It’s happening right now…

A turning point that the former CEO of Google says is:

“The most important thing that’s going to happen in about 500 years – maybe 1,000 years of human society – and it’s happening in our lifetime.”

Yet very few are fully warning you of what’s coming.

Instead you’re kept distracted by the inane trivialities of “bread and circuses” while the very fabric of our lives erodes beneath our feet.

As one former U.S. Treasury Secretary says:

“When your great-grandchild writes the history of this period, my guess is that stuff about Donald Trump and Xi will be the second or third story.”

The first story they write about?

You and I have never seen anything like it before…

The dot-com collapse, global financial crisis, COVID-19 pandemic… nothing we’ve seen in our lifetime holds a candle to what’s coming next.

In short, I believe we are about to be plunged into a period of dramatic, almost unimaginable change.

And you need to be ready, or risk being left behind.

Porter Stansberry

3 Low P/E Stocks: Separating Multibaggers From a Value Trap

Authored by Thomas Hughes. Article Posted: 1/16/2026.

What You Need to Know

- Low P/E stocks offer value, limited downside, and potential for outsized gains if fundamentals improve, but they can also signal deeper problems.

- Comcast and HP Inc. stand out with high yields, oversold conditions, and analyst support pointing to meaningful upside in 2026.

- Rogers Communications trades at a discount but lacks near-term growth catalysts, with inconsistent dividend payments and muted institutional interest.

P/E, the price-to-earnings multiple, measures a stock's value relative to earnings and is a cornerstone of value investing. Stocks with lower P/E ratios are cheaper relative to their earnings, often indicate value for investors, and can deliver significant gains over time.

Additionally, low P/E stocks often have their bad news priced in, offer limited downside compared with higher-valued names, tend to provide above-average yields, and can produce multi-bagger returns. Improving fundamentals combined with earnings growth create a two-fold tailwind that can accelerate price appreciation as stocks are revalued and premiums are restored. The risk, of course, is that a low P/E can reflect structural problems — in that case, upside may be limited. Below is a look at five low P/E stocks and whether they present opportunities for gains in 2026.

Why Rogers’ High Yield Comes With Limited Upside

Did the government just make a $500 trillion mistake? (Ad)

A little-known government task force just wrapped up a 20-year project, and its findings could unlock access to a massive U.S. national asset. Under existing law, everyday Americans may now have a legal path to participate in what some are calling a once-in-a-generation opportunity.

Details are still flying under the radar, but that may not last.

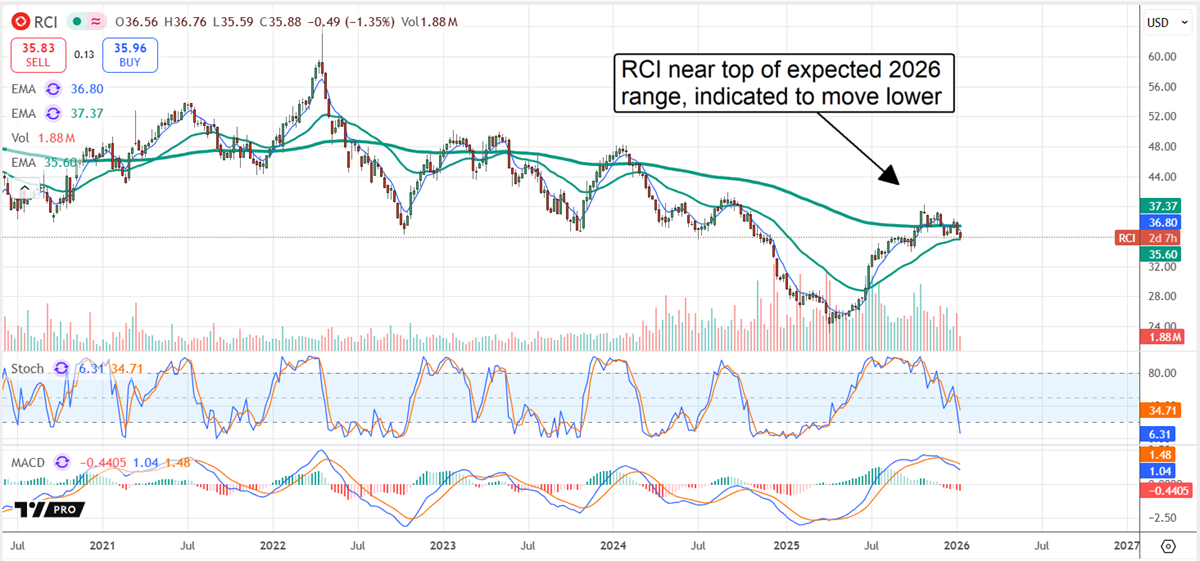

Rogers Communications (NYSE: RCI) is a Canadian communications and media company trading at about 10x current-year earnings, which on the surface suggests upside if it were to re-rate to broader market multiples. The company's dividend yielded more than 4% as of early 2026, but Rogers trades in line with media peers and faces a tepid outlook. Earnings growth is uncertain, and dividend growth is not assured — the company's payout history has been irregular, with variable quarterly distributions and recent cuts.

Analyst and institutional signals offer little reason to expect a rebound in 2026. Analysts rate it a Hold but have materially lowered price targets over the past year; the current target sits below the stock price. Consensus pricing in mid-January implies fair value that could point to downside. Institutional support is modest—institutions own roughly 45% of the shares and were net sellers at the start of the year.

Comcast Combines High Yield With Rebound Potential in 2026

Comcast Corporation (NASDAQ: CMCSA) is another media and communications company trading at a low P/E. It sits near 7x current-year earnings, which suggests value relative to peers, and it offers a roughly 4.5% dividend yield. The company will show a revenue and earnings decline due to divestitures, but core results are expected to grow and expectations are modest — a setup that could enable outperformance and spark a bullish analyst revision cycle. Analysts are already constructive on the name.

An analyst reset pressured CMCSA in 2025, but two factors point to a rebound in 2026. First, the stock became oversold and recent targets line up with the consensus forecast for about a 20% price gain. Second, institutional activity supports a recovery: institutions own more than 65% of the shares and were net buyers in early January, purchasing roughly $3 for every $1 sold in the first two weeks of the year.

HP Inc. Looks Positioned for a Powerful Rebound in 2026

HP Inc.’s (NYSE: HPQ) share price has been influenced by AI-driven demand and by DRAM shortages that have constrained supply and limited production. Those factors prompted analysts to reset price targets, but like Comcast, HPQ was oversold and is setting up for a rebound. The company is expected to deliver modest growth over the next few years and generate enough earnings to support capital return.

HP’s capital return program includes a dividend that yielded more than 5.5% annualized as of early January, and distributions are expected to grow. The company pays under 40% of earnings, has increased its dividend for 15 consecutive years, and its dividend has grown at roughly a 10% compound annual rate.

Analysts are optimistic. While consensus was trimmed in 2025, late-year and early-2026 updates have generally reaffirmed the outlook. Consensus implies about a 20% upside; achieving that level could trigger additional gains of 20%–30%. Technically, HPQ is trading near long-term lows and the MACD is diverging from price — a classic signal that the downtrend may be weakening and bulls could be poised to regain control.

This email message is a sponsored message sent on behalf of Porter & Company, a third-party advertiser of MarketBeat. Why was I sent this email?.

If you need help with your account, please don't hesitate to contact our U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl. #620, Sioux Falls, S.D. 57103. United States..