Margin is solid, growth is present, and the capital return outlook is reliable.

- Analyst and institutional trends suggest these influential market groups will buy ABT on the dip.

Abbott Laboratories' (NYSE: ABT) October price plunge looks like a buy signal, as analyst and institutional trends point to continued buying. MarketBeat data show increasing analyst coverage, with new ratings initiated within days of the Q3 earnings release. Coverage is expanding, sentiment has firmed over the past two quarters, and price targets are moving higher. Analysts' consensus projected about a 10% gain ahead of the release — enough to reach a new all-time high — with the high-end range implying roughly another 10% upside. While headlines focus on Tesla's car sales, tech analyst Jeff Brown says the real story is Tesla's role in a $25 trillion AI revolution — one that Nvidia's CEO himself has called a "multi-trillion-dollar future industry" — and he's uncovered a little-known stock 168 times smaller than Nvidia that could be positioned to ride this breakthrough. Click here now to see the full report Institutional investors have been consistent net buyers of this healthcare stock throughout the year. MarketBeat's tracking shows institutions bought roughly $1.50 for every $1.00 sold over the past 12 months, accelerating in the back half of the year to about $3.25 bought per $1 sold as of mid-October. Institutions own roughly 75% of the stock, providing a solid support base and a tailwind for price action reflected in the charts.

The ABT chart shows a stock in a long-term uptrend that is now consolidating ahead of its next move. The monthly view indicates the stock is pulling back from recent peaks but remains in rebound mode, forming a bullish flag pattern after an October 2023 trend-line bounce and the price reversal confirmed earlier this year. Abbott's price action may consolidate through year-end, but the setup points to higher levels in 2026, driven by growth, earnings quality, and capital returns. A move to new highs would be significant — potentially representing roughly a $30 (about 30%) upside from current levels. Abbott Laboratories Q3 Release Is No Reason to Sell This Stock Abbott Laboratories' Q3 report was slightly softer than analysts' consensus, but not a reason to sell. Revenue missed consensus by only 0.17 percentage points, while reported revenue still rose 6.9% year over year and margins remained solid. Foreign exchange, which recently has been a headwind for many S&P 500 companies, turned into a tailwind for Abbott, positively affecting both revenue and earnings for the quarter. Revenue growth was driven by strength in both U.S. and international markets — international sales rose 9.9% — with growth across three primary reporting segments. Diagnostics was the weakest segment, down 7.8% organically, largely due to declines in COVID-19-related sales that are not central to the long-term business. Other segments performed better, led by 12.5% organic growth in Medical Devices and 7.1% in Established Pharmaceuticals. The margin story was encouraging. The company widened its adjusted operating margin by 40 basis points, producing leveraged income growth. Operating income rose 10.6%, net income grew 7.5%, and adjusted EPS was $1.30 — in line with expectations and up roughly 7.5% year over year. The key takeaway: Abbott's diversified model supports steady growth and healthy margins, which underpins its capital return outlook. Abbott Laboratories' Dividend Is Reliable and Growing Abbott Laboratories' dividend is reliable and is expected to grow at a high-single- to low-double-digit pace for the foreseeable future. The company is a Dividend King with more than 50 consecutive years of annual increases, maintains a payout ratio around 45%, and benefits from solid earnings growth expectations. Long-term consensus forecasts project Abbott growing earnings at a low-double-digit pace for at least the next five years — enough to support distribution increases without compromising financial health or investment in growth. Its diversified product portfolio across diagnostics, medical devices, nutrition, and branded generics provides multiple revenue streams, helping to buffer the company against sector-specific slowdowns. With a strong balance sheet and consistent cash flow, Abbott is well-positioned to sustain both growth investments and rising shareholder returns.

|