Good day,

Thank you for subscribing to the Earnings360 newsletter, your daily source for quarterly earnings news and updates.

Each morning edition contains a wrap-up of today's pre-market earnings announcements and yesterday's earnings announcements after the closing bell.

Before we send you your first edition, please take a moment to confirm your subscription below. We will not be able to send your newsletter until you confirm your subscription.

Confirm Your Subscription Here

The Earnings360 Team

Saturday's Featured Content 3 Under-the-Radar AI Stocks to Buy on the DipWritten by Dan Schmidt. Published 11/15/2025.

Key Points - Markets have been volatile over the last few weeks, and some stocks have pulled back from previous highs.

- Despite this pullback, the long-term AI uptrend still looks promising, and data center spending continues to reach unprecedented levels.

- These three AI-related stocks could be great 'buy the dip' opportunities for investors who missed the initial rally.

Investors have been conditioned to buy dips since the 2008 Global Financial Crisis, a belief reinforced by aggressive government market support during the COVID-19 pandemic. The 2018 bear market? Buy the dip. A new virus shutting down the economy? Buy the dip. The Fed starts raising rates with authority? Buy the dip. Does President Trump enact disruptive tariff policies? Buy the dip. There may come a day when buying the dip becomes a poor strategy, but prior corrections and bear markets have often presented opportunities to purchase assets at a discount. Warren Buffett is the greatest value investor of all time. But even the Oracle of Omaha has limits.

Because of Berkshire Hathaway's size, Buffett simply can't invest in small-cap stocks without taking controlling stakes. That means some of the market's most promising companies are completely off his radar.

But they don't have to be off yours.

We've put together a brand-new report profiling 5 small-cap stocks that check all the boxes of Buffett's investing criteria solid financials, durable business models, strong management, and clear growth catalysts.

The only difference?

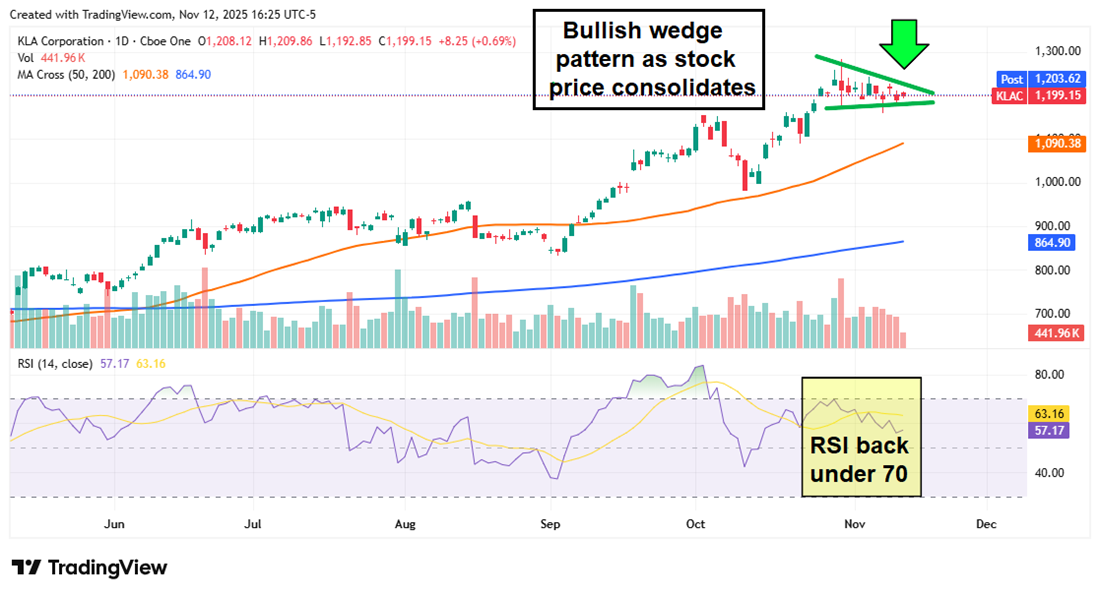

These stocks are flying under Wall Street's radar and still accessible to individual investors like you. >> Click here to get your free copy of this report Today, artificial intelligence dominates market headlines, and the capital expenditure devoted to AI buildouts is staggering. There's no greater example than NVIDIA Corp. (NASDAQ: NVDA), which surpassed a $100 billion market cap in early 2019 and is now on the cusp of becoming one of the most valuable companies in history. While hyperscalers and chipmakers grab headlines, under-the-radar tech companies are increasingly offering attractive risk/reward. This recent volatility presents an opportunity to buy dips in less heralded but highly profitable names. Below are three companies at the forefront of their industries that address critical AI bottlenecks in quality control, thermal management, and CPU design. KLA Corporation: A Stranglehold on Process Controls As chips get smaller and denser, quality control becomes increasingly critical. Manufacturing advanced AI chips requires tight process controls because the slightest nanoscale variation or defect can render a semiconductor useless. The cost of producing defective chips far exceeds the cost of quality control. That makes the technology from KLA Corp. (NASDAQ: KLAC) essential for any chipmaker serving data center customers. KLA's inspection suite can check chips throughout the manufacturing process, ensuring each layer and structure is fabricated correctly. The company manufactures, installs and services its systems, generating recurring revenue. A major catalyst for KLA is the growth of advanced packaging, which enables integration of multiple semiconductors into a single device. Advanced packaging improves performance but creates more intricate designs that demand additional quality control. In its fiscal Q1 2026 report, KLA management forecast $925 million in revenue from advanced packaging services, a 70% year-over-year increase.

Despite these fundamental tailwinds, the stock has pulled back from its late-October all-time high and is consolidating in a wedge pattern. A breach of the upper trendline typically signals the next leg up in a rally. With the Relative Strength Index (RSI) now back under 70, a breakout could be imminent. ARM Holdings: Next-Gen Designs for Next-Gen AI ARM Holdings plc (NASDAQ: ARM) has lagged some larger peers like NVDA, but the U.K. chip designer occupies a strong position in the AI ecosystem with a unique licensing model. ARM doesn't manufacture chips; it licenses intellectual property to customers who build the chips themselves. ARM's Neoverse platform continues to expand, reaching roughly a 25% penetration of the data center CPU market earlier this year. In its fiscal Q2 2026 earnings release, ARM reported year-over-year revenue growth of more than 34% and counts many hyperscalers, including Meta Platforms Inc. (NASDAQ: META), as customers for custom silicon.

Despite record revenue, ARM shares had a rocky 2025 and have yet to reclaim the all-time high set in July 2024. Although the stock flashed a Golden Cross this summer, it recently dipped below the 50-day simple moving average (SMA) for the first time since September. The 200-day SMA could provide more durable support, as it has during prior volatile stretches. The RSI also hints that ARM may be approaching a short-term bottom, so watch for a potential reversal off the 200-day SMA. Vertiv Holdings: Innovators in Cooling Technology Data centers generate enormous heat and require sophisticated cooling systems to avoid damage or accelerated obsolescence. Vertiv Holdings Co. (NYSE: VRT) is an innovator in electrical thermal management, and its liquid-cooling systems are likely to be critical as data centers scale up. Providers aim to pack as many servers as possible into racks, and a single AI rack can consume power comparable to that of 100 households. As power density rises, traditional air cooling becomes less effective. Vertiv says its liquid-cooling solutions can be significantly more efficient than conventional systems, and the addressable market for its technology is expected to grow at about a 20% compound annual growth rate through the decade.

Despite an impressive Q3 2025 earnings beat and guidance raise (including a $9.5 billion order backlog for 2026), the stock has pulled back from its post-earnings high. That pullback appears to be profit-taking after a year in which the stock was up more than 50% year to date for many long-term holders. The company has numerous fundamental tailwinds, and the technical trends also look promising. After a July Golden Cross, the stock has used the 50-day SMA as support, and the price now appears headed back toward that level following an overbought signal on the RSI. The long-term uptrend remains intact, and the 50-day SMA could be a reasonable entry point for new positions.

|