Attention retirees,

If you’re willing to be at your computer between 9 am and 10:45 am on most weekdays…

I can show you one simple trade that can potentially bankroll your retirement.

Hi… I’m Dave Aquino and I help everyday Americans go after their retirement goals sooner… by teaching them how to master the retirement trade.

The Retirement Trade is designed to be used every morning between 9am and 10:45am eastern time.

Why this window?

Well… I can’t share that information here…

But don’t worry because you’ll discover the exact reason why inside the free report you see pictured below…

And it’s yours - for FREE!

But please don’t delay, because it might not be free for long.

Just click here to claim it today...

Dave Aquino

Partner, Head of Options Trading

Base Camp Trading

Insiders Piled Into These 3 Stocks in Q4—One Stands Out

By Thomas Hughes. Posted: 2/17/2026.

Key Points

- Insider purchases accelerated in late 2025 across three names, with directors and executives adding exposure.

- One pick pairs heavy insider ownership with a tightly held float, which could amplify moves if commercialization ramps.

- The group includes a high-yield turnaround story, a steady med-tech compounder, and a speculative efficiency play.

- Special Report: [Sponsorship-Ad-6-Format3]

Insider buying was hot in Q4 2025, with money flowing into several underappreciated names. The question, as always, is whether these purchases signal genuine value investors should own or if executives are trying to support their share prices. In this case, insiders highlight value and opportunity across three stocks — and one stands out. Its technology is simple, effective, in demand, and potentially disruptive in a rapidly growing industry.

Tightly Held Alight Accumulated by Insiders

Alight (NYSE: ALIT) is a cloud-based employee engagement platform. Its services help employers and employees stay connected after onboarding, providing tools for scheduling, time-off requests, financial services and benefits administration. Insiders, including several directors, increased purchases throughout 2025, peaking in Q4. Insiders own roughly 2% of the shares — modest, but meaningful given the buying activity and the large institutional base. Institutions own most of the remaining shares and have been accumulating as well, absorbing available supply.

This makes me furious (Ad)

I Called Black Monday. Now I'm Calling March 26!

I predicted the 1987 crash six weeks early. I called the fall of the Berlin Wall. I pinpointed the exact bottom in 2009.

Now I'm staking my reputation on March 26, 2026 - the day I believe Elon will announce the SpaceX IPO.

Bloomberg is calling it "the biggest listing of ALL TIME."

A $1.5 TRILLION valuation... the "wealth-building" moment of the decade.

Today, I'll show you how to get in before the big announcement.

Short interest has pressured the stock. While institutions are buying, their activity hasn't been aggressive enough to fully offset short sales. Short interest has pulled back from its peaks but remains elevated, near 7%, which weighs on the share price. The company also faces tepid, uneven growth and relatively high debt. Offsetting those negatives are profitability and a high dividend yield — roughly 12% in early 2026 — driven by the depressed share price. The dividend appears sustainable versus the EPS outlook, which implies about a 28% payout ratio in 2026 with potential improvement thereafter.

Price action is choppy but hints at a possible rebound. Despite recent declines, volume has been rising and momentum indicators such as the MACD suggest bulls may be regaining control. Trading near $1.30, the stock sits below analysts' lowest targets, implying as much as 200% upside relative to consensus projections.

The Cooper Companies Insiders Affirm Growth Outlook

The Cooper Companies (NASDAQ: COO) doesn't pay a dividend, choosing instead to reinvest in growth. The outlook is modest but steady, with gradual revenue and earnings improvements that create value over time. A med-tech company focused on vision and women's health, Cooper saw insiders — including the CEO and several directors — buy about $2.6 million of stock in Q4 2025, bringing their holdings to roughly 3% of outstanding shares.

Institutions and analysts are also constructive. Institutions, which own about 24% of the stock, increased purchases through 2025 and appear on track to set another high in Q1 2026. Sell-side coverage is steady: analysts rate the stock a Moderate Buy, and price-target trends suggest roughly a 12% upside. A move of that size would place the share price near the midpoint of its long-term trading range and above key moving averages — a technical setup that could support further gains.

AirJoule: Technology Data Centers (and Other Industries) Will Need to Own

AirJoule Technologies (NASDAQ: AIRJ) makes dehumidification equipment, but its designs are far from ordinary. Their systems are roughly 75%–90% more efficient than traditional refrigerant-based units, delivering significant utility savings and much lower operating costs for a range of industries. While many sectors rely on humidity control, the data center industry is a particularly strong fit.

Data centers are proliferating, with top-tier 1-gigawatt facilities costing in the tens of billions (often starting near the $35 billion range), and their components are highly sensitive to humidity. Corrosion can cause catastrophic system failures, and condensation or stray droplets can disrupt optical data transmission.

Insiders — including the CEO, CFO and several directors — bought heavily in Q4 2025. That buying is noteworthy given insiders' ownership is in the roughly 40% range. At the same time, institutions own about 60% of the float, making the shares tightly held. Analysts' consensus rating is a Moderate Buy, with target ranges implying more than 100% upside at the low end and roughly 200% at the consensus target. Key catalysts should arrive as commercialization and sales scale later in the year.

MCD and TXRH: 2 Low-Risk Restaurant Stocks With Upside

Submitted by Dan Schmidt. Article Published: 2/17/2026.

Key Points

- The restaurant industry has become a key indicator for the K-shaped economy.

- Winners and losers are beginning to emerge based on the perceived value they offer to both higher-end and lower-end customers.

- McDonald's and Texas Roadhouse continue to grow comps despite the tough environment thanks to their value-oriented focus that keeps diners coming back.

- Special Report: [Sponsorship-Ad-6-Format3]

The restaurant sector has often been at the forefront of the debate on the K-shaped economy. While consumer sentiment continues to diverge from actual consumer behavior (especially in the retail sector), the food-service industry quickly reveals those split trends. The upper end of the 'K' keeps indulging, while more cost-conscious consumers at the bottom are searching for value to stretch their dollars.

In this environment, two chains stand out for different reasons. But the numbers speak for themselves: McDonald’s Corp. (NYSE: MCD) and Texas Roadhouse Inc. (NASDAQ: TXRH) continue to grow comparable sales and win market share from competitors. Below, we examine why these two have thrived in a challenging dining environment and why their stocks could outperform the restaurant industry this year.

McDonald's Continues to Dominate the Fast-Food Market

This makes me furious (Ad)

I Called Black Monday. Now I'm Calling March 26!

I predicted the 1987 crash six weeks early. I called the fall of the Berlin Wall. I pinpointed the exact bottom in 2009.

Now I'm staking my reputation on March 26, 2026 - the day I believe Elon will announce the SpaceX IPO.

Bloomberg is calling it "the biggest listing of ALL TIME."

A $1.5 TRILLION valuation... the "wealth-building" moment of the decade.

Today, I'll show you how to get in before the big announcement.

The recent earnings reports from McDonald's and Wendy’s Co. (NASDAQ: WEN) highlighted how fast-food players are separating themselves.

McDonald’s reported Q4 2025 results last week and beat both earnings-per-share (EPS) and revenue projections, delivering 9.7% year-over-year (YOY) sales growth.

Global same-store sales surpassed expectations with 5.7% YOY growth, including 6.8% growth in the United States. By contrast, Wendy’s Q4 2025 showed a 5.5% revenue decline and an 11.3% drop in U.S. same-store sales. How has McDonald’s managed nearly 7% U.S. sales growth while other quick-service restaurants struggle?

The answer comes down to value. McDonald’s projects operating margins above 40% in 2026, giving it the flexibility to execute a broad Value Leadership strategy.

Unlike the limited-time promotions used by Wendy’s and Burger King, McDonald’s Value Menu 2.0 is a permanent fixture. Extra Value Meals were reintroduced last September, and earlier this year the company launched the McValue platform, which includes $5 Meal Deals and Buy One, Get One for $1 offers. The Grinch Meal holiday promotion produced the biggest single-day sales figure in the company’s history.

Additionally, the McDonald’s app has roughly 200 million active users, driving repeat visits, and a marketing emphasis on chicken items such as the McCrispy helps mitigate beef-price inflation. The company also plans to open an additional 2,600 restaurants this year, while competitors like Wendy’s are closing underperforming locations.

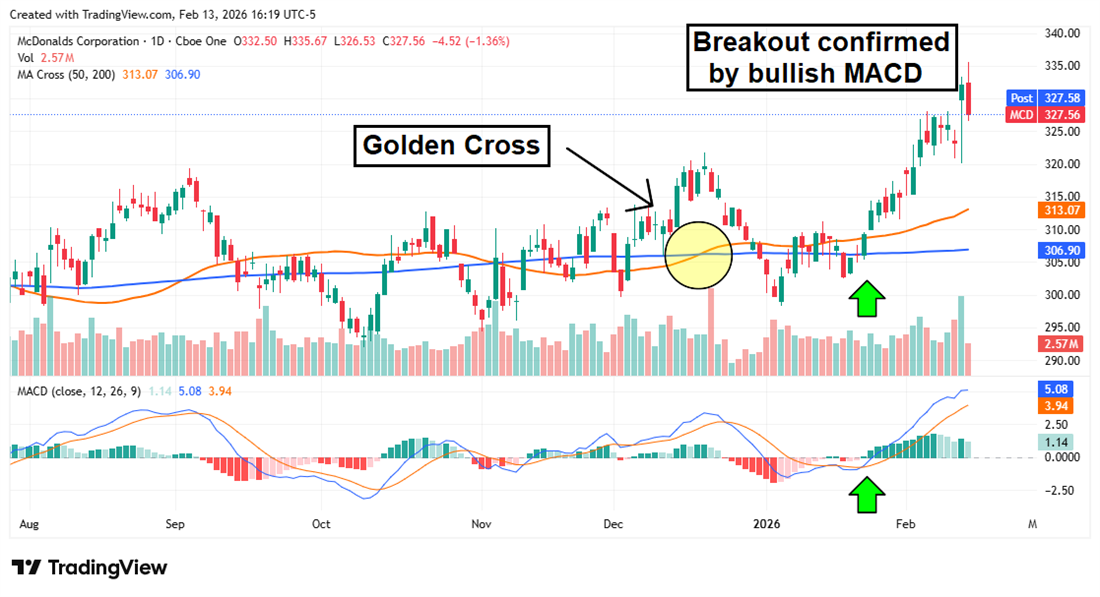

The breakout in MCD shares began well before last week’s earnings. A bullish crossover in the Moving Average Convergence Divergence (MACD) indicator coincided with the stock climbing above both the 50-day and 200-day simple moving averages (SMAs), signaling strong upward momentum. If lower-income consumers continue to trade down for value, McDonald’s is well-positioned to keep growing sales, with both fundamental and technical catalysts in 2026.

Texas Roadhouse Gains Share Despite Commodity Headwinds

Soaring beef prices have hung over Texas Roadhouse shares for much of the past year. Beef costs have risen faster than inflation since the COVID-19 pandemic, and the surge over the last two years has alarmed restaurant operators and investors.

The rise has been driven in part by cattle shortages that pushed live cow and steer prices to record levels, a situation likely to persist into 2027.

Despite that headwind, Texas Roadhouse continues to grow same-store sales faster than many casual-dining peers.

Its barbell business strategy supplies value to budget-conscious guests while offering premium steaks and add-ons for customers willing to spend more.

In a Q3 2025 report in November, the company reported comps of 6.1% and nearly 13% YOY revenue growth despite a 224-basis-point increase in food-and-beverage costs. Texas Roadhouse raised prices by only 1.7%, a deliberate margin concession designed to retain value-oriented diners.

Customer experience is central to the chain’s success. Traffic durability matters for fast-casual and casual-dining concepts that rely on repeat visits. Large portions, quick service, streamlined digital kitchens, and numerous add-ons give Texas Roadhouse the feel of a special night out without breaking the bank. Customers often report that the restaurant is “worth it” for date nights and family dinners because the value and experience meet expectations.

TXRH’s performance so far this year suggests the doldrums of 2025 may be behind it. The stock rose 11 days in a row to open 2026, breaking through the 200-day SMA that had blocked previous breakout attempts. That streak was followed by a consolidation in which the Relative Strength Index (RSI) cooled to more neutral levels while the 50-day and 200-day SMAs converged.

With a Golden Cross appearing imminent, the 50-day SMA could act as support for a renewed rally. That level has already been tested once and held, and the share price is now approaching the 50-day moving average. This may be an attractive entry point for new investors, particularly with a catalyst coming when the company reports its Q4 2025 results after the market close on Feb. 19.

This email content is a sponsored email for Base Camp Trading, a third-party advertiser of MarketBeat. Why did I get this email?.

This promotional message is sent on behalf of Base Camp Trading, located at 5540 Centerview Drive, Suite 204, Raleigh, NC 27606. If you no longer wish to receive promotional emails from Base Camp Trading, please unsubscribe here with the "optout" in the subject line.

If you have questions or concerns about your subscription, please feel free to contact our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl. #620, Sioux Falls, SD 57103-7078. United States of America..