Welcome! Thank you for subscribing to the Earnings360 newsletter, your daily source for quarterly earnings news and updates.

Each morning edition contains a wrap-up of today's pre-market earnings announcements and yesterday's earnings announcements after the closing bell.

Please take a moment to confirm your subscription below so we can ensure these updates reach your inbox.

Confirm Your Subscription Here

The Earnings360 Team

For Your Education and Enjoyment 3 Under-the-Radar AI Stocks to Buy on the DipWritten by Dan Schmidt. Published 11/15/2025.

Key Points - Markets have been volatile over the last few weeks, and some stocks have pulled back from previous highs.

- Despite this pullback, the long-term AI uptrend still looks promising, and data center spending continues to reach unprecedented levels.

- These three AI-related stocks could be great 'buy the dip' opportunities for investors who missed the initial rally.

Investors have been conditioned to buy dips since the Global Financial Crisis, a belief reinforced by aggressive government support during the COVID-19 pandemic. The 2018 bear market? Buy the dip. A new virus shutting down the economy? Buy the dip. The Fed starts raising rates? Buy the dip. Disruptive tariff policies? Buy the dip. There may come a day when buying the dip is a poor strategy, but recent corrections and bear markets have offered attractive chances to purchase assets at a discount. Gold has surged past $4,200 an ounce — up sharply over the past year — but Sean Brodrick of Weiss Ratings believes this move could still be in its early stages. After three decades tracking precious metals, he says past gold surges have often been overshadowed by a different type of opportunity that historically delivered far stronger returns than simply holding physical gold.

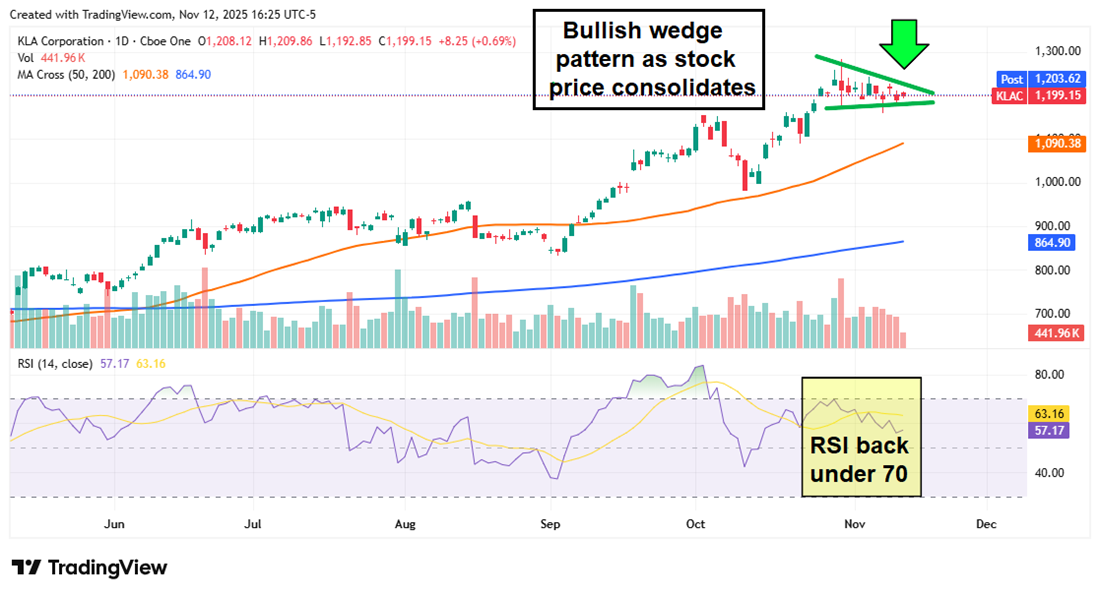

Sean now believes that pattern may be setting up again, and the strategy behind it doesn't require buying gold coins or bars. For a limited time this weekend, investors can access his full research — including the approach he says could benefit most if this gold cycle continues — for just $19 as part of a special offer. Click here to see how you could benefit before the offer expires Today, artificial intelligence dominates market headlines, and the capital expenditure for AI buildouts is staggering. There's no greater example than NVIDIA Corp. (NASDAQ: NVDA), which surpassed a $100 billion market cap in early 2019 and today is on the cusp of becoming the first $5 trillion company in the history of capitalism. While hyperscalers and chipmakers attract the most attention, under-the-radar tech companies are starting to offer better rewards to investors. This recent volatility presents an opportunity to buy the dip in these less-heralded but still profitable names. Below are three companies at the forefront of their industries that address critical AI bottlenecks in quality control, thermal management, and CPU design. KLA Corporation: A Stranglehold on Process Controls As chips shrink and pack more transistors, quality control becomes increasingly crucial. Manufacturing advanced AI chips requires tight tolerances—tiny nanoscale defects can render a high-yield semiconductor useless. The cost of producing defective chips far outweighs quality-control costs, so the technology offered by KLA Corp. (NASDAQ: KLAC) is essential for chip manufacturers serving data-center clients. KLA's inspection suite checks chips throughout the manufacturing process, ensuring each layer and structure is fabricated correctly. The company manufactures, installs, and provides field support for its systems—generating recurring revenue. A major catalyst for KLA is the growth of advanced packaging, which integrates multiple semiconductors into a single device. Advanced packaging improves performance but creates more intricate designs that demand additional quality control. In its fiscal Q1 2026 report, KLA management forecast $925 million in revenue from advanced packaging services, a 70% year-over-year increase.

Despite these fundamental tailwinds, the stock has pulled back from its late-October all-time high and is consolidating in a wedge pattern. A breach of the upper trendline typically signals the next leg of a rally. With the Relative Strength Index (RSI) back under 70, a breakout could be imminent. ARM Holdings: Next-Gen Designs for Next-Gen AI ARM Holdings plc (NASDAQ: ARM) has lagged larger peers such as NVDA, but the British semiconductor designer plays a unique and powerful role in the AI ecosystem. ARM doesn't manufacture chips; it licenses intellectual property to customers that build chips themselves. ARM's Neoverse platform continues to gain traction, reaching about 25% penetration of the data-center CPU market earlier this year. In its fiscal Q2 2026 earnings release last week, ARM reported year-over-year revenue growth north of 34% and added several megacap hyperscalers—such as Meta Platforms Inc. (NASDAQ: META)—as customers for custom silicon.

Despite record revenue, ARM shares have had a rocky 2025 and have yet to reclaim the all-time high set in July 2024. After flashing a Golden Cross this summer, the stock recently dipped below the 50-day simple moving average (SMA) for the first time since September. The 200-day SMA has historically provided support and could be the actual support area now. The RSI also hints at a potential short-term bottom, so watch for a reversal off the 200-day SMA as a possible entry signal. Vertiv Holdings: Innovators in Cooling Technology Data centers produce massive heat, requiring sophisticated cooling to prevent damage and premature obsolescence. Vertiv Holdings Co. (NYSE: VRT) is an innovator in electrical thermal management, and its liquid-cooling systems will be critical infrastructure as data centers scale up. A single AI rack can consume power comparable to that of 100 households. As power density rises, traditional air-cooling becomes less effective. Vertiv says its liquid-cooling solutions are 3,000 times more efficient than conventional systems, and the addressable market for its technology is expected to grow at roughly a 20% CAGR through the decade.

Despite an impressive Q3 2025 earnings beat and raised guidance—including a $9.5 billion order backlog for 2026—the stock has pulled back from its post-earnings high. That pullback likely represents profit-taking after a strong run (long-term holders are up more than 50% year-to-date). The company has numerous fundamental tailwinds, and the technical trends also look promising. Following a July Golden Cross, the stock has used the 50-day SMA for support, and the price appears headed back to that level after an Overbought signal on the RSI. The long-term uptrend remains intact, and the 50-day SMA could serve as a reasonable entry point for new positions.

|