To support our work please consider becoming a paid subscriber to EconVue+ Part 1: RecapIn The Heart of the Matter I advocate for forgiveness of financial and political debt. This includes loan forgiveness programs for poor countries, eliminating the US debt ceiling, and political pardons for the two warring factions of the American political establishment. Resolving these issues and others are prerequisites for greater economic stability and political harmony in the aftermath of the pandemic. Most of my readers heartily agreed, even though no one under the age of 40 got my Don Henley reference. Some had trouble with the idea of political pardons, but most agreed that they are fatigued by the incessant media coverage of US political scandals. There is a strong desire for more practical economic and political solutions to our current problems, but no clear channel for them to be discussed dispassionately, and no incentives for leaders to resolve them. Unfortunately, there are additional risks to the post-pandemic recovery such as new global taxation legislation, policy uncertainty and lack of consumer confidence in China, and in the US, student debt payments, an increase in credit card debt and auto loan defaults. All point to a need for wise policy choices that could include some degree of forgiveness or compromise. We need to take immediate action to alleviate visible risks, because there are undoubtedly other hidden risks. Part 2: Post Pandemic Economic Challenges and Hidden RisksPolitical security, the foundation of economic growth, is waning in many places including the streets of my own city, Chicago. Covid has upended the old balances by increasing debt, and costs to service that debt to flood levels, adding to economic uncertainty worldwide. Global trade and finance are tightly interconnected, so the domestic policies of individual countries, especially the US and China, affect others. Still, many nations continue to act as if alone, or even at cross purposes. International organizations such as the United Nations, the WTO, and the World Bank/IMF are caught in the crossfire. New alliances are forming to meet the need for security and economic cooperation. Trade wars and sanctions rarely achieve their goals and often misfire, but despite their proven inefficacy these blunt weapons are being used with greater frequency. Instead of negotiating geopolitical conflicts, we threaten our foes with prosecution prior to peace treaties, as we arm ourselves and others to the teeth. We expect rewards for ourselves, and punishments for others. We apply a pre-Covid mindset to post-Covid problems. Meanwhile, danger lurks beneath the surface of financial and trade networks. In ways that are not clearly understood, shadow banking has become entwined with high levels of government and private debt, creating new channels for liquidity failure. We are not sure where the weakest links are, because private debt is not transparent and central banks don’t always tell the truth. Financial innovation including fintech is another known unknown. Some headwinds to consider:

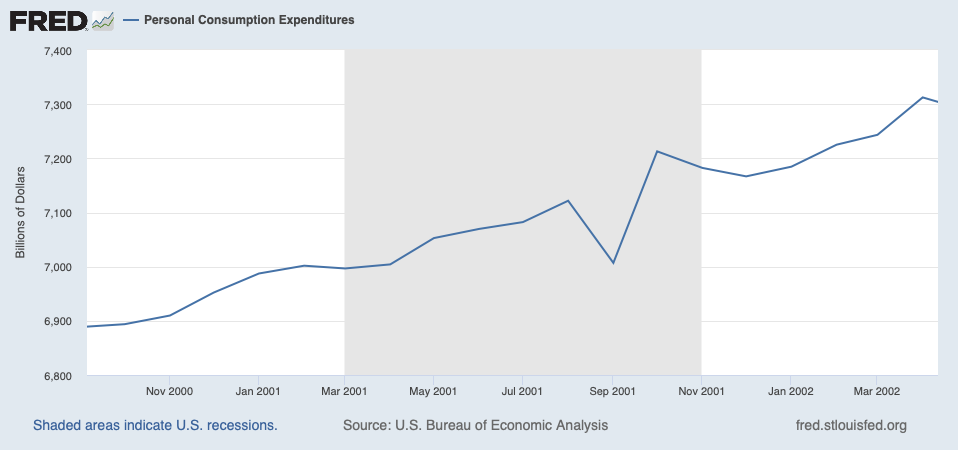

Consumption and Personal Debt in the US and ChinaThere were at least two possible individual reactions to the shock of the pandemic. To save, as Chinese consumers have done historically. The other is to spend and borrow as US consumers who post-stimulus payments are now are maxing out their credit cards. This incidentally also happened in the anxious aftermath of 9/11:

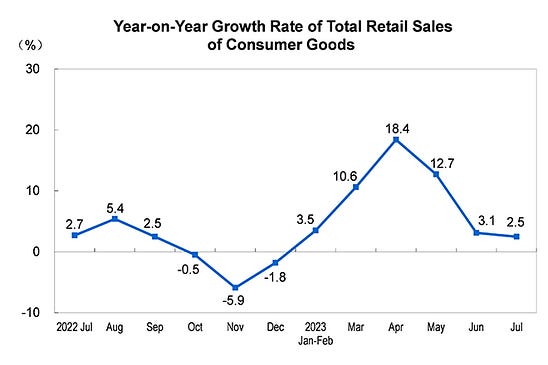

However, US consumption could fall in coming months. Total household debt is increasing, including credit card debt of $1T and student debt of about $1.5T. Student debt payments will resume in the US in October, as gas prices continue to climb. Interest rates are higher, but real estate costs are not falling due to supply constraints, so housing remains expensive. Increasingly, home insurance required by lenders is harder and more expensive to obtain, especially in states such as California which have been highly impacted by natural disasters. Credit card and auto loans defaults are seeing an uptick. This will make new credit harder to get, further depressing consumption. Now that US consumers have used up their pandemic savings, we should be thinking of how to deal with these issues before they become a crisis. I have some recommendations below. Chinese consumers did not increase spending as expected post-lockdown, although forecasts are that during the upcoming Golden Week holidays beginning September 27th we will see a boost in domestic travel, possibly due to pent-up demand that is still playing out.

Balancing this data out, services that are not optional such as healthcare have become more expensive, incentivizing savings. State statistics are harder to find today, but anecdotally, Chinese malls are uncrowded and durable good purchases are down. The transition to a dual circulation economy, driven by both exports and domestic consumption has failed so far. As Martin Wolf writes: The most intractable economic problem is over-reliance on credit-fuelled investment, not consumption, as a source of demand and the parallel over-reliance on capital accumulation, not innovation, as a source of rising supply. What is underestimated is the extent of institutional reform required to achieve a transformation to a consumption-led Chinese economy. Without it, I agree with Michael Pettis that China is unlikely to achieve long term growth that is higher than 2-3%, making it ever harder to find the fiscal room for institutional-level adjustment. In addition to structural constraints, the negative wealth effect in China, which has seen both stock and real estate prices take the down escalator, should be a warning to US policymakers:

China has decided not to offer individuals stimulus relief in order to boost consumption. Now that the US has done so, there is a non-trivial risk that the government might need to do it again, in certain instances. Recommendations to Increase Global Stability and ProsperityWhat this data says to me is that Covid is not “over” and that both pervasive and subtle global economic effects will persist, especially as interest rates rise or plateau. Inflation, and the pendulum shift in the relationship between labor and management in the US, are but two examples of this long-tailed persistence. What could speed up normalization and growth?

The Heart of the MatterThis all might sound a bit dismal, but my concern is that because of the human need to return to normality, we are underestimating longer-term impacts of the Covid-19 pandemic. Further substantial adjustments could still be necessary. On the positive side, the resilience of the world economy in the face of this unprecedented exogenous shock was actually quite remarkable. I have faith that innovation and technology will solve our biggest problems longer term, if we don’t throw down unintentional policy roadblocks along the way. Global commerce is interlinked, but politics remains local. National leaders should be more aware of the extraterritorial consequences of their domestic policies, and be willing to mark to market their post-pandemic losses to boost consumption. Weapons of finance and war should only be used as a last resort. However political courage —the ability to compromise and forgive and begin again— is in very short supply. And that truly is the heart of the matter. You're currently a free subscriber to econVue + . For the full experience, upgrade your subscription.

|