Thanks for joining DividendStocks.com, the daily newsletter built for dividend and income investors like you. We’re thrilled to have you on board and can’t wait to help you discover the best dividend opportunities out there. Before we can start sending your daily insights, please take a quick moment to confirm your subscription: Click Here to Confirm Your Subscription to DividendStocks.com Here’s a small glimpse of what you’ll get access to: Dividend Stock Ideas — Each newsletter features dividend stocks with high yields, sustainable payouts, and strong growth potential. Ex-Dividend Stocks — Want to capture upcoming dividend payouts? Find out which stocks are going ex-dividend this week. Market News and Events — Stay in the loop on the latest developments impacting popular dividend names like AT&T, Exxon Mobil, IBM, Procter & Gamble, and Verizon. Bonus: As a thank-you for confirming, you’ll also receive a free PDF copy of Automatic Income, our popular guide to building wealth through dividend investing. Why wait? Let’s get your dividend journey started! Click Here to Start Discovering Top Income-Generating Stocks See you in your inbox soon,

The DividendStocks.com Team P.S. Don’t miss out click here to verify your subscription and secure your daily dividend insights and your free investing guide!

Just For You These 3 Stocks Trade at Discounts the Market Won't Ignore ForeverReported by Dan Schmidt. Article Posted: 1/5/2026.

Key Points - The S&P 500 posted another gain above 15% in 2025, but the market is now approaching historically concerning valuation levels.

- When valuations are elevated, slowing earnings growth is harshly punished, and investors often turn to value stocks for safety.

- These three large-cap stocks all trade well below their industry-average P/E ratios, which could help protect against market volatility in 2026.

The S&P 500 wrapped up 2025 with a total return of about 18% — the third straight year above historical norms, but below the gangbusters 25% returns of 2023 and 2024. AI euphoria remains the dominant market theme entering 2026, and usual suspects like NVIDIA Corp. (NASDAQ: NVDA) and Alphabet Inc. (NASDAQ: GOOGL) rose again on the first trading day. If you've ridden the AI rally since the market bottomed in 2022, you're likely sitting on substantial gains and may feel compelled to diversify, especially with a tech-heavy allocation. The S&P 500 is entering the year trading at about 26x forward earnings, well above its 20-year average of 16x. When valuations are this elevated, investors demand outsized earnings growth, and high-multiple stocks can fall out of favor quickly if growth slows even a little. If rates remain high, 2026 could be the year value investing stages a comeback. A strange investment indicator discovered nearly a century ago has reappeared — and analysts say its warning couldn't come at a more critical time. While many investors believe the worst of the volatility is behind us, this signal suggests a far more significant market shift may be forming.

According to historical patterns, certain types of stocks tend to bear the brunt of this transition. Weiss analysts have highlighted five companies that may be especially exposed if the current trend accelerates. See the 5 stocks analysts say to avoid now Below, we look at ways to de-risk a portfolio by adding stocks that enter the new year undervalued and overlooked. Each company discussed here trades at a substantial valuation discount to its industry average, but fundamental and technical tailwinds suggest those discounts may not persist. Comcast: Strong Balance Sheet and Sports Expansion Enhance Outlook Comcast Corp. (NASDAQ: CMCSA) was one of the biggest victims of the cord-cutting revolution, as customers fled expensive cable packages for a la carte streaming services. A lost decade is every investor's worst nightmare — CMCSA is about five months from completing that milestone, trading around the same price it did in May 2016. Now, however, customers appear to be experiencing cord-cutting fatigue: streamers are raising prices and getting into costly disputes with major networks. Meanwhile, Comcast has quietly built a sturdy balance sheet and diversified revenue streams. Its forward price-to-earnings (P/E) ratio of 6.84 is well below the communications industry average (16.5) and far cheaper than major competitors like The Walt Disney Co. (NYSE: DIS) and AT&T Inc. (NYSE: T).

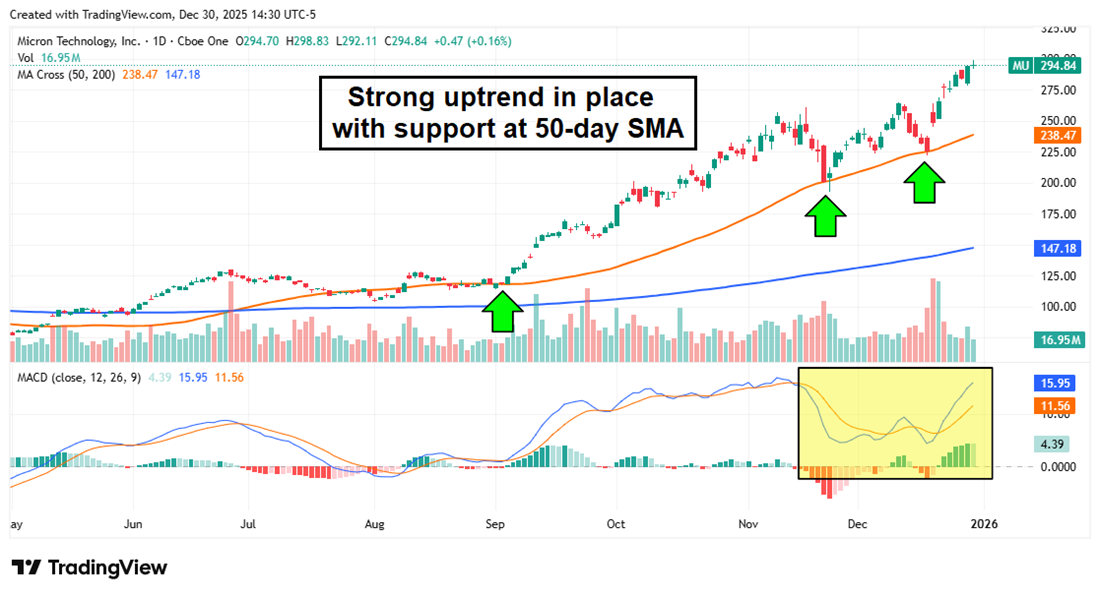

Comcast's broadband business is a steady, high-margin cash-flow engine. Despite Connectivity and Platforms revenue slowing 1.4% year-over-year (YOY) in Q3 2025, EBITDA margins for the residential and business segments were 37% and 56%, respectively. The advertising business should also benefit in 2026, as NBCUniversal holds rights to Super Bowl LX, the FIFA World Cup, and the Winter Olympics in Italy. The company generated $4.9 billion in free cash flow in Q3, supporting its 4.4% dividend. Comcast's value story may be gaining attention: the stock is up nearly 10% over the past 30 days, and several technical indicators point to potential further upside. Micron: An Essential AI Stock Trading at a Deep Discount How can a stock that just posted a roughly 200% year still look undervalued? Despite its parabolic 2025, Micron Technology Inc. (NASDAQ: MU) remains one of the more reasonably valued players in the AI ecosystem, trading at about 29x earnings versus roughly 75x for the broader tech sector. A P/E of 29 isn't cheap relative to the broader market, but it looks attractive for a company generating roughly 57% year-over-year quarterly revenue growth, maintaining strong gross margins, and consistently raising guidance.

Memory companies are high-margin businesses, and Micron has said it is struggling to keep up with insatiable data-center demand. The chart shows a solid uptrend with support along the 50-day simple moving average (SMA). This aligns with the TradeSmith Health indicator, which currently places MU shares in the Green Zone, indicating a robust trend with healthy pullbacks. Pfizer: Fueling Pipeline Innovation Through Acquisitions Shares of healthcare giant Pfizer Inc. (NYSE: PFE) have lagged since the COVID-19 pandemic receded; the stock is down more than 30% over the past five years. Competitors such as Eli Lilly and Co. (NYSE: LLY) have outpaced Pfizer with obesity drugs like Mounjaro. Pfizer now trades near historical low valuations (about 8.4x forward earnings), considerably cheaper than most large-cap pharma peers. The company's Seagen acquisition is beginning to pay dividends in oncology, adding more than $6 billion in revenue since the deal closed in 2023.

Although Pfizer's pivot into the obesity-drug market has been gradual, its pipeline has been strengthened by acquisitions of two smaller firms offering oral and injectable treatment options. The market has largely discounted Pfizer's prospects in this space, which helps explain the valuation gap. Low expectations can create opportunities — the stock doesn't yet reflect the potential for Pfizer to capture meaningful share of the GLP-1 market. Pfizer also offers defensive qualities due to its low valuation and a history of dividend growth.

|