It’s disgraceful.

The United States, a country that once stood for personal freedom, yet demanded personal responsibility from its citizens and politicians alike, is broken.

I barely recognize it anymore.

Since 2010, I’ve been warning everyone who would listen about the United State’s looming debt crisis in my documentary, The End of America.

Now, 16 years, and $22 trillion in additional debt later…

We’re very near the $40 trillion mark in total national debt:

This massive debt… annual deficit increases… along with looming unfunded pension obligations, are spiraling this country toward insolvency.

And as I’ll show you, the soaring price of gold right now is a very clear warning of this.

Congress cannot possibly finance its legislatively mandated spending:

Mandatory spending plus interest is locked in at around 37% of GDP before a single discretionary dollar is spent.

It’s inevitable that the government will be forced to print trillions of dollars to finance its growing obligations and borrowing costs.

This has the potential to trigger a technical U.S. Treasury default… which would mean catastrophic losses for long-duration bond investors.

It’s happening right now in Japan, where the 10-year bond yield has tripled over the last year. It has cost investors over $200 billion.

And that’s what happened in Great Britain in September 2022, costing investors around $700 billion.

In both cases, the bond markets sold off after the governments announced plans to both increase spending and cut taxes. Following the same logic at home…

I believe it’s now certain America will soon experience a financial reckoning, much like we saw in 1973-1974.

After the U.S. abandoned the gold standard in August 1971, Congress passed huge increases to spending, including linking Social Security payouts to meet the inflation rate.

In the 10 years following the August 1971 break with gold, the size of the Federal Reserve’s balance sheet grew 174%, from $70 billion to over $190 billion, as it bought enormous amounts of Treasury bonds with newly printed money.

This set off the roaring inflation of the 1970s, which wiped out long-duration Treasury bonds.

That meant a stock market decline of more than 50% between 1973 and 1974. The sell-off in financial stocks was even more intense.

For banks, which must hold Treasury securities as reserves, the technical default (printing money to finance government debt) was catastrophic.

The price of gold, in the meantime? Soared from $35/ounce to $455 by the end of the decade. That should sound familiar…

Today, we’re witnessing the largest gold bull run since the 1970s, and for an important reason:

Central banks around the world are recognizing this massive risk that U.S. Treasury bonds pose to their bottom line. So they’re dumping Treasuries… and buying gold hand-over-fist.

Put simply, gold is money again. And it’s the greatest monetary shift we’ve ever seen.

I warned anyone who would listen to get into gold over a year ago. And I’d bet the ones who did are enjoying some incredible returns.

But this is just the beginning of this wealth shift - and I have a new gold recommendation that I believe everyone should consider immediately.

In short, if you don’t own gold right now, you’re making a big mistake. But if you really want to protect and potentially grow your wealth during these dangerous times…

Click here to see the absolute best way to invest in this global gold rush right now.

Good investing,

Porter Stansberry

United Parcel Service Transitions to Growth: Accumulation Begins

Written by Thomas Hughes. Date Posted: 1/28/2026.

In Brief

- United Parcel Service has returned to growth sooner than expected, and its stock price looks to be in rebound mode.

- An ample capital return is reliable in 2026, with distributions expected to increase.

- Analysts and institutional data align with a market bottom and reversal, and trends will likely strengthen as 2026 progresses.

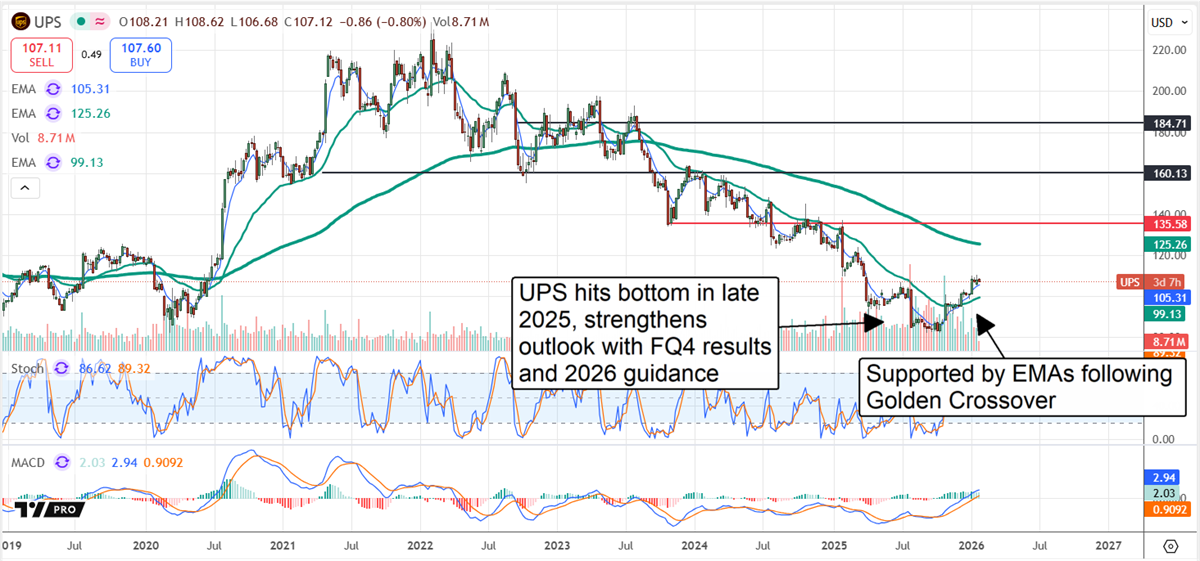

The long-awaited bottom in United Parcel Service (NYSE: UPS) stock appears to be in, and the rebound is underway. Backed by solid results, improving operational quality and a growth-oriented outlook, the rebound could be substantial for long-term holders. After a period of heavy distribution and downward pressure from analysts, UPS is back in an accumulation posture that is likely to strengthen as the year progresses.

Analysts and Institutions Have Shifted to Bullish

The shift is evident in recent analyst activity. The analyst group still carries a consensus Hold, but analysts began raising price targets in late 2025 and continued to revise estimates higher into early 2026.

What a Roth Conversion Makes Permanent (Ad)

Firing Your Financial Advisor: The 5 Major Red Flags

Many investors miss these warning signs.

That momentum accelerated once UPS released its 2026 guidance.

The company is forecasting $89.7 billion in net revenue, roughly 300 basis points above MarketBeat's consensus, implying growth a year earlier than previously expected. Margins are also expected to remain healthy, suggesting the potential for an outsized earnings rebound.

Institutional activity has also turned constructive. Institutions own about 60% of this high-yielding stock and, on balance, were net buyers in Q4 2025. While there were institutional sales earlier that coincided with the stock's low, a late-quarter shift back to accumulation extended into January 2026 and appears likely to continue. Combined with the Q4 strength and the 2026 guide, this supports a reliable capital-return program for investors.

Dividend Strength and Buybacks Reward Investors

Trading near COVID-19-era lows, the stock yields more than 6% and is expected to sustain dividend increases over the coming years. UPS' 2026 guidance implies payments slightly above 2025 levels, consistent with another low-single-digit raise. Share buybacks reduced the share count by roughly 0.7% in 2025 and are expected to continue trimming the float in 2026.

UPS Accelerates Stock Reversal With Strong Results

UPS delivered a solid Q4 despite reporting a modest net contraction.

Revenue declined 3.2%, but the shortfall was smaller than expected — the company beat revenue estimates by nearly $500 million. Strength in revenue per package and international markets offset weakness in domestic volume and supply chain solutions.

Adjusted operating margin contracted as expected and aligned with forecasts, leaving adjusted earnings above consensus by a similar margin.

For investors, the opportunity is to enter early in this rebound. The outlook for earnings, the potential for outperformance and the shift in analyst sentiment all point to a cycle of outperformance and upward revisions ahead.

In that scenario, UPS stock could move to the high end of the early-2026 target range — a rally of roughly 40% from the pre-release close — as upgrades and bullish price-target revisions drive demand.

UPS Advances Following Strong 2026 Guide

UPS stock ticked higher after the 2026 guide, showing support near its 30-day exponential moving average (EMA). That EMA has been climbing alongside the 150-day EMA following a Golden Cross in December 2025. This technical signal, together with visible accumulation, suggests a solid support base. If the EMA cluster continues to hold, a more substantial price rebound could follow.

Key catalysts for 2026 include persistent revenue growth, margin recovery and operational outperformance. UPS' push into digitization, automation and AI should pick up steam and compound improvements in business quality. The decline in Amazon-related volume is expected to stabilize as the business mix shifts toward higher-margin consumer and commercial traffic. Industry focuses such as healthcare — where UPS targets specialized, time- and temperature-sensitive solutions — are also expected to add high-quality, higher-margin revenue streams.

This email content is a sponsored message provided by Porter & Company, a third-party advertiser of DividendStocks.com and MarketBeat.

If you have questions or concerns about your subscription, feel free to contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 North Reid Place, Suite 620, Sioux Falls, SD 57103-7078. United States of America..