Dear Reader,

According to a former Wall Street insider who's been tracking Trump's every move...

President Trump is preparing to unleash a stunning triple-shock bombshell on Washington.

Creating a frenzy all across America the moment it goes live.

In fact, Trump’s triple-bombshell will be so seismic, it’ll trigger a $7.5 trillion chain reaction in the markets.

With one corner of stocks erupting by up to 1,000% in 12-24 months.

This isn't being covered on CNBC… and Fox Business isn't talking about it.

But the smart money on Wall Street is already moving fast:

- Stanley Druckenmiller just dropped $81 million…

- David Tepper: $270 million…

- Peter Thiel: $273 million…

- Ken Griffin: $1.7 billion…

- Warren Buffett: $5.4 billion….

That's because Trump’s bombshell plan is his priority #1.

He’s fired up about this.

Based on undeniable evidence you’ll see today for the first time, Trump’s plan could go down in history as one of the greatest ‘America first’ initiatives of our lifetime.

It’ll be bigger than the Apollo program and even bigger than the Manhattan Project.

And Trump wants to see initial results within 90 days.

By then the biggest gains will have long since vanished into thin air.

So get the full story here on Trump’s triple-shock bombshell before it's too late.

To Your Profits,

Adam O'Dell

Chief Investment Strategist, Money & Markets

P.S.This opportunity could deliver 10X gains in a year.

Good enough to turn $100,000 into $1 million.

The kind of gains that made NVIDIA’s early investors rich beyond their wildest dreams.

Wall Street Loves FIGS. So Why Do Price Targets Predict a Pullback?

Authored by Jennifer Woods. Originally Published: 3/2/2026.

After a stunning plunge following its 2021 IPO, medical and lifestyle apparel company FIGS, Inc. (NYSE: FIGS) has climbed back to a price it hadn't seen in nearly four years. The stock has surged almost 260% over the past year, including a 58% gain in the last month alone. The rally has been driven by strong earnings reports and a wave of bullish analyst commentary. Yet despite the rally and positive sentiment, the consensus 12-month price target sits at just $12.25 — almost 30% below the current stock price. That raises the question: how much of this recovery is supported by fundamentals, and how much is momentum? A closer look at FIGS’ recent results and the stock's price action offers some clues.

Early investors saw a quick windfall after the company's May 2021 IPO, which priced at $22 per share and surged to $50 within a month. Demand for medical apparel was high during the COVID-19 pandemic, but as the pandemic eased, shares reversed sharply and, within a year, were trading below $8. In the years that followed, FIGS remained mostly range-bound in the single digits. After dipping below $4 in April 2025, the stock began another upward move — this time more sustained.

Earnings Momentum Sparks Rally

After steady gains following positive Q1 and Q2 2025 earnings reports, the Q3 2025 results, released on Nov. 6, pushed the stock higher. The report showed stronger-than-expected revenue growth, solid demand across FIGS’ core business, and healthy margins despite tariff pressures. The company also issued an upbeat outlook, raising full-year guidance for net revenue and adjusted EBITDA margins. Wall Street rewarded the news, lifting the stock more than 30% over the following week and prompting Zacks Research to upgrade the stock to Strong Buy from Hold.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Key Points

- FIGS stock is up nearly 260% over the last year

- Strong earnings have fueled the rally

- Stock is trading almost 30% above the average price target

- Special Report: [Sponsorship-Ad-6-Format3]

Momentum continued with the Q4 2025 earnings report released on Feb. 26. Q4 revenue jumped 33% and marked the company's best quarterly result, with sales exceeding $200 million. In its earnings call, FIGS highlighted strength across the business, including growth in its active customer base and higher average order values. Scrubwear — more than three-quarters of net revenue — was a particular bright spot, rising 35%, and international sales climbed 55%. The fourth quarter capped a strong year: full-year net revenue rose 14% year-over-year to a record $630 million. Despite tariff-related pressure on gross margins, profitability was robust, with full-year adjusted EBITDA margin beating its target by more than 200 basis points.

Earnings And Outlook Spark Analyst Support

FIGS also issued an upbeat outlook for the year ahead, citing continued demand driven in part by growth in healthcare jobs. The company plans to expand into new international markets, prioritize growth opportunities across its businesses, and continue its stock buyback program. For fiscal 2026, FIGS expects net revenue to grow 10% to 12%, with improvements in profitability.

Analysts responded with a wave of positive research notes after the earnings release. Barclays raised its rating to Strong Buy from Hold, KeyCorp moved to Overweight from Sector Weight with a $17 price target, and Goldman Sachs shifted to Hold from Strong Sell. BTIG reiterated a Buy rating with a $15 target, and Telsey Advisory increased its target to $15 from $9.

FIGS Stock Pushes Past Price Targets

FIGS’ strong results have been the primary engine behind the stock's run to four-year highs. Shares began climbing even before the Q4 report, jumping nearly 14% in the session ahead of the release. After the results, the rally accelerated: the stock surged 24% on the first trading day following the report and added another 10% the next day. As of March 4, the stock was trading above $17, about 30% above the $12.25 average 12-month price target based on 10 analyst reports. It is more than double Morgan Stanley's $8 target issued in January and sits at or above most other targets, including KeyCorp's $17.

The gap between bullish analyst sentiment and relatively modest price targets suggests analysts like FIGS’ improving fundamentals but remain cautious on valuation. At its current level, shares trade at a price-to-earnings ratio near 90, implying much of FIGS’ expected growth may already be baked into the price. Investors are clearly applauding the turnaround, but skepticism persists about whether the stock can sustain further gains or if a pullback may be likely.

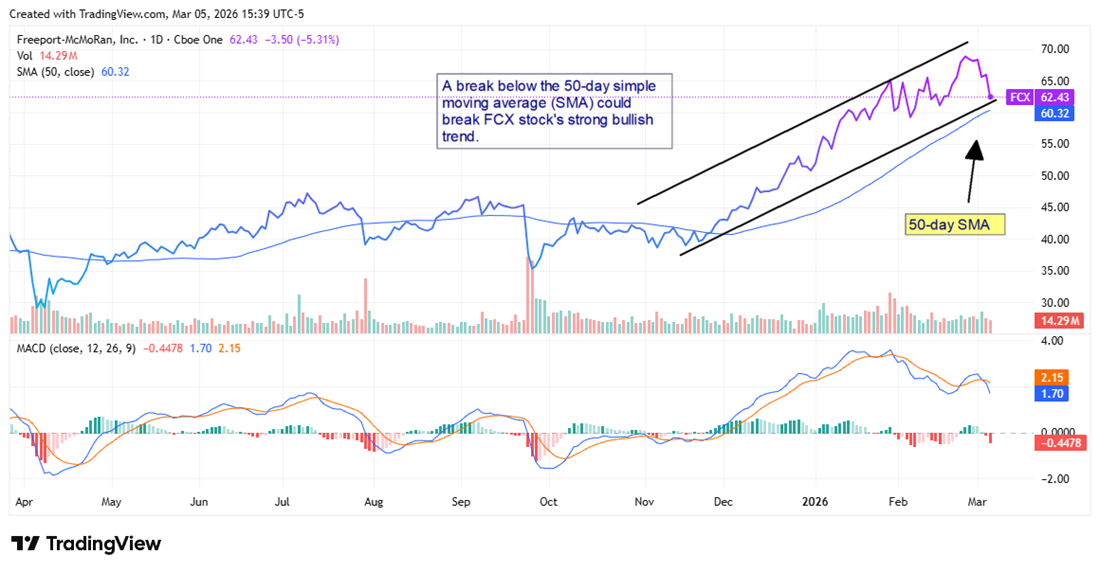

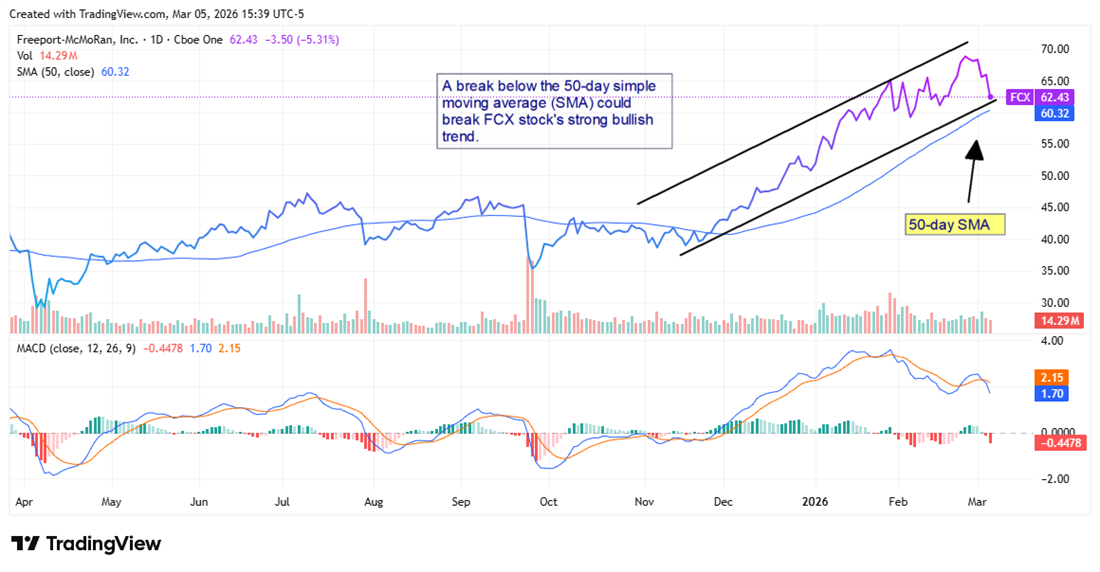

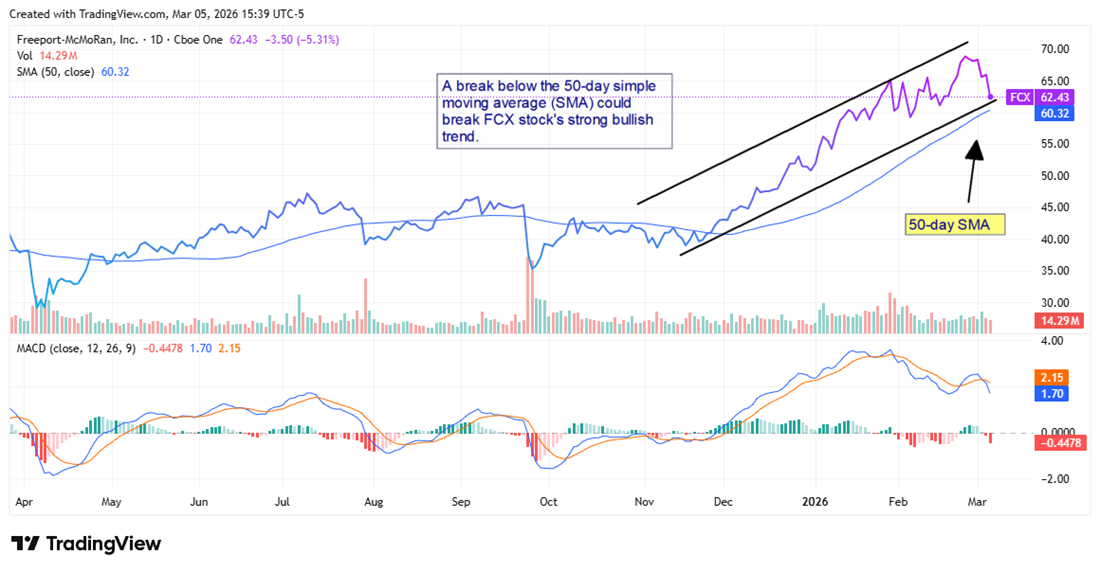

Freeport-McMoRan: Grasberg Deal Frames Long-Term Risk and Reward

Authored by Chris Markoch. Originally Published: 3/5/2026.

Freeport-McMoRan Inc. (NYSE: FCX) came into 2026 riding a wave of bullish sentiment. The company is one of the world's leading copper miners at a time when basic materials stocks, in general, and mining stocks, in particular, are considered among the safest investments.

However, after surging nearly 20% following its earnings report on Jan. 22, FCX has given back nearly all of those gains. Its $62.37 close on March 5 sits near the 50-day moving average of $60.32. To investors who missed the rally that began in November 2025, the recent pullback may seem puzzling.

Dig a little deeper and a more nuanced picture emerges: the long-term bull case remains largely intact, arguing for a buy-the-dip opportunity. However, near-term valuation concerns and geopolitical complexity could push the stock lower before it resumes an uptrend.

The Grasberg Factor: A Calculated Bet on Indonesia

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

The Grasberg mine in Papua, Indonesia, is one of the world's largest copper mines and one of its largest gold mines. It's also central to the bull case for Freeport-McMoRan.

On Feb. 18, Freeport announced that it had restructured its relationship with the Indonesian government. Specifically, the company traded a majority stake in the Grasberg operation to state-owned PT Indonesia Asahan Aluminium (Inalum) in exchange for operational continuity and a long-term contract of work.

The arrangement locks in Freeport's right to operate through at least 2041, giving the company a runway that matters when you consider where copper demand is headed.

This was pragmatic dealmaking under pressure, and shareholders pushed FCX to its all-time high within a week of the announcement.

As the stock has retreated, investors may be weighing the trade-off: Freeport now holds a minority economic interest in the mine versus its previous majority position, which reduces per-share earnings leverage to Grasberg's output.

Still, Grasberg's ore body and rich gold and copper grades mean even a minority stake produces meaningful cash flow. This isn't a diminishing asset, and that cash flow should become more valuable as electrification increases demand for copper.

The Copper Demand Thesis Is Not Going Away

The long-term bull case for FCX ultimately rests on copper, and that story remains strong. In 2022, investors focused on electric vehicles (EVs) and renewable energy infrastructure. By 2026, that narrative has expanded to include grid-scale battery storage and data centers.

Demand for copper is surging while supply is not keeping pace. There are three key reasons for that.

- New large copper deposits are increasingly rare

- Many are located in geopolitically difficult regions

- The ones that are accessible require years and billions of dollars to bring online

Freeport, with world-class assets in Arizona, Peru, and Indonesia, is one of a small number of companies capable of meeting that demand at scale.

Analysts tracking the copper market broadly agree that the structural deficit expected in the late 2020s has not been priced away. Macroeconomic concerns—slower Chinese growth and the impact of higher interest rates on industrial demand—have muddied the picture, but the electrification tailwind remains generational.

Gold Adds a Second Engine

Adding to the bull case for FCX is the company's exposure to gold. Grasberg is not a copper mine that produces a little gold on the side; it is a genuine dual-commodity powerhouse.

Historically that may not have mattered as much, but it does today. Gold is in a multi-year bull cycle, driven by central bank accumulation, de-dollarization trends, geopolitical uncertainty, and investor demand for hard assets. With gold trading well above $2,000 per ounce in recent months, Grasberg's gold revenue is increasingly material to Freeport's overall earnings profile.

This gold exposure acts as a partial hedge against copper price volatility and provides FCX with a revenue stream operating in a favorable pricing environment, largely independent of industrial demand. For long-term investors, that dual-commodity structure is a genuine differentiator among the major mining stocks.

The Chart Is Sending a Warning Signal

The technical picture warns against aggressive short-term positioning. FCX rallied from roughly $38 in October 2025 to a peak just above $70 in early February 2026. A move of more than 80% in roughly four months almost always requires consolidation.

The MACD has turned negative, with the signal line sitting above the MACD line — a bearish crossover. That, combined with the stock breaking below its recent trading range, suggests the path of least resistance in the near term may be lower — or at best sideways — before the next leg higher.

The 50-day moving average at $60.32 represents the first meaningful support level. A sustained break below that would open the door to a test of the $55 area, which served as a prior consolidation zone on the way up.

Key Points

- Freeport-McMoRan’s Grasberg restructuring secures operations through 2041 but reduces its economic ownership, creating both stability and lower earnings leverage.

- Rising copper demand from EVs, data centers, and electrification supports the long-term bull case for FCX stock.

- After an 80% rally in four months, technical indicators suggest FCX stock may pull back toward the $55–$57 range before its next move higher.

- Special Report: [Sponsorship-Ad-6-Format3]

This message is a paid sponsorship provided by Banyan Hill Publishing, a third-party advertiser of The Early Bird and MarketBeat.

If you would like to unsubscribe from receiving offers for Strategic Fortunes, please click here.

If you have questions or concerns about your newsletter, please feel free to email our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place #620, Sioux Falls, SD 57103-7078. USA..