Hi there,

Our investment research analysts are going to be releasing their next investment idea tomorrow morning, around 10:00 AM Eastern time.

It will be first sent to subscribers that sign up to receive American Market News via SMS, then later in the morning to people who subscribe to our email newsletter or read our content on our website.

Don't miss out on your opportunity to be among the first to see our next stock idea. Our last idea was quite popular with our subscribers.

This is a free service from American Market News. If you want to take advantage of this unique research opportunity, just click the link below to be added to our priority distribution list.

Get Research Alerts from American Market News

Jessica Mitacek

Managing Editor

American Market News

Workday, Seriously, It's Time to Buy This SaaS Leader

Author: Thomas Hughes. Publication Date: 2/26/2026.

Key Points

- Workday is on track to hit multiyear lows amid a fear-driven sell-off; its stock oversold to deep value territory.

- AI disruption fears are overblown; this company is growing and cementing itself as an AI automation leader.

- Institutions buy as price action declines, and even analyst trends reveal the value.

- Special Report: [Sponsorship-Ad-6-Format3]

Workday's (NASDAQ: WDAY) stock decline didn't end with its Q4 2025 earnings report — it pushed to long-term lows, creating a more attractive buying opportunity. While guidance missed consensus and AI disruption fears persist, the miss was small, guidance remains solid, and disruption may not unfold as the market expects: not necessarily in the way investors fear.

AI-first companies may try to move into Workday's territory by turning models into full HR and finance software.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Incumbents like Workday are embedding AI into their existing platforms, and because they're already deeply integrated into enterprise workflows and data, they may be harder to displace than the market fears.

The analyst response to the earnings news was negative. Jefferies downgraded to Hold and several firms trimmed price targets, highlighting the abrupt CEO change: co-founder and Executive Chairman Aneel Bhusri is returning to lead the company through its next phase.

Workday Accelerates Growth and Profitability in Q4 2025

Workday had a solid quarter in Q4, with revenue growth accelerating sequentially to 14.5%. Revenue of $2.53 billion outpaced MarketBeat's consensus by 40 basis points, driven by subscriptions, which rose 15.7% year-over-year, and that strength carried through to the bottom line.

Margins were also strong: GAAP and adjusted operating margins widened by several hundred basis points. A 420-basis-point improvement in adjusted operating margin drove a 32% rise in operating income and a 28% increase in adjusted earnings — 650 basis points ahead of expectations.

Guidance was the sticking point: Q1 and full-year 2026 revenue forecasts missed consensus. However, the company still expects 13% topline growth in Q1 and 12.5% for the full year, with a robust adjusted operating margin. Price action may reset, but is unlikely to remain depressed. WDAY's consensus target sits roughly 100% above its key support levels, and even the low end of analyst ranges implies upside.

Institutional Support and Share Buybacks Underpin WDAY Rebound Outlook

Two factors supporting a potential rebound are capital returns and institutional support. Capital returns so far are entirely share repurchases, which steadily reduce the share count. 2025 repurchases trimmed the share count by about 0.4% — modest but meaningful for shareholder leverage — and institutions appear to be buying.

Institutional holders own over 90% of the stock and have been accumulating for seven consecutive quarters, including the first two months of Q1 2026. In Q1 2026 the ratio was roughly $1.15 bought for each $1 sold — modest, but trending bullish — and the pickup in buying to offset selling suggests institutions may continue to buy despite the "tepid" guidance.

Workday's balance sheet reflects capital returns, acquisitions, and growth investments but shows no red flags. Cash is healthy and roughly flat year-over-year. While current assets declined, total assets increased. Liabilities rose and equity contracted, but leverage remains light — roughly two times cash and below 0.5 times equity — giving the company flexibility to reduce debt and bolster equity through 2026.

Catalyst for Workday Stock: Yes, They Exist

Catalysts in 2026 include continued revenue growth, improving cash flow, and potential outperformance versus Q1 and full-year guidance. The company cautioned about macro uncertainty and longer deal-closing timelines. The likely path is for Workday to outperform quarterly results across the year, prompting guidance upgrades and a rebound in analyst and market sentiment. Trading near $115, WDAY sits in a zone not seen since the depths of the COVID-19 panic, so a rebound from these levels is plausible.

Diamondback Sees Resilient Demand Despite Cautious Guidance

Authored by Chris Markoch. Originally Published: 2/26/2026.

Key Points

- Diamondback Energy’s disciplined production outlook signals a supply environment that could help support higher oil prices into 2026.

- Strong free cash flow is funding dividend growth and share repurchases, reinforcing the company’s shareholder-return story.

- FANG stock remains technically constructive, with analysts projecting moderate upside as energy sentiment improves.

- Special Report: [Sponsorship-Ad-6-Format3]

Diamondback Energy Inc. (NASDAQ: FANG) stock has nearly recovered its pre-market losses after delivering its Q4 2025 earnings report on Feb. 23. The headline numbers were mixed — a slight earnings miss offset by a topline beat — and the company issued cautious guidance that likely tempered initial enthusiasm.

It's a reminder that investors reward companies that underpromise and then overdeliver, but only once the overdelivering actually occurs. Still, there was a lot to like in Diamondback's report, including a more optimistic view on the supply-demand outlook for crude oil in 2026.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Diamondback expects demand to remain resilient. At the same time, it provided a conservative initial read of 2026 guidance that keeps output roughly in line with the final three months of 2025. That forecast may not fully reflect the potential for higher crude prices in the months ahead.

Disciplined Production Could Support Higher Oil Prices

As of this writing, the April contract price of West Texas Intermediate (WTI) crude is $65.94 — about 20% higher than at the start of the year and roughly 40% higher than some analysts had expected.

Rising crude prices have buoyed the entire energy sector, but concerns about a supply glut still hang over producers. That makes Diamondback's emphasis on demand resilience notable: it suggests December 2025 may have helped establish a price floor for crude.

Several slides in Diamondback's presentation bolster the case for a sustained move higher in crude. First, the company's 2026 production guidance of 500–510 Mbo/d represents only modest growth from 2025, signaling a disciplined approach that could prevent supply from overwhelming demand.

Second, Diamondback's scenario analysis shows that even at $70 per barrel, the company expects to generate more than $5.5 billion in free cash flow. That indicates management views meaningful upside from current prices as a realistic base case, not a stretch target.

There's also a structural gas story that could indirectly support oil prices. Diamondback is expanding its long-haul gas pipeline commitments, raising its forecast from roughly 350,000 MMBtu/d today to 800,000 MMBtu/d by Q4 2026. That expansion should reduce the WAHA pricing drag that has historically hurt Permian producers' realizations. As that headwind fades, the economics of Permian production improve, reinforcing capital discipline across the basin. Fewer wells drilled industry-wide would tighten supply, which tends to push prices higher.

Dividend Growth Reinforces Long-Term Investor Appeal

The cyclical nature of energy — particularly oil — helps explain why many companies in the sector pay attractive dividends.

A highlight of Diamondback's report was a 5% increase in its quarterly dividend. That marks seven consecutive years of dividend raises for the company.

The dividend appears well supported by growing free cash flow (FCF).

Diamondback says the dividend is protected so long as crude oil prices remain above roughly $37 per barrel.

The company also repurchased about 2.9 million shares in Q4.

It has roughly $2.3 billion remaining on its authorized $8 billion share repurchase program.

Technical Indicators Point to Consolidation, Not Reversal

On Feb. 20 — the last trading day before the earnings report — FANG stock popped to its 52-week high, capping a rally that began at the start of the year.

That pattern has been common across energy stocks, which have been rangebound in recent years as demand lagged record output. As a result, even a small earnings miss could trigger a pullback.

Volume was slightly above average on the day, and the initial drop appeared driven by algorithmic trading; traders were buying the dip later in the session.

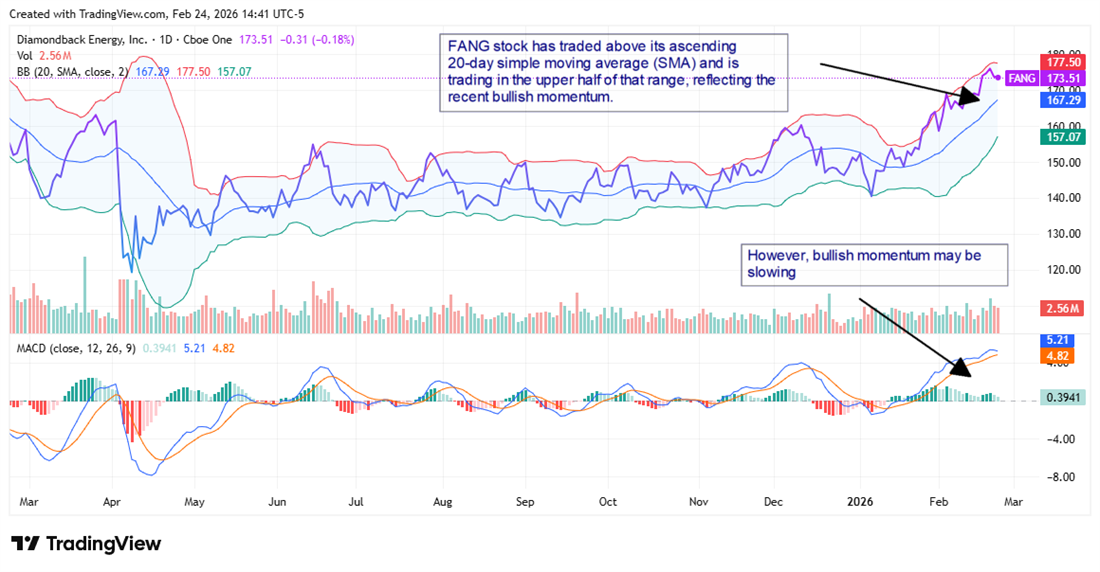

FANG has remained above its ascending 20-day simple moving average (SMA). The Bollinger Bands show the upper band at $177.50 and the lower band at $157.07; with the stock trading at $173.51, it sits in the upper half of that range, reflecting recent bullish momentum.

The moving average convergence/divergence (MACD) paints a broadly constructive picture: the MACD line at 5.21 remains above its signal line at 4.82, though the narrowing gap suggests near-term momentum may be fading. That could leave the stock vulnerable to a pullback toward the SMA — currently around $167.29 — before its next move.

The Diamondback Energy analyst forecasts on MarketBeat put the consensus price target at $187.33, about an 8% upside from the price at the time of writing. Sentiment has been bullish since the start of the year, and that continued after earnings when TD Cowen upgraded FANG to a Strong Buy.

This email message is a paid advertisement for American Market News, a third-party advertiser of The Early Bird and MarketBeat.

If you have questions about your subscription, don't hesitate to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl., Suite 620, Sioux Falls, SD 57103-7078. USA..