Wafer-scale technology could deliver 100X the performance while using 90% less energy...

Dear Fellow Investor,

While everyone’s fighting over AI scraps...

Trump just triggered what I believe is the biggest tech disruption since the internet.

I’m George Gilder. I’ve been calling tech revolutions for 40+ years.

When I predicted cell phones would change everything in 1991, people laughed.

When I said streaming video would kill Blockbuster in 1994, Wall Street ignored me.

When I called Amazon’s dominance in 1996, investors shrugged.

Those “crazy” predictions were followed by insane returns:

- Apple: 249,900% since IPO

- Netflix: 112,700% from going public

- Amazon: 216,100% since IPO

Now I see something even BIGGER brewing…

I see the death of big data centers coming. And My research suggests three companies are making it happen: building what I call the “Trillion Dollar Triangle”:

- Wafer-scale chips 100X faster than current systems

- 90% energy reduction

- Technology that makes AI data centers unnecessary

Make no mistake... This could be one of the biggest opportunities I’ve seen in over four decades.

>> Get the three company names before Wall Street catches on <<

To the future,

George Gilder

Editor, Gilder’s Technology Report

3 Consumer Staples Stocks Breaking Out This Month

Written by Dan Schmidt. Article Published: 2/9/2026.

Key Points

- Investors have started rotating out of volatile tech stocks and into safer assets.

- Consumer staples are often considered a 'safe' sector since its constituients sell necessities like food, household items, and hygiene products.

- These three consumer staples stocks appear to be on the verge of breaking out following a rough performance in 2025.

- Special Report: [Sponsorship-Ad-2-Format3]

A new rotation is underway as investors abandon the tech ship in search of safer assets. AI hyperscalers are still posting solid earnings, but even the Magnificent Seven are selling off after posting impressive top- and bottom-line beats. As bold AI capital expenditure (CapEx) plans are met with skepticism rather than optimism, the market is shifting toward a risk-off environment, making commodities and sectors like consumer staples look more attractive. If the tech rotation continues to intensify, the three stocks discussed below offer upside potential along with strong dividend income.

Rotation Into Consumer Staples Is Picking Up Steam

Nothing lasts forever in markets, and the AI trade is starting to wobble harder than it has since the end of the Fed hiking cycle in 2022. AI bellwether NVIDIA Corp. (NASDAQ: NVDA) hasn't gained much in six months, and Oracle Corp. (NYSE: ORCL) has lost about 60% since its September all-time high. Mega-caps like Alphabet Inc. (NASDAQ: GOOGL) and Amazon Inc. (NASDAQ: AMZN) dipped after earnings despite announcing 2026 CapEx plans that rival the GDP of some small countries. But data-center growth takes time, and hyperscalers are competing for increasingly scarce resources (e.g., energy and memory).

Elon Musk: This Could Turn $100 into $100,000 (Ad)

What if you could shrink your entire wealth journey from decades down to just 24 hours?

Sounds impossible…

But I'll show you how Elon Musk is about to make it a reality.

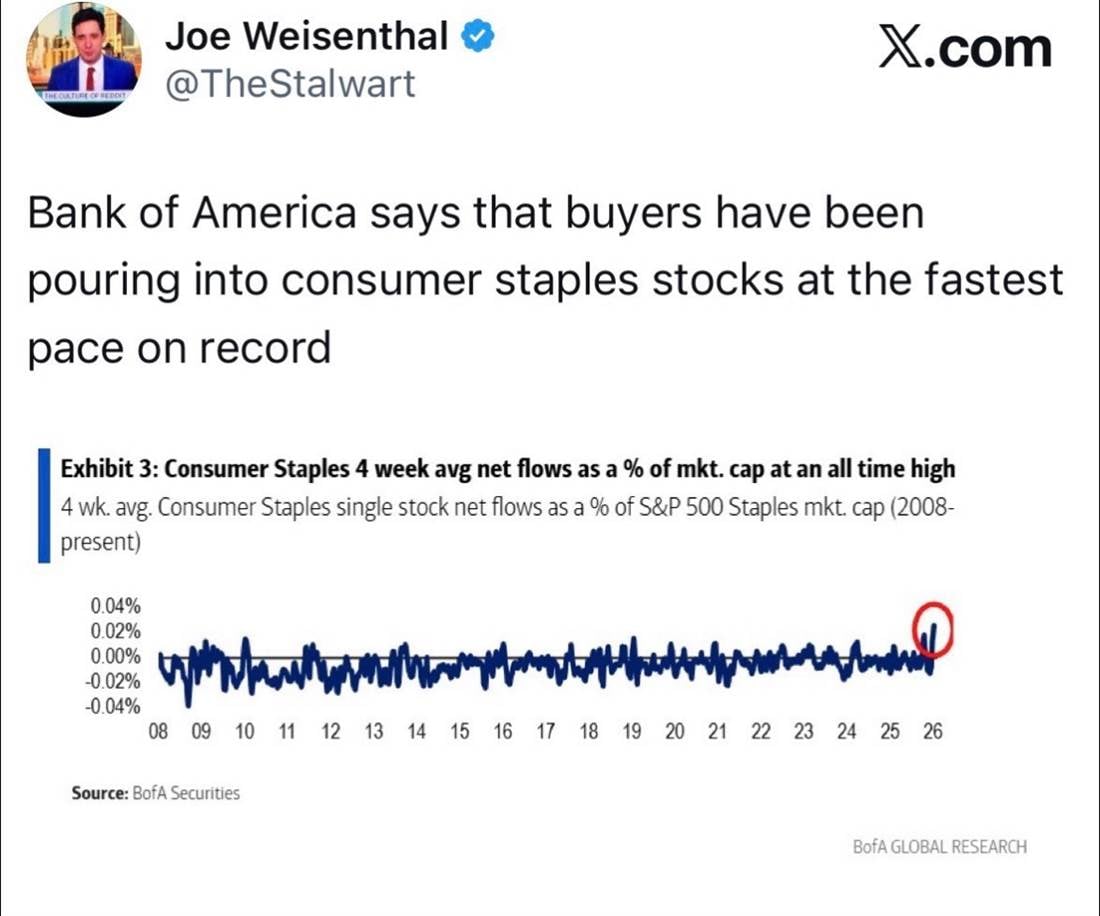

Investors are starting to look for risk-off assets in case these ambitious plans fail to deliver profits, but recent moves in gold and silver hardly qualify as a classic flight to safety. Money may be flowing out of tech stocks, but it isn't leaving the market entirely — as this post from Bloomberg's Joe Weisenthal illustrates:

Consumer staples usually aren't the target of speculative fervor, so large inflows suggest investors are taking some risk off the table as speculative returns wane. These defensive companies deliver consistent, predictable sales and typically return a sizable portion of profits to shareholders. With cryptocurrencies struggling and the precious-metals trade sputtering, the stampede into staples may be gaining momentum.

3 Breakout Consumer Staples Stocks With Strong Dividends

Predictability is a perk of value sectors like consumer staples, but that doesn't always mean sacrificing growth. The three stocks selected here are household names that suffered significant drawdowns in 2025, yet are now showing signs of technical breakouts in 2026.

Procter & Gamble: Dividend King Making Long-Awaited Technical Breakout

Procter & Gamble Co. (NYSE: PG) just had its best month in nearly two years, gaining about 13% over the last 30 days. Margins are one driver of the breakout: the company generated 270 basis points of productivity savings in its fiscal Q2 2026 results to help offset tariff headwinds. The stock is also clearing a key technical level, rising above the 200-day simple moving average (SMA) for the first time since early last year.

The company maintained its 2026 revenue guidance, which bodes well for another year of dividend increases for this Dividend King. P&G has raised its dividend for 70 consecutive years, while allocating roughly 62% of earnings and less than 50% of free cash flow to dividends. The company returned more than $4.8 billion to shareholders in Q2 alone, making PG a defensive option for investors seeking income during volatile markets.

Reynolds Consumer Products: Mitigating Tariffs and Commodity Volatility

Reynolds Consumer Products Inc. (NASDAQ: REYN) jumped nearly 10% after its Q4 2025 earnings release on Feb. 4, largely driven by margin resilience amid stiff tariffs and price increases. Aluminum is the biggest concern for the maker of Reynolds Wrap foil, with the spot price up nearly 20% since last April. Reynolds nonetheless maintained 21% adjusted EBITDA margins on $220 million in earnings and successfully offset higher input costs. The Hefty brand also posted a 3% year-over-year (YOY) retail volume increase.

The daily chart is showing signs of life, with a Golden Cross and support forming at the 200-day SMA. Reynolds also offers a about 4% dividend yield with a 63.9% dividend payout ratio (DPR), though it doesn't have a long history of raises like P&G. Reynolds' dividend behaves more like a bond coupon, but the company appears to have ample room to maintain it, especially if aluminum price pressure eases.

Constellation Brands: Strong Earnings and Stock Breakout Calm Beer Slowdown Fears

Concerns about declining beer sales have weighed on Modelo and Pacifico parent Constellation Brands Inc. (NYSE: STZ), but the company managed to quell those fears for at least one quarter with its latest report. Constellation released its fiscal Q3 2026 earnings last month: revenue declined nearly 10% year over year but beat expectations. Beer operating margins came in better than expected, helping limit the damage, and the stock is up more than 15% since the Jan. 8 release.

Bullish momentum has been building in STZ since last November, and the stock has finally broken above the 200-day SMA after a prolonged downtrend. Constellation is an attractive value play, trading at roughly 12 times forward earnings and 2.6 times sales. It also uses only about 12% of its cash flow to cover its 2.46% dividend yield and has raised its payout for five consecutive years.

Exelixis Reports Solid Earnings—Are New Highs Back on the Table?

Authored by Chris Markoch. Publication Date: 2/12/2026.

Key Points

- Exelixis delivered a major EPS beat driven by strong Cabometyx demand, highlighting the company’s profitability and continued leadership in kidney cancer treatments.

- The biotech is transitioning to a multi-franchise oncology model, with zanzalintinib targeting colorectal cancer and representing a potential $5 billion peak-sales opportunity pending FDA review.

- Heavy R&D investment alongside share buybacks signals confidence in the pipeline, positioning Exelixis for sustained growth beyond its current single-drug revenue base.

- Special Report: [Sponsorship-Ad-2-Format3]

Exelixis Inc. (NASDAQ: EXEL) stock is down about 2% in early trading the day after the company delivered a solid, but mixed earnings report. The company reported earnings per share (EPS) of $0.94, 27% above the consensus estimate and 95% higher year-over-year (YoY).

The improved profitability also expanded operating margins, which Exelixis plans to reinvest into research and development to support its franchise strategy. The company also repurchased $264.5 million of its stock.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Revenue was mixed. The $598.66 million in revenue missed expectations of $609.17 million, but was up 5% from $566.76 million in the same quarter last year. Much of that revenue was driven by Cabometyx, the company's branded formulation of cabozantinib used across multiple cancer types.

Exelixis forecasts 2026 revenue of $2.52 billion to $2.62 billion. Importantly, that guidance excludes any potential revenue from zanzalintinib, its pipeline candidate for colorectal cancer, if it receives regulatory approval.

What Makes Exelixis Different?

At one level, Exelixis carries the same risk-reward profile as many other biotech companies. Investors should, however, pay attention to the company's franchise strategy.

Exelixis is building comprehensive treatment ecosystems around specific molecules, aiming to develop deep expertise in particular tumor types with multiple treatment lines and combinations that physicians can use at different stages.

In plain terms, Exelixis is working to have multiple therapeutic options for specific cancers — first-line, second-line, and combination therapies — so it can become a go-to choice for oncologists treating kidney cancer, colorectal cancer, or neuroendocrine tumors.

Two key takeaways from the fourth-quarter report:

- Cabozantinib is effective in kidney cancer both as monotherapy and in combination with immunotherapy, and it remains the primary revenue driver today.

- Zanzalintinib is described as "the foundation of future oncology franchises" and has the potential to reach $5 billion in peak annual sales.

Consolidation Now, Growth Later

Trading at roughly 18x trailing twelve-month earnings and 21x forward earnings, EXEL carries a modest premium to the broader biotechnology sector. The franchise model and deep pipeline, however, may justify that premium if the expected growth materializes.

The EXEL chart looks constructive: the stock sits just below the 50-day simple moving average (SMA), which had recently acted as support. Momentum indicators were neutral heading into earnings, and the shares were about 8.6% below the consensus price target of $46.12.

In the days after the report, Wells Fargo & Company reiterated an Equal Weight rating and raised its price target to $35 from $30. Barclays similarly lifted its target to $44 from $41 on Feb. 4.

For now, EXEL is in a consolidation pattern, but if the company's growth thesis proves correct, fresh all-time highs are plausible within the next 12 months.

Exelixis Is at an Inflection Point

Exelixis Is at an Inflection Point

The story isn't just about beating EPS or hitting revenue milestones. Exelixis is transitioning from a single-product company to a multi-franchise oncology player, and 2026 could be the year that shift becomes tangible.

The FDA decision on zanzalintinib in colorectal cancer (PDUFA date: Dec. 3, 2026) represents the company's first major expansion beyond cabozantinib. Approval would open the door to a potential $5 billion peak-sales opportunity and validate the franchise strategy Exelixis is pursuing.

A key signal is the company's R&D spending. Despite improved profitability, Exelixis is maintaining roughly $1 billion in annual R&D while also executing share buybacks — a sign of confidence in its pipeline. That spending supports seven pivotal trials for zanzalintinib alone, plus four early-stage programs advancing toward full development.

For context, the expanded GI sales team isn't just about NET (neuroendocrine tumor) growth; it's pre-positioning for a potential zanzalintinib launch later this year. The pieces are being put in place for a different biotech story: sustainable, multi-product growth anchored in deep tumor expertise rather than single, binary drug bets.

This email communication is a sponsored message sent on behalf of Eagle Publishing, a third-party advertiser of Earnings360 and MarketBeat.

If you need assistance with your subscription, please don't hesitate to email our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from Earnings360, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place #620, Sioux Falls, S.D. 57103. USA..