Hi, Tim Plaehn here.

Silver has become one of the best investments for both growth AND income.

I've just found one tiny fund that is now delivering up to 20% in annualized cash distributions….

And could deliver $1,170 every month for you.

However that's not all….

The share price has jumped 68% in just 5 months.

This is one of the rarest combinations I've seen in 20 years of analyzing investments.

Click here to see how this works.

But hurry: the next monthly payout hits soon.

To your income,

Tim Plaehn

Lead Income Strategist

P.S. This isn't physical silver. It's a simple ETF that trades like any stock. Buy once, collect monthly income.

Why eBay's Depop Acquisition Matters More Than the Earnings Beat

By Chris Markoch. Publication Date: 2/20/2026.

Key Points

- eBay’s Q4 beat and GMV acceleration support a comeback narrative, even as the stock remains pressured by broader “AI trade” sentiment.

- Advertising and recommerce are emerging as durable growth engines, while Depop adds a targeted Gen Z/Millennial wedge.

- Depop integration costs, cyclical category tailwinds, and margin pressure remain the main risks to watch.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of eBay Inc. (NASDAQ: EBAY) were about 3.8% higher the day after the company delivered a strong Q4 2025 earnings report. On one level, the results make sense: eBay is a pure play on consumer spending, which has remained resilient despite conflicting macroeconomic signals. Plus, eBay fits into the "discount" category of retail stocks that has performed solidly in a volatile market.

There was a lot for investors to like. Revenue of $2.97 billion exceeded expectations of $2.87 billion. A key metric, gross merchandise volume (GMV), climbed to $21.2 billion — up almost 6% globally and nearly 10% in the United States. That suggests the platform is expanding and attracting more customers.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Another highlight was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. (NASDAQ: ETSY), for $1.2 billion in cash. The move is a strategic attempt to capture more of the Gen Z and Millennial customer base.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY stock was trading lower in early 2026 ahead of the report. One solid quarter won't change sentiment overnight, but there are several reasons to believe in eBay's comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 report showed three specific engines doing the heavy lifting. The first is advertising. On an annualized basis, eBay is approaching $2 billion in ad revenue — a stream that was almost non-existent five years ago.

Total advertising revenue was $544 million in Q4, representing GMV penetration of nearly 2.6%, with first-party ads growing over 17% to $517 million. About 4.8 million sellers adopted at least one promoted listing product during the quarter. The takeaway is that advertising is becoming standard behavior on the platform, not just an optional feature for power sellers.

The second growth engine is recommerce (pre-owned and refurbished merchandise). This category accounted for over 40% of the company's GMV in 2025 and grew roughly 10% during the year. Recommerce is an area where eBay is distinct from Amazon.com Inc. (NASDAQ: AMZN), and one that Amazon will be hard-pressed to replicate at scale.

The third growth engine is the Depop acquisition. In 2025, Depop generated approximately $1 billion in gross merchandise sales for Etsy. Nearly 90% of Depop's roughly 7 million active buyers are under age 34 — a demographic eBay has historically struggled to attract.

Depop specializes in private-label and curated fashion, one of the fastest-growing segments in retail. If these younger shoppers migrate to eBay with the platform integration, it could provide a credible foothold that drives revenue growth.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

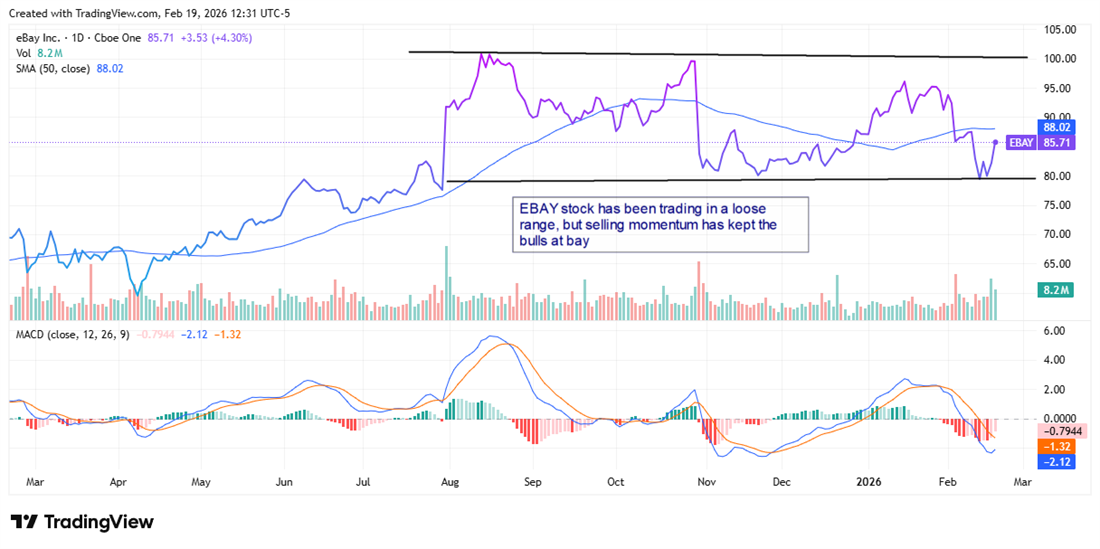

Institutional sentiment around EBAY has been bearish over the last three quarters, with selling outpacing buying by about $2 billion. Some of that selling may reflect the stock's run: EBAY hit an all-time high in August 2025 and then traded in a loosely defined range with support around $80 and resistance near $100.

Still, the eBay analyst forecasts on MarketBeat show analysts have been quick to raise price targets on EBAY stock. Several new targets sit above the consensus price of $96.52 — roughly a 12% premium to the stock price at the time of writing. The most bullish comes from Needham & Company, which raised its target to $122 from $115.

Investors should also consider the company's dividend. A dividend alone isn't the reason to buy a stock like EBAY; investors should want to see the company investing in growth, as it is with the Depop deal.

That said, the dividend yield of 1.35% is above the S&P 500 average. The company has increased the dividend at an average rate of over 14% in the last three years, to a current annual payout of $1.16. The payout ratio, just over 25%, is modest and not draining the company's cash.

Risks That Investors Shouldn't Ignore

While the bull case is compelling, there are several risks to keep in mind. First, some of Q4's GMV growth was commodity-driven. Management acknowledged on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025. Those categories are cyclical and unlikely to repeat at the same rate.

Second, the Depop deal, though strategically sensible, carries near-term costs. eBay expects the acquisition to represent a low single-digit headwind to non-GAAP operating income growth and dilution to EPS growth, with accretion not expected until 2028.

Third, non-GAAP gross margin slipped by nearly 80 basis points year over year. Sustainable margin expansion in the face of Amazon's logistics muscle and Shopify's (NASDAQ: SHOP) seller ecosystem remains the central question keeping EBAY under pressure. The margin decline was primarily due to the scaling of managed shipping and Authenticity Guarantee programs — necessary investments that underscore the real costs of protecting trust on a peer-to-peer marketplace.

In short, eBay's Q4 report and the Depop acquisition give the company multiple growth levers — advertising, recommerce, and a pathway to younger fashion shoppers. Those positives are real, but investors should weigh them against near-term dilution, margin pressure and cyclical category tailwinds when assessing EBAY's outlook.

From Missteps to Momentum: Jack in the Box's Comeback Plan

By Thomas Hughes. Publication Date: 2/21/2026.

Key Points

- Jack in the Box is working through execution and balance-sheet challenges, while McDonald’s highlights what strong operational discipline can deliver.

- Despite weak first-quarter results, analyst targets and ratings suggest continued confidence in a recovery over time.

- Technical support, heavy institutional ownership, and elevated short interest could amplify any upside catalyst.

- Special Report: [Sponsorship-Ad-6-Format3]

Comparing Jack in the Box (NASDAQ: JACK) with McDonald’s (NYSE: MCD) may sound like comparing apples and oranges, but there is a connection. Where McDonald’s executes at a high level, leans into digital, and gains market share, Jack in the Box has endured a series of executive missteps that culminated in lost market share, reduced shareholder value, rising debt, and suspended capital returns.

The connection? Jack in the Box's problems can be corrected. It won’t unseat McDonald’s as the world’s largest restaurant chain, but it can take cues from its more successful competitor, reclaim lost ground, and reinvigorate shareholder value. Last year’s CEO change is the first of several steps that could lift this consumer stock back to higher levels over time.

Analysts Remain Optimistic for a JACK Turnaround

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Despite weak fiscal Q1 2026 results, the analyst response shows confidence in the turnaround efforts. (Note that Jack in the Box's fiscal reporting period does not align with the calendar year.) Sales fell more than expected, in part because of store closures intended to rationalize and optimize the franchise footprint; nevertheless, analysts remain hopeful. The first revision tracked by MarketBeat reaffirmed a Hold-equivalent rating while raising the price target to $23.

The $23 target sits below the consensus $26 but still suggests potential for a double-digit advance when recovery materializes. As it stands, 21 analysts rate the stock a Hold, with a 67% conviction rate, and project levels more than 40% above the company’s critical support level.

The critical support level in February 2026 corresponds to the long-term low set during the height of the COVID-19 panic. That low may represent a market bottom and a likely turning point.

Price action in 2025 suggests a bottom may be forming, with potential to evolve into a reversal if upcoming releases show improvements in operations and quality. The post-release move included a roughly 15% decline in the stock price—alarming in magnitude but not yet a definitive red flag. The decline and subsequent action broadly align with a possible head-and-shoulders bottom formation.

In this scenario, price could dip in the near term before lows are reached and a recovery begins. If the stock falls below the support target and confirms a move lower, the decline could deepen, potentially revisiting levels not seen in more than two decades or even sliding into single-digit territory. However, technical indicators and institutional activity point to the $16.80 floor as a meaningful level of support.

Institutions Set Floor: Short-Sellers Provide Potential for Rapid Share Price Increase

Institutional activity indicates confidence in the brand and its cash-generating ability. Although selling rose in Q4 2025 and Q1 2026, buying increased as well and outpaced selling. The net result has been accumulation and a solid support base, with institutions accounting for nearly all public shares. The next question is what happens next—one possible answer is a short squeeze, or at least a short-covering rally.

Near-term headwinds remain, but store rationalization, quality improvements, and debt reduction position the company for a healthier recovery, including a return to growth and resumed capital returns. With short interest above 26% and roughly 13 days to cover, a squeeze could be a potent catalyst. If a squeeze takes hold, reaching the consensus $26 target could be an interim stop; technical targets combined with high short interest suggest the stock could move into the $30–$40 range, and potentially higher.

Jack in the Box Amid Transformation: Catalysts Ahead

Key catalysts include debt repayments, which will free up cash flow; asset sales, which will lighten the balance sheet; portfolio rationalization to optimize the footprint; and clearer capital allocation. Capital returns were suspended to pay down debt, but the paydown appears on track, supporting the prospect of resumed dividends and/or share repurchases sometime in 2027.

Assuming a payment of even half the last recorded dividend, the yield would be greater than 1%. End-of-Q1 highlights show the share count was marginally higher while cash increased by roughly 57%, providing room for accelerated debt reduction.

This email message is a paid advertisement sent on behalf of Investors Alley, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you need help with your subscription, please contact our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC.

345 North Reid Place, Sixth Floor, Sioux Falls, S.D. 57103-7078. U.S.A..