Ticker Reports for January 16th

3 Low P/E Stocks: Separating Multibaggers From a Value Trap

P/E, the price-to-earnings multiple, is a measure of stock value relative to earnings power and a cornerstone of value investing. Stocks with lower price multiples are cheaper to own relative to their earnings power, indicate value for investors, and have the potential for significant price gains over time.

Additionally, low P/E stocks typically have their bad news priced in, offer limited downside relative to higher-valued stocks, provide higher-than-average yields, and offer the opportunity for multi-bagger gains. The combination of improving fundamentals and earnings growth provides a dual-market-tailwind and leverage for price action as stocks are revalued and premiums are priced in. The risk is that low P/E stocks are cheap for a reason. In this scenario, there is little hope for stock price gains. This is a look at five low P/E stocks and whether they present opportunities for gains in 2026.

Why Rogers’ High Yield Comes With Limited Upside

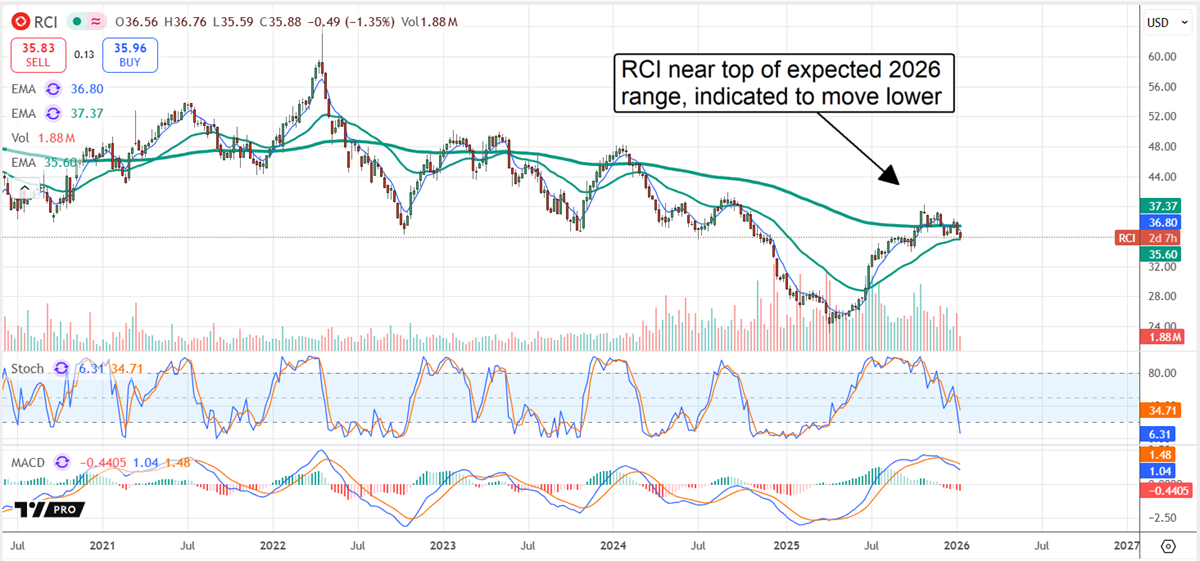

Rogers Communications (NYSE: RCI) is a Canadian communications and media company. It trades at a low 10x current-year earnings, suggesting it could rise by 100% to align with broad market averages. The problem is that this company, whose dividend yields more than 4% as of early 2026, trades in alignment with media peers and has a tepid outlook for the year. Not only is earnings growth questionable, but so too is dividend growth. The company’s payment history is spotty, with irregular quarterly distributions and recent declines.

Likewise, analysts and institutional trends provide no reason to expect this stock price to rise in 2026. Analysts rate it a Hold but have significantly reduced their price targets over the trailing twelve months, resulting in a price point below consensus. Consensus assumes fair value in mid-January, suggesting a likely downside move. Meanwhile, institutions provide mediocre support, owning about 45% of the stock and distributing shares at the start of the year.

Comcast Combines High Yield With Rebound Potential in 2026

Comcast Corporation (NASDAQ: CMCSA) is another communications and media company trading at a low P/E multiple. The difference is that this stock trades at only 7x its current-year earnings, indicating a value relative to its peers, along with a 4.5% dividend yield. This company will report a decline in revenue and earnings due to divestiture, but its core results are expected to grow, and expectations are modest. This sets the company up to outperform and drive a bullish analyst revision cycle, and the analysts are already optimistic on the stock price.

An analyst reset helped depress CMCSA stock prices in 2025, but two factors set the market up to rebound in 2026. The first is that the CMCSA market oversold, and the most recent targets align with the consensus forecast for a 20% stock price increase. Institutional activity also aligns with a rebound in early January, as they own more than 65% of the stock and bought at a pace of $3 for each $1 sold the first two weeks of the year.

HP Inc. Looks Positioned for a Powerful Rebound in 2026

HP Inc.’s (NYSE: HPQ) share price is affected by AI, as DRAM shortages are curtailing supply and limiting production. The impact caused analysts to reset their price targets. However, as with Comcast, this market has oversold and is setting up for a rebound. While the outlook is depressed, this company is expected to sustain modest growth over the next few years and generate sufficient earnings to support its capital return. The capital return includes a dividend yielding more than 5.5% annualized as of early January, along with an expectation of distribution growth. HP Inc. pays less than 40% of its earnings, has increased its dividend for 15 consecutive years, and has a 10% CAGR.

Analysts are optimistic. Their reset reduced consensus in 2025, but late-year and early-2026 updates have reaffirmed it. The takeaway is that this stock is expected to rise by at least 20%, and the 20% stock price gain indicated is the trigger for another 20% to 30% gain when achieved. Looking at the chart, HPQ stock is at its long-term lows, and the MACD is diverging from the price movement. The divergence is a critical indicator, as it signals a weakening downtrend with bulls ready to regain control.

Ticker Revealed: Pre-IPO Access to "Next Elon Musk" Company

Ticker Revealed: Pre-IPO Access to "Next Elon Musk" Company

3 Metals Stocks Bank of America Is Bullish on for 2026

The first quarter earnings season coincides with the start of a new year and new forecasts for which stocks and sectors are likely to perform well. Most growth-oriented investors will continue to be in technology stocks. However, many analysts believe metals and mining stocks will outperform. This trade is about more than gold and silver. Copper and uranium stocks are also expected to outperform.

Bank of America (NYSE: BAC) recently released its top commodity stock picks for 2026. The list includes three mining stocks, which makes sense. With gold, silver, and copper at record levels, the companies that mine these metals become significantly more profitable.

Agnico Eagle: Gold Exposure With Operational Leverage

The gold and silver trade will continue to be strong in 2026 for several reasons. First, it’s a hedge against the ongoing devaluation of the U.S. dollar. Supply and demand imbalances also support the bullish narrative. There’s growing industrial demand, and a limited supply that’s tough to extract.

Agnico Eagle Mines (NYSE: AEM) is a best-in-breed gold miner that delivered strong performance in 2025 due to a high spot price of gold and lower oil prices. That combination makes it more cost-effective for the company to increase its mining production to a record 870,000 ounces in its most recent quarter.

AEM stock is up more than 134% in the last 12 months and is brushing up near its consensus price target. However, that’s partly based on expectations of negative earnings growth in the next 12 months. That’s not supported by other sources, which suggest Agnico Eagle could grow earnings by over 22%.

Whenever investors are faced with such a wide range of options, a smart idea is to split the difference. In this case, that still suggests an upside bias for AEM stock.

Freeport-McMoRan: Copper’s Breakout and Long-Term Demand

For many investors, copper is the breakout trade they’ve been waiting on for two years. It’s been a long wait, but in the last month, copper has broken to an all-time high, and it looks like things are just getting started.

That makes Freeport-McMoRan Inc. (NYSE: FCX) a no-brainer choice for stocks you can go long with. FCX stock stumbled after a mining accident in Indonesia. But the company, and its stock, are regaining their footing.

Freeport-McMoRan stock is trading close to its 52-week high and above its consensus target, but still carries a consensus Buy rating due to projected earnings growth of 28% that may not be priced in.

Cameco: Uranium’s Role in the Global Nuclear Buildout

Copper may be the breakout metal in early 2026, but many experts believe that uranium will be the metal to watch in the second half of the year. Nuclear energy has moved from being an ancillary part of the energy story to the main character.

The narrative is about data centers in the United States. However, globally, nuclear power will be needed in order for many companies to meet net-zero requirements.

There are many ways to play this sector, but Cameco Corp. (NYSE: CCJ) is a pure play on uranium. It's the world’s largest publicly traded uranium company, and its business model focuses on long-term contracts with utilities. This gives Cameco and its investors a line of sight on revenue and earnings for years to come.

CCJ stock has soared over 120% in the last 12 months. It’s not expected to deliver another monster gain in 2026, but there’s still likely to be double-digit upside in 2026 and beyond.

Mining Stocks as an Equity-Based Way to Access Metals

Gold and silver were two of the best investments in 2025. However, for all the positive sentiment surrounding gold, silver, and other metals, there is a risk of being over-weighted in the category. That comes from data that supports the narrative of a healthy U.S. economy that will power corporate earnings. Strong corporate earnings create a virtuous cycle that will drive stocks higher.

Ultimately, gold and silver are a hedge against a slumping economy. That's a good reason to look at mining stocks. These stocks provide exposure to the underlying metals trade while staying in equities as the economy continues to run hot.

The gold story that no one's telling

The gold story that no one's telling

Small Caps Break Out! Russell 2000 Poised for 40% Gain

While the S&P 500, Dow, and Nasdaq were mixed to start the year, the Russell 2000 (INDEXRUSSELL: RUT) moved up to set a new high and extended gains in the subsequent week.

That breakout is a bullish technical signal across multiple time frames. Based on prior move size, this rally could advance by 750 points as a low-end target and, in a stronger scenario, up to 45% from the breakout point. A 750-point gain puts this market near 3,250, a 45% advance near 3,650. Here’s a look at what’s driving the move.

Market Rally Broadens as Economic Strength Drives Upside

Numerous factors have converged in early 2026, suggesting a cyclical rally is upon us. Profitability, economic strength, and valuations are at the heart of the story, driving a catch-up trade in the non-tech and small-cap stocks that make up the Russell 2000 Index.

Moderating interest rates and inflation, along with operational improvements and consumer health, are likely to drive accelerating growth in non-tech names in 2026.

Meanwhile, the Atlanta Fed's GDPNow tool forecasts Q4 GDP growth at 5.3%, suggesting that economic momentum accelerated into the end of 2025. Early indications, including anecdotal evidence in JPMorgan’s (NYSE: JPM) January earnings release, suggest that these tailwinds will persist for the foreseeable future, potentially strengthening by year’s end as positive feedback loops form.

Labor Markets and Low Valuations Underpin 2026 Russell 2000 Outlook

Labor markets and consumer health are critical to the Russell 2000's outlook. Labor markets weakened in 2025, pulling back sharply from their COVID-19-induced strengths, but have remained healthy overall. Employment levels, including wages, jobless claims, and job creation, are trending at historically healthy levels and are notably stronger than before the COVID-19 pandemic.

In 2025, lackluster growth, contraction, and underperformance sapped investor appetite for many non-tech names. However, the price action of 2025 left non-tech firms trading at the lower ends of their valuation ranges, making them attractive plays for 2026, especially compared to expensive mega-cap tech giants. Investors have a two-fold opportunity, as earnings growth is improving and a bullish market revaluation could drive share price action this year.

Top Sectors for Small-Cap Growth in 2026

While some mega-cap tech names are looking overextended, technology has the potential to be a winning play in the small-cap sector in 2026. The accelerating digitization, cloud use, and data center boom are spilling over into adjacent industries that support the construction and operation of critical AI infrastructure. Additionally, industrials and infrastructure companies are expected to be strong, supported by lower interest rates, government deregulation, and consumer spending. Office space is also expected to see increased demand, underpinned by economic expansion.

Forecasts for the Russell 2000 range from 15% to 20%, with some pointing as high as 30%, compared to about 15% for the S&P 500. However, investors should be cautious, as this group has historically included many underperforming names. For a more detailed, stock-by-stock look at potential small-cap upside, see this MarketBeat analysis of five small-cap names setting up for outsized moves and the corresponding buy/sell/hold takeaways.

As always, investors should do their own research, considering factors like growth estimates, analyst revisions, bullish or bearish sentiment, and profitability. Companies that are profitable today or are pivoting to profitability will perform best, while pre-profit companies will likely see high volatility.

Trump's crypto czar leaked THIS

Trump's crypto czar leaked THIS

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.