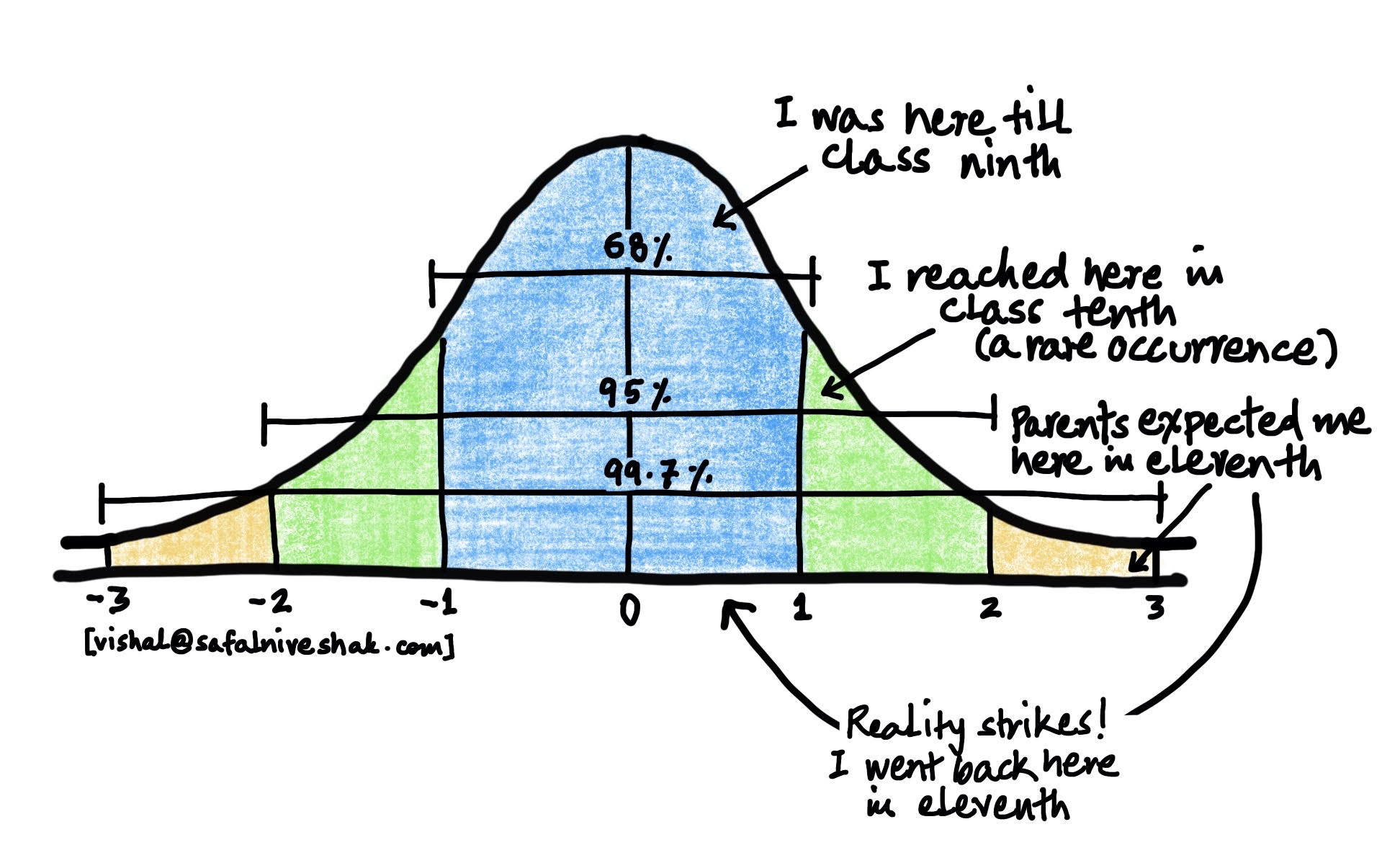

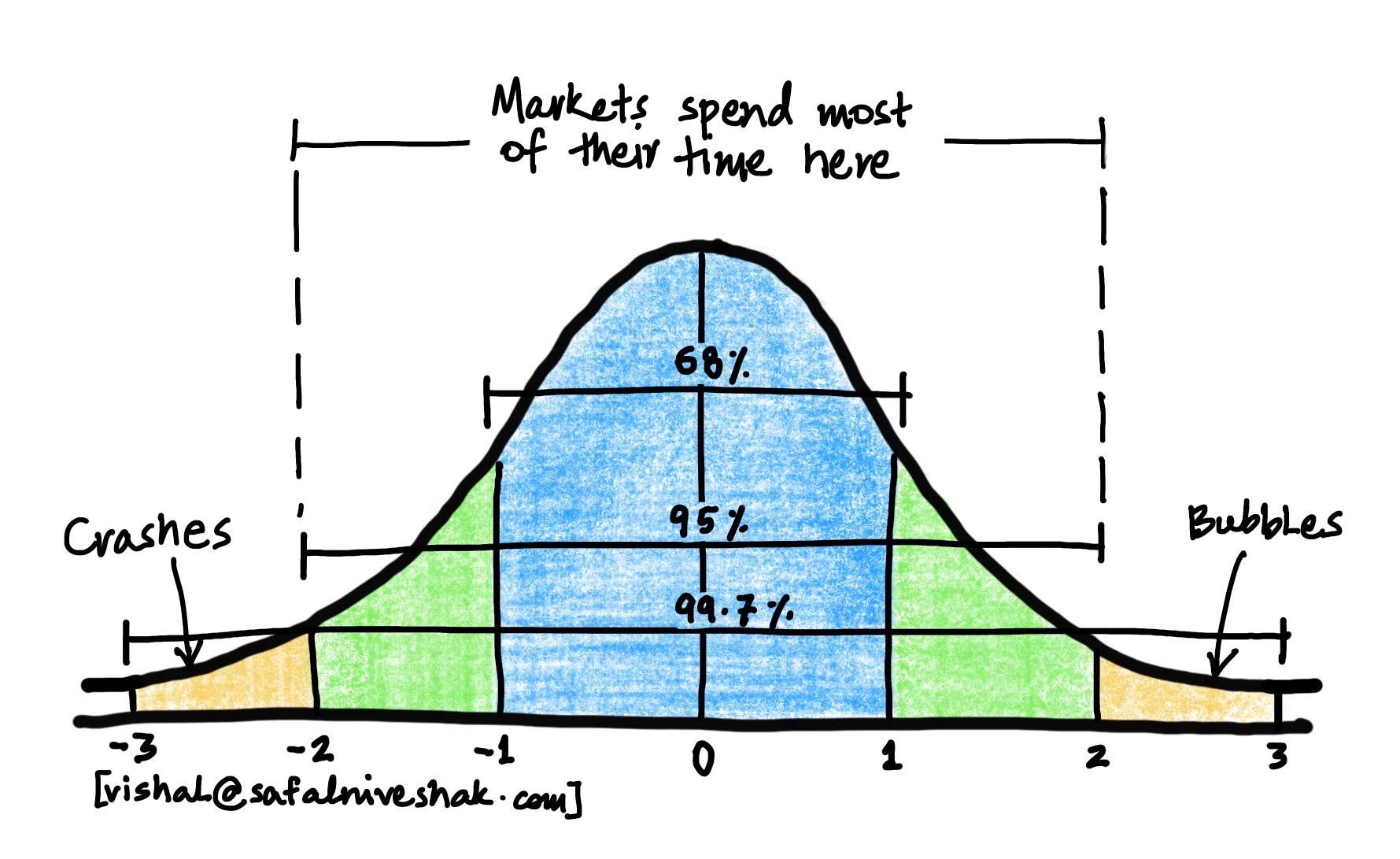

| However, this had an unintended consequence. In eleventh, my parents extrapolated my performance from tenth and drew a pattern in their minds that would move me within three standard deviations (among the top 2.5% students, which essentially meant first in class). They ignored the fact that my tenth performance was a tail event given the rest of my performances at school, and they should not have predicted the future based on one such event that had a rare chance of re-occurrence. Well, to their dismay, I came back to one standard deviation in eleventh, thus failing their expectations. After that, they stopped expecting anything from me (which, in hindsight, was good). Now, the reason I share this story of my 'accomplishments' with you is because I was reminded of it while reading one of the Howard Marks' memos. One of the parts from the same reminded me of those days when my parents extrapolated my future performance by drawing patterns from the past, and failed because that past was a rare occurrence amidst my long list of average performances. This is, after all, what most of us investors do. Most of our investing lives is spent while the markets perform within two standard deviations of the normal, but we still use our learning from these times to extrapolate and predict how the markets will behave when they are beyond two standard deviations i.e., during bubbles and crashes. Now, we are not wrong in building our expectations using such past history, for that is where we spend most of our time, but that is what makes predicting such a difficult, almost impossible, task. Here is the part from Marks' memo I am referring to – …one of the great conundrums associated with investing … Since we know nothing about the future, we have no choice but to rely on extrapolation of past patterns. By "past patterns," we mean what has normally happened in the past and with what severity. And yet, there's no reason why (a) things can't happen that differ from those that happened in the past and (b) future events can't be worse than those of the past in terms of severity and thus consequences. While we look to the past for guidance as to the "worst case," there's no reason why future experience should be limited to that of the past. But without reliance on the past to inform us regarding the worst case, we can't know much about how to invest our capital or live our lives. Many years ago, my friend Ric Kayne pointed out that "95% of all financial history happens within two standard deviations of normal, and everything interesting happens outside of two standard deviations." Arguably, bubbles and crashes fall outside of two standard deviations, but they are the events that create and eliminate the greatest fortunes. We can't know much in advance about their nature or dimensions. Or about rare, exogenous events like pandemics. |