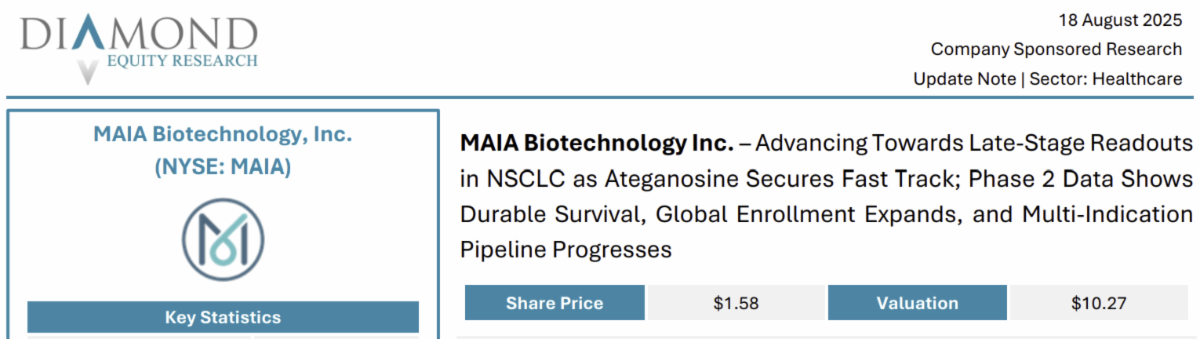

| From MAIA's closing valuation on Thursday, this $10.27 target suggests an upside potential of over 500%!

Critical Report Info:

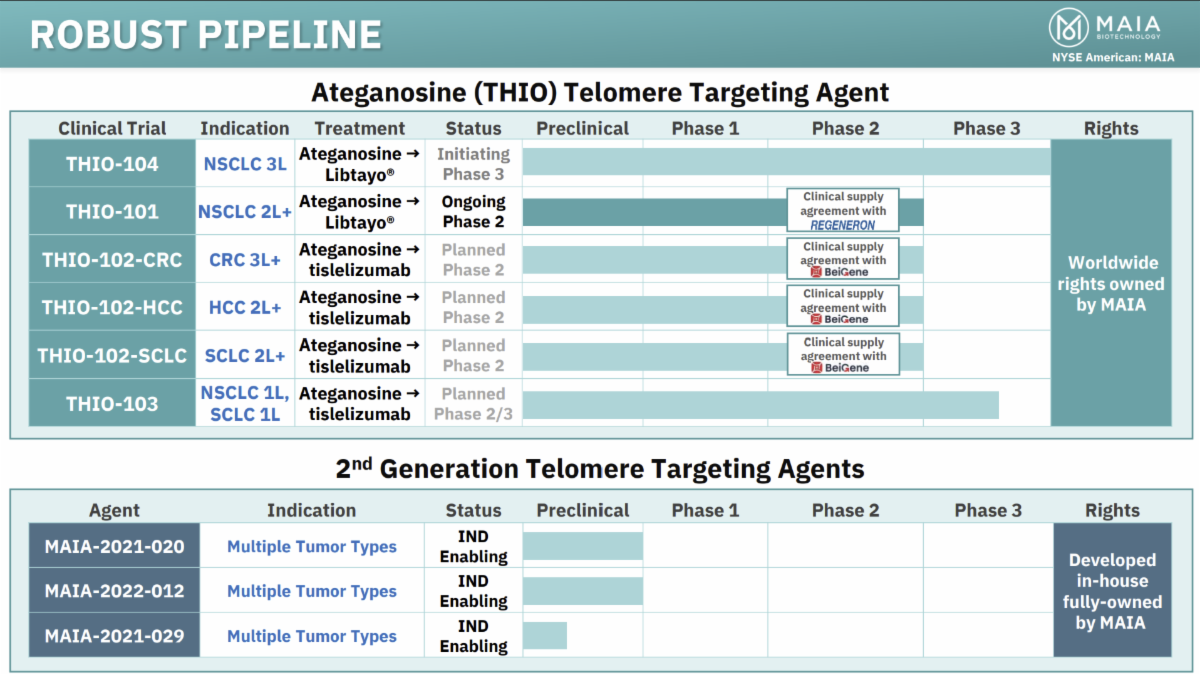

Valuation: Recent updates further de-risk the THIO program in third-line NSCLC. The Phase 2 THIO-101 dataset now shows a median overall survival of 17.8 months in the intent-to-treat cohort with a generally tolerable safety profile, and a confirmed partial response after 20 months of therapy supports durability. Fast Track designation for ateganosine in NSCLC and a master clinical supply agreement with Roche to evaluate the THIO–atezolizumab sequence enhance the regulatory path and partnering visibility. We continue to expect initiation of the pivotal THIO-104 study in the second half of 2025 with an accelerated approval filing targeted for 2026, contingent on THIO-101 outcomes, while planned multitumor studies expand the addressable opp. We have revised our valuation model to incorporate the most recent financial results, updated share count, and re-evaluated the comparable company analysis, yielding a valuation of $10.27 per share, contingent on successful execution by the company.

#2. A Major Analyst Target Suggest Serious Upside Potential (Triple-Digit!).

Noble Capital Markets - $14.00 Target - (Potential upside of 800+% from Thursday's close.)

Key Report Details:

Conclusion. Roche becomes the third pharmaceutical company to make a supply agreement with MAIA to test a checkpoint inhibitor in combination with THIO. We believe this shows that potential partners have noticed the data showing improved overall survival (OS), progression free survival (PFS), and the side effect profile. Clinical data from the three of the eight approved checkpoint inhibitors could make bidding for a marketing partnership more competitive. We are reiterating our Outperform rating and $14 price target.

#3. MAIA Has A Relatively Low Float (Volatility Potential May Be Explosive).

Sporting a float of roughly 28.34Mn shares, according to Yahoo Finance, volatility potential could pop up in a flash.

#4. MAIA Biotechnology Expands Global Leadership With European Cancer Therapy Patent.

MAIA Biotechnology, Inc. achieved a major milestone with the European Patent Office granting protection for its novel telomere-targeting anticancer agents.

This new patent covers ateganosine-based analogues, designed to disrupt telomeres, halt cancer cell growth, and enhance anticancer activity with higher specificity.

The innovation strengthens MAIA’s intellectual property portfolio across Europe, securing rights in 19 countries.

#5. MAIA Achieves Fast Track FDA Designation For Ateganosine Lung Cancer Therapy.

MAIA Biotechnology, Inc. received FDA Fast Track designation for ateganosine (THIO) in treating non-small cell lung cancer (NSCLC), a $34Bn market with significant unmet need.

Ateganosine, a first-in-class telomere-targeting molecule, disrupts cancer cell survival and enhances immune response.

This designation accelerates potential FDA approval, strengthening MAIA’s competitive edge.

If approved, ateganosine could reach market, advance cancer care, and secure exclusivity, underscoring MAIA’s pioneering role in innovative oncology treatments.

#6. MAIA Expands Global Phase 2 Trial Advancing Ateganosine Lung Cancer Therapy.

MAIA Biotechnology, Inc. announced the dosing of the first patient in Taiwan for the expansion of its pivotal Phase 2 THIO-101 trial, advancing ateganosine (THIO) for advanced non-small cell lung cancer (NSCLC).

This milestone extends the study’s reach across Asia and Europe, broadening access to a larger patient pool.

Interim results show ateganosine delivers a median overall survival of 17.8 months in heavily pre-treated patients—far surpassing the 5–6 months seen with chemotherapy.

Well-tolerated and first-in-class, ateganosine positions MAIA for leadership and first-mover advantage in the multi-Bn-dollar NSCLC market.

#7. MAIA Has Multiple, Potential Value-Driving Milestones In The Near Future. |