Thanks for signing up for DividendStocks.com! It's the daily newsletter built for dividend and income investors. Before we can begin sending your daily updates, there’s one quick step left. Please confirm your subscription using the link below so our emails reach your inbox. Click Here to Confirm Your Subscription to DividendStocks.com Here’s a small glimpse of what you’ll get access to: Dividend Stock Ideas — Each newsletter features dividend stocks with high yields, sustainable payouts, and strong growth potential. Ex-Dividend Stocks — Want to capture upcoming dividend payouts? Find out which stocks are going ex-dividend this week. Market News and Events — Stay in the loop on the latest developments impacting popular dividend names like AT&T, Exxon Mobil, IBM, Procter & Gamble, and Verizon. Bonus: As a thank-you for confirming, you’ll also receive a free PDF copy of Automatic Income, our popular guide to building wealth through dividend investing. Let’s get your dividend journey started! Discover Top Income-Generating Stocks Here See you in your inbox soon,

The DividendStocks.com Team P.S. Don’t miss out click here to verify your subscription and secure your daily dividend insights and your free investing guide!

Special Report United Parcel Service Transitions to Growth: Accumulation BeginsWritten by Thomas Hughes. Posted: 1/28/2026.

Article Highlights - United Parcel Service has returned to growth sooner than expected, and its stock price looks to be in rebound mode.

- An ample capital return is reliable in 2026, with distributions expected to increase.

- Analysts and institutional data align with a market bottom and reversal, and trends will likely strengthen as 2026 progresses.

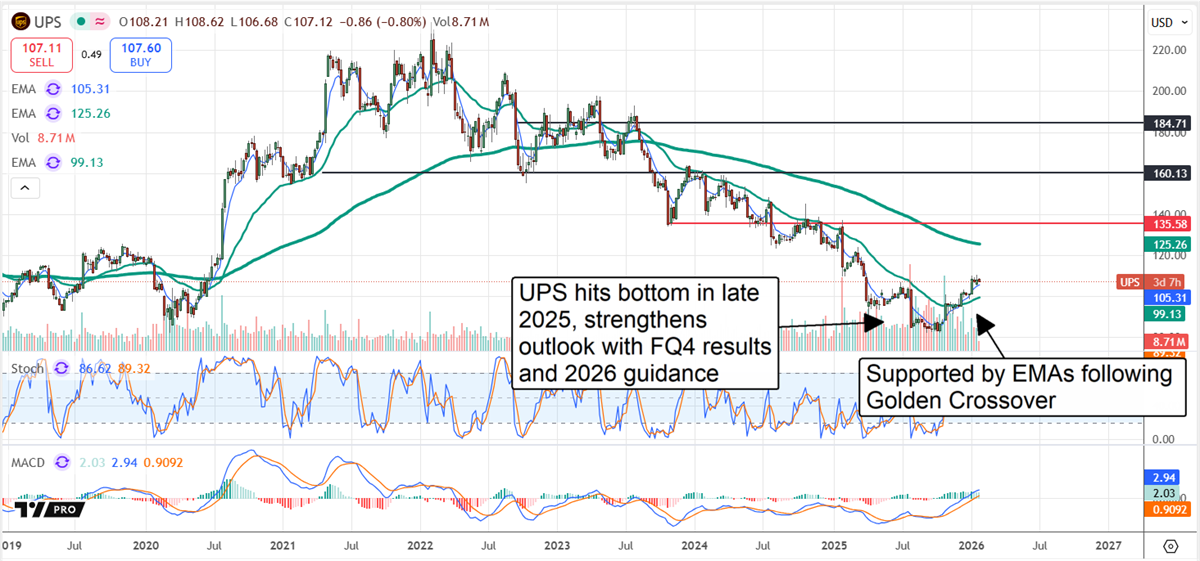

The long-awaited bottom in United Parcel Service (NYSE: UPS) stock appears to be in, and a rebound is underway. Backed by solid results, improving operational quality and a growth-oriented outlook, this recovery is poised to be meaningful for long-term holders. The UPS market — long pressured by distributive activity and analyst downgrades — has shifted into accumulation and should strengthen as the year progresses. Analysts and Institutions Have Shifted to Bullish The shift is evident in analyst activity. The analyst group still rates the stock a consensus Hold, but began raising price targets in late 2025. A growing number of investors are paying attention to developments around private space companies and potential future public listings.

In a recent briefing, one research publisher outlines how some investors are seeking early exposure to the space economy through publicly traded assets — without waiting for a formal IPO. The presentation walks through the structure, risks, and mechanics behind this approach for those who want to understand how it works. Read the full sponsor briefing here Bullish revisions continued into early 2026 and picked up momentum once the 2026 guidance was released. The company forecasted $89.7 billion in net revenue — roughly 300 basis points above MarketBeat's reported consensus — and now expects growth a full year earlier than previously anticipated. Management also expects margins to remain strong, supporting the potential for a leveraged earnings rebound. Institutional activity is supportive as well. Institutions own about 60% of the stock and were net buyers in Q4 2025. While some selling coincided with UPS's lows, a late-quarter shift toward accumulation extended into January 2026 and appears likely to continue. The Q4 strengths and the 2026 guide also reinforce a reliable capital-return program for investors. Dividend Strength and Buybacks Reward Investors Trading near COVID-19-era lows, the stock currently yields more than 6% and is expected to sustain dividend increases over the coming years. The 2026 guidance projects payouts slightly above 2025 levels, implying another low-single-digit raise is likely. Share repurchases trimmed the share count by about 0.7% in 2025, and buybacks are expected to continue in 2026. UPS Accelerates Stock Reversal With Strong Results UPS delivered a solid Q4 despite reporting a net contraction. Revenue declined 3.2%, but came in roughly $0.5 billion better than expected. Strength in revenue per package and international markets helped offset weakness in domestic volumes and supply-chain solutions. Adjusted operating margin contracted as anticipated and matched forecasts, leaving adjusted earnings above consensus by a similar margin. That combination — a better-than-feared top line and margins broadly in line with expectations — creates an opportunity for investors to enter early in the rebound. The outlook for earnings, the potential for outperformance, and the shift in analyst sentiment point to a cycle of outperformance and further bullish revisions. Under this scenario, UPS could reach the high end of the early-2026 target range — roughly a 40% gain from the pre-release close — as upgrades and higher price targets attract demand. UPS Advances Following Strong 2026 Guide UPS stock ticked up after its 2026 guide, showing support near the 30-day exponential moving average (EMA). The 30-day EMA has been moving higher along with the 150-day EMA after a Golden Cross formed in December 2025. That signal, combined with increasing accumulation, suggests the EMA cluster can act as durable support and sets the stage for a more substantial rebound.

Key catalysts for 2026 include persistent revenue growth, margin recovery and continued outperformance. The company's push into digitization, automation and AI should gain traction and compound as overall business quality improves. Amazon-related volume declines are expected to stabilize as the business mix shifts toward higher-margin consumer and commercial traffic. Industry-specific initiatives — notably healthcare, where UPS targets specialized, time- and temperature-sensitive transportation solutions — should also contribute to stronger results.

|