|

The Biotech Toll Booth Quietly Printing Royalties |

|

|

Some biotech stocks live and die by a single data readout. This one doesn't. It gets paid when its partners succeed, and right now those wins are stacking up. |

|

|

|

Smart Money (Sponsored) | | | Bank of America increased its position 197%.

Swiss National Bank disclosed a new stake.

What do they know?

They're buying AI infrastructure companies: | Connectivity chips (64% gross margins)

Voice AI technology (217% revenue growth)

Data engineering services (margins up from 9% to 23%)

| Discover which 3 stocks they're buying

(By clicking this link you agree to receive emails from Trading Tips and our affiliates. You can opt out at any time. - Privacy Policy) |

|

|

|

|

|

Halozyme Therapeutics, Inc. | | December 30 – Pre‑market

Ticker: HALO | Sector: Biotechnology/Healthcare | Market Cap: ~$8.1B |

|

|

|

30‑Second Take |

This is a classic "the hits keep coming" setup. |

Halozyme just picked up US FDA approval for RYBREVANT FASPRO, an ENHANZE-enabled therapy targeting advanced EGFR-mutated non-small cell lung cancer, extending its platform deeper into oncology where pricing power and durability matter most. |

At the same time, a German court issued a preliminary injunction protecting Halozyme's ENHANZE patents against a rival product, reinforcing the moat around its royalty engine. |

This one-two punch matters. It shows Halozyme can both expand ENHANZE into new high-value indications and actively defend the royalty stream that underpins its cash flow. |

The business is de-risking in real time, and the market is still catching up to how valuable that combination really is. |

|

Trade Setup |

Time frame: 6–12 months

Edge type: Platform re-rating with royalty compounding |

This is a patience-rewarding setup rather than a quick biotech pop. |

You're buying into a proven platform that keeps stacking approved products, expanding royalties, and reducing downside risk. |

As Halozyme continues to look less like a speculative biotech and more like a durable growth business, the market's willingness to pay up for that consistency is the real edge. |

|

|

|

Poll: Which would you rather have? |

|

|

Numbers at a Glance |

Metric | Value | Current Stance |

|---|

Price | $68.93 | Above average |

|---|

52‑week range | $47.50 - $79.50 | Above average |

|---|

Short interest | 10.95% | Below average |

|---|

Next catalyst | Partner momentum and pipeline proof | |

|---|

|

|

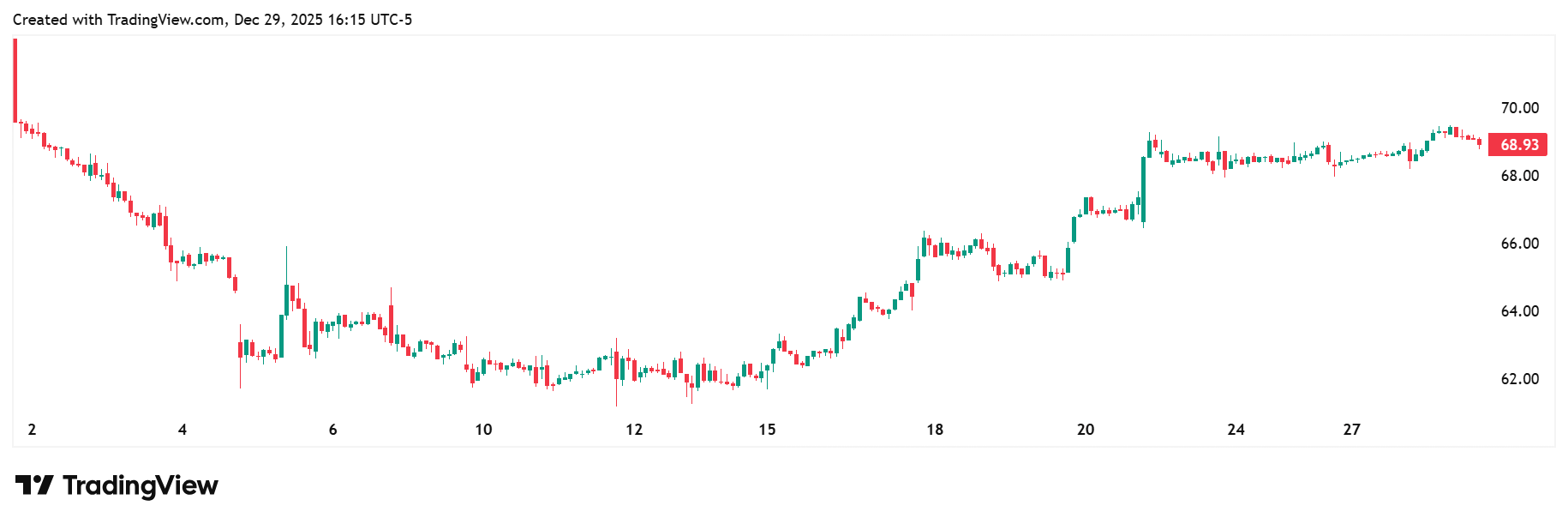

Chart |

|

1-month trading summary: Let's be honest. The stock is down a little over 3% on the month, so this hasn't been a straight-line march higher. |

But the pullback matters less than how it's happened. |

Selling pressure showed up early, cooled off quickly, and then gave way to a steadier grind as the stock found support in the low-to-mid $60s. |

Since then, price action has looked more like a pause than a panic. |

Volumes have stayed muted, downside follow-through has been limited, and buyers have quietly stepped back in as the story improved. |

This is what digestion looks like after a prior run, not a stock falling apart. |

|

Bull Case |

A toll booth, not a gamble: Halozyme isn't betting the company on a single binary drug readout. That's the key distinction. |

Instead, it owns a toll-booth business model through its ENHANZE platform, collecting high-margin royalties from a growing roster of partnered drugs that are already approved, already selling, and still scaling. |

This shifts Halozyme out of the "hope and hype" biotech bucket and into something far more durable. |

Partners fund development, commercialization, and sales while Halozyme captures recurring economics with limited incremental cost. |

As more ENHANZE-enabled therapies move into oncology and other high-value indications, operating leverage quietly compounds. |

It's a business built to grow without swinging for the fences. |

Royalties, range, and reinforced moats: HALO's toll-booth model is firing on multiple cylinders right now. |

The recent FDA approval of an ENHANZE-enabled oncology therapy extends the platform into another large, durable cancer indication, reinforcing Halozyme's relevance in areas where treatment adoption tends to stick. |

At the same time, the court ruling protecting ENHANZE patents sends a clear signal to would-be competitors: this royalty stream is defended. |

Each new approval adds incremental revenue, and each legal win strengthens pricing power and longevity. |

The result is a compounding catalyst stack rather than a single headline moment, precisely what you want to see as a long-term growth investor. |

Price targets: Price targets span from $56.00 to a high of $92.00. |

Support, structure, and patience: From a technical standpoint, this chart is doing more right than wrong. |

After the early-month dip, the stock carved out a clear base in the low-to-mid $60s and has since worked its way back toward the top of the recent range. |

That ability to stabilise, rather than cascade lower, is a quiet but essential tell. |

If the broader action cooperates, the technical setup supports a move higher without needing anything dramatic to go right. |

|

Bear Case |

Could the royalty engine stumble? The most significant risk here isn't a failed trial or a surprise FDA rejection. It's something quieter. Halozyme's strength is also its vulnerability. |

The business depends on partners continuing to grow sales of ENHANZE-enabled drugs. |

If adoption slows, pricing comes under pressure, or partners shift focus to alternative delivery technologies, royalty growth could disappoint even if nothing "goes wrong" operationally. |

There's also a concentration risk to respect. A handful of major products drive a meaningful share of revenue, so any stumble by a key partner can ripple through results. |

This isn't a reason to avoid the stock, but it is a reminder that this is still a platform story, not a guaranteed annuity. |

Good science, shakier economics: Halozyme doesn't compete in the usual biotech knife fight. Its real competition comes from alternative drug-delivery technologies and internal solutions developed by big pharma. |

Names like Amgen, Pfizer, and Roche all have the resources to build or buy their own delivery platforms if they choose. |

The difference is economic discipline. |

Most competitors are still spending heavily to prove their tech works or justify internal investment, while Halozyme is already cash-flowing from approved products. |

That gives it a timing advantage. |

Still, if a cheaper or more flexible delivery solution gains traction, some partners could eventually look elsewhere. |

This isn't an immediate threat, but it's the competitive pressure that sits quietly in the background, keeping this from becoming a permanent monopoly. |

Biotech still needs to behave: Even high-quality biotech doesn't trade in a vacuum. If risk appetite fades, rates rise, or the market swings back into a risk-off mood, Halozyme can get dragged lower with the group, regardless of fundamentals. |

Platform stories tend to hold up better than binary names, but they're not immune to sector-wide multiple compression. |

There's also the reality that healthcare policy noise never really goes away. |

Pricing pressure, regulatory scrutiny, and shifting reimbursement dynamics can spook investors fast, even when the underlying business is executing. |

Consensus creeping in: As Halozyme continues to execute and the royalty story becomes easier to understand, more generalist investors are starting to show up. |

That's good for validation, but it can cap upside in the short term if expectations run ahead of results. Not a red flag, just something to keep an eye on. |

|

Quick Checklist |

✅ Thesis still valid after today's close

✅ Volume confirms move above key levels

✅ Catalyst date double-checked (December 29, 2025) |

|

Deep‑Dive Links |

|

|

That's all for today's Everyday Alpha. We'll have a new pick for you every morning before the market opens, so stay tuned! |

Best Regards,

—Noah Zelvis

Everyday Alpha |