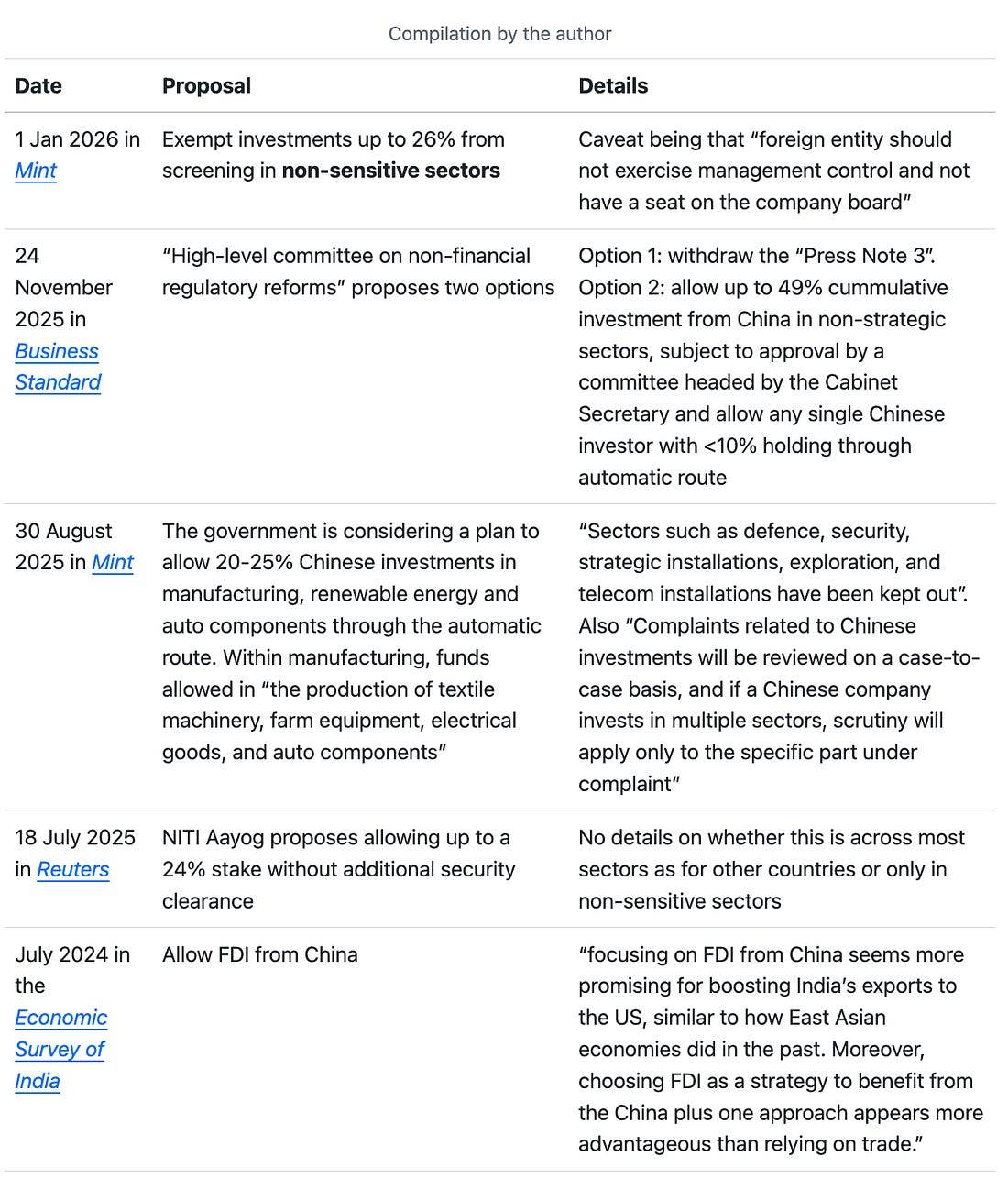

#337 Ramps, Tipping Points, and U-turnsThe West Asia War, a welcome TACO on chip controls, India's Energy Insecurity, and the Press Note 3 AmendmentGlobal Policy Watch #1: Off-ramps AvailableGlobal issues and their impact on India—RSJThe great pleasure of following geopolitical events is how much sense everything makes in retrospect, even though very little can be accurately predicted in advance. In that sense, its practitioners can sometimes be on a par with astrologers. They remind everyone of the odd prediction, which was loaded with assumptions, they got right while conveniently forgetting others. There is no shortage of experts who are now talking about the inevitability of the asymmetric warfare that Iran is waging with its blockade of the Strait of Hormuz, the civilisational state that is Iran and how its state infrastructure can’t just be wished away. Everyone now can see the miscalculation that Trump and Netanyahu made in assuming that knocking out the ayatollah and the top brass of the Islamic state would automatically lead to a people’s revolution and regime change. The fact that none of these was part of the war-gaming scenario is an apparent head-scratcher for everyone now. Hindsight is a lovely thing. Well, therefore, all forecasts now about which way things will shape up in the next two weeks are as reliable as believing in your weekly horoscope. No one really knows anything. We are in a stalemate of the most intractable kind. The Iranian state has survived the worst of aerial bombardment and seems to be as entrenched as ever, with a new head of state who will be as strident as his father. It has now held the global oil supply and logistics to ransom for a week by shutting down the Strait of Hormuz. It has enough missiles and drones left, and with some Russian navigation and targeting support, it is keeping everyone in the Gulf region on tenterhooks. And I guess it still has some 400 kgs or more of 60 per cent enriched Uranium that can’t be taken away from it unless there’s a ground force that physically takes possession of it, which looks unlikely now. In the meantime, polycrisis is upon us: oil is over $100 per barrel, global LNG supply from Qatar has broken down, there is a real possibility of a global oil crisis in the next few weeks, expats and capital are fleeing the Gulf states and Trump is declaring that he’s won the war and there’s nothing left to strike in Iran. The problem is that it takes one to start a war but two to call a ceasefire. Iran has no incentive to make things easy for the world and to de-escalate its asymmetric approach. It has now waged a war on the global economy. Nobody, except Iranians themselves, apparently cares for Iran being bombed to oblivion, but everyone understands the petrol price hike, cooking gas shortage and inflation. So, why not hurt them there? For Iran, this is the war to end all wars. Either it ceases to exist as a state, or it ensures no one bombs it again without consequences for a long time. All blame can be laid at Trump’s door for having initiated this. The convenient way that Trump thought this war would end after knocking off the ayatollah was for Iranians to engineer a regime change or descend into a civil war. Neither has happened so far. The only other option left is to sit down with Iran, agree on a ceasefire, and return to the deal that Oman and other intermediaries were working out prior to these strikes. But why would Iran agree to that deal now? They don’t want similar strikes to rain down on them in another six months after the deal. What’s the guarantee against that? So, they will ask for Russia and China to be on the table, they will demand lifting of the multiple sanctions that have been crippling them, a guarantee for future security and more. That will mean no deal for quite some time because I can’t see Trump agreeing to these. I suspect we are going to be in this low-intensity war for the foreseeable future. The US will declare victory and withdraw. Israel will stay in a perpetual state of readiness for war. The Gulf states will work out their bilateral peace with Iran at the expense of the U.S., which will then mean Iran will selectively let ships go through the Strait of Hormuz and guarantee no strikes on airports, hotels, tech companies, et al in the region. But who really knows? All this is just the astrologer in me speaking. Often on these pages, we write the metaphorical “we have seen this movie before” when we come across a PolicyWTF that’s been repeated earlier. However, this war is a brand new release. We haven’t seen this movie before. But as I thought about the possible endgame scenarios for this, I realised I had quite literally seen a few of these movies before. So, here are my three scenarios for what could happen next, based on three of my favourite movies from three different eras spanning 45 years. The “No Other Choice” scenario: In this Park Chan-wook adaptation of the Donald Westlake thriller, The Ax, a middle-aged manager of a paper company is laid off as part of a cost-cutting exercise. He then begins to hunt down the people living in his town who could possibly take his job, one after another, so that eventually he remains the last eligible man standing. Every time he eliminates one, things get worse, and he digs himself deeper into a moral quagmire. This is the scenario Trump and Netanyahu are working toward at this moment. They will keep knocking off one ayatollah after another that Iran puts up, pleading they have no other choice, till they find one who will do their bidding. Alas, when they get to that one pliable ayatollah, they will realise that IRGC has developed an AI ayatollah agent using Seedance 2.0 who acts and talks like the deceased Ali Khamenei, and they are now taking orders from him. All the killings and destruction they did led to zilch. Life is meaningless. The Groundhog Day scenario: Bill Murray is a cynical, world-weary TV weatherman who gets trapped in a time loop in the small town of Punxsutawney. His life becomes an endless repeat of the same day (Feb 2 or the Groundhog Day) and no matter how he tries to alter the day’s proceedings, he wakes up the next morning again to “I got you babe” playing on the radio and it is still Groundhog Day. This seems like the default scenario for Trump in this war. He wakes up every morning thinking of obliterating Iran in a new way that will rid him of the evil regime forever. After another day of calling Iran new names (deranged scumbags, for instance) and pounding them with bombs, he sleeps thinking tomorrow will be a new day. Yet, he wakes up to the same day with Iran still blocking the Strait of Hormuz and oil at over $100. This goes on till one day Trump has a change of heart, falls in love with the reigning ayotallah, breaks naan with him and they tango together to the music of kamancheh. The next morning he wakes up to “I got you babe” on the radio but finds it is indeed a new day with Iranian TV playing Trump rallies on the loop. The Hirak Rajar Deshe scenario: In the land of Hirak, there are diamonds and riches galore, but there is a tyrant Raja who represses his subjects and starves them while he entertains himself with dance and music at his palace. Any subject who protests or questions the regime is swiftly deported to the jantarmantar, the brainwashing chamber of the Raja, where such rebellious thoughts are squashed. This goes on till Gopi and Bagha, the magical singing duo, arrive at the kingdom and, together with the sole banished rebel, Udayan Pandit, go about setting things right. The film ends with the singing duo mesmerising the king with their singing and then pushing him into the brainwashing chamber from which he emerges as a just and reformed king who happily pulls down his own statue at the central square. All’s well in Hirak Desh. Fantastic as it may sound, to me, this is the most desirable scenario. If only Trump and Netanyahu could be convinced to disguise themselves as wandering minstrels and enter Tehran, they could easily brainwash the entire regime to mend their ways with their magical singing and dancing skills. We could have world peace and a blockbuster Netflix series for 2027 at the same time. Satyajit Ray FTW. India Policy Watch #1: Definitely Not China, Padhaaro Mhaare DesInsights on current policy issues in India—Pranay KotasthaneIn edition #328, we had a chart listing all the proposals circulating in Indian news outlets regarding a possible recalibration of India’s position on China’s investments. Here’s that chart once again for reference.

So, after all this balloon floating, the government has finally announced a policy change. And turns out, the eventual amendment is far less permissive than any of the solutions that had been floated thus far. Let me explain. Earlier this week, the Union Cabinet amended the FDI rules governing investments from land-bordering countries (LBCs). If you read the headlines, you might think the doors to Chinese capital are swinging open. They aren’t. Here’s how. A Quick RecapIn April 2020, at the height of COVID-19 anxiety, India introduced Press Note 3. The rule was blunt and meant to prevent ‘opportunistic takeovers of distressed Indian firms.’ Any entity from a land-bordering country—read China—could invest in India only through the government approval route. No exceptions. The problem is that blunt instruments such as these created collateral damage. A Singapore PE fund with a Chinese LP holding 8 per cent of the fund got caught in the same net as a Tencent or an Alibaba. Global investors started routing around India. Startups and deep-tech firms began complaining that PN3 was quietly strangling their fundraising efforts. Six years later, the government responded. What the Amendment DoesIt makes two changes. The more substantive one is the amendment, which introduces a Beneficial Ownership (BO) test at the level of the investing entity. If a fund’s Chinese beneficial ownership is below 10 per cent, that fund can now invest through the automatic route. This is not a green light for Chinese investors to directly pick up stakes in Indian companies. A direct Chinese investment still requires government approval, regardless of stake size. What’s changed is that a Temasek or SoftBank-type fund— with incidental, passive Chinese LP exposure below 10 per cent—can now invest in Indian startups without going through the approval maze. This matters because the automatic route covers most sectors. For global funds that were being caught by PN3’s broad sweep, this is genuine relief. But the press release offers no rationale as to why this threshold is 10 per cent. The number is borrowed from PMLA definitions, which themselves were designed for anti-money laundering purposes, not strategic FDI screening. Using an anti-money laundering threshold to calibrate national security risk is a category error. Also, how would anyone actually verify the beneficial ownership chain through multiple fund structures, SPVs, and offshore vehicles? The amendment requires the investee entity, the Indian startup, to report relevant details. But the investee often doesn’t have full visibility into who ultimately owns the fund investing in it. The second change is a 60-day processing timeline for Chinese investments in specific manufacturing sectors: capital goods, electronic capital goods, electronic components, polysilicon and ingot-wafer. The government wants Chinese firms to come in as minority JV partners and help India build out its electronics and solar supply chains. The government approval route for Chinese investments continues as before, except that decisions on investments in some sectors will be taken in a time-bound manner. The press release is silent on what happens if no decision is made in 60 days. There’s no deemed approval clause, which would mean an automatic green light if the government misses the deadline. Without that, the 60-day target is aspirational at best. If you were an IES officer in the industry ministry processing these files, nothing about your incentive structure has actually changed. The SignalStep back from the details, and the message is clear enough. The government knows it needs Chinese capital. The electronics and solar manufacturing ambitions under PLI simply cannot be realised without accessing Chinese technology, components, and, in some cases, direct Chinese participation in supply chains. But the government is not yet convinced it has the tools to let that capital in without importing the risks that come with it. So it has done what governments do in such situations: make a partial, hedged move. The 10 per cent BO carve-out helps global funds. The 60-day window helps some manufacturers. Neither touches the core question of whether and when India will have a systematic framework for distinguishing between Chinese capital that poses a genuine strategic risk and Chinese capital that is just capital. Until that framework exists, expect more cautious incremental moves of exactly this kind. Here’s another thing worth keeping in perspective. Even as India agonises over whether to let a Singapore fund with 8 per cent Chinese LP money invest in a Bengaluru startup, the West has spent the last two decades doing something far more consequential with China. American and European firms built deep manufacturing dependencies, took on Chinese JV partners, and allowed Chinese capital to flow into their most sensitive technology sectors. The decoupling conversation in the US and EU today is precisely because the integration ran so deep. India never did any of that because of structural reasons. The India-China economic relationship has always been lopsided and transactional. Bilateral trade is large but shallow. Investment flows, in either direction, have been negligible compared to what China has built with the US, Germany, or South Korea. This amendment doesn’t change that any of this. Global Policy Watch #2: TACO FTWGlobal issues and their impact on India—Pranay KotasthaneFor once, the Trump administration has timed a TACO to perfection. The US Department of Commerce has withdrawn a planned rule that imposed some mind-boggling restrictions on the export of AI chips. Sample this Reuters report from ten days ago, which speculated on what the draft was proposing:

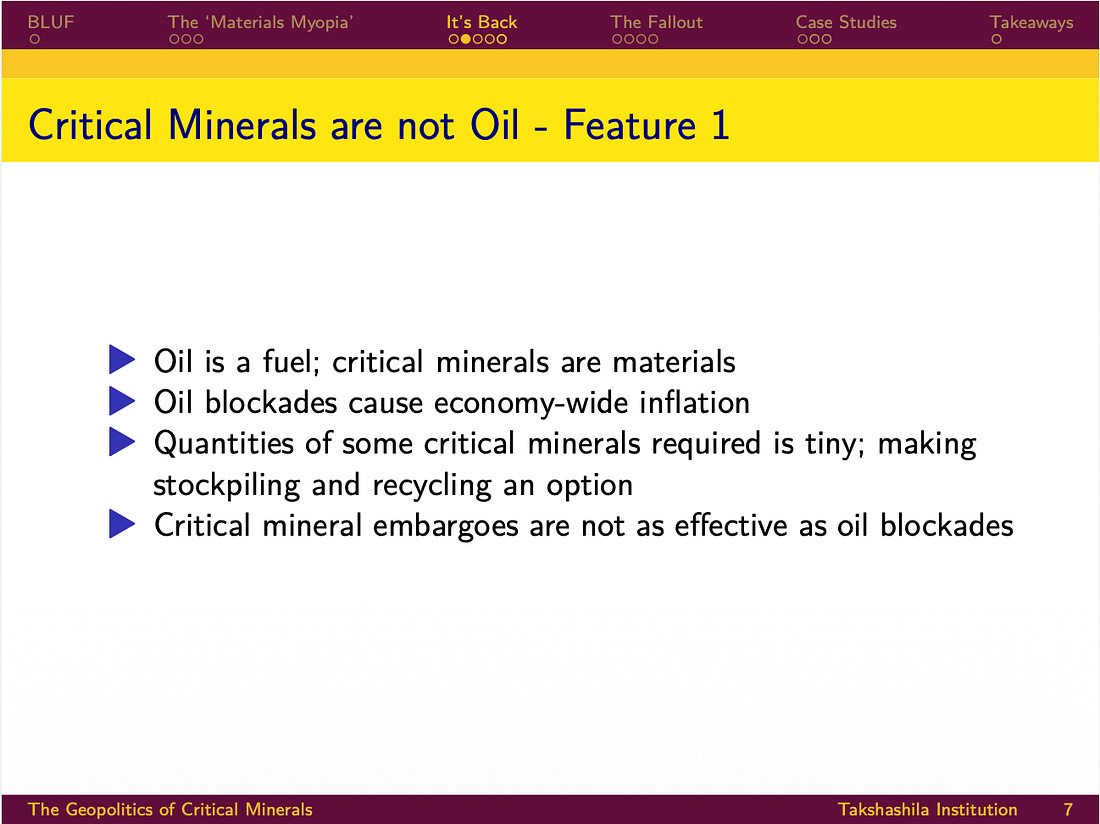

Now, if you have been following this newsletter, you know I find chip export controls ridiculous. I can understand the logic behind controls on semiconductor manufacturing equipment, which are large, specific-purpose, and meant for only a handful of customers. But I do not understand the logic of tightening controls on chips, which are used by thousands of companies and individuals across the world. In any case, these restrictions fail to achieve their primary purpose. Not only have chips been smuggled to China and Russia, but they are also being legally deployed by Chinese companies in other countries, as ByteDance's access to a 36,000 B200 chip cluster in Malaysia illustrates. Given these inherent flaws, policies demanding reciprocal investments from companies and countries in return for buying chips would have been a disaster. Moreover, the prospect of American ‘chip inspectors’ visiting company facilities would have further pushed companies to dissociate themselves from the legal US AI stack. Notably, the Biden administration had proposed the AI Diffusion Rules, which I had then called the AI ‘compute-rationing’ rules. That version had divided the world into three tiers of compute access. There were also rules to prevent the diffusion of models, whatever that meant. After nearly a year of formally rescinding that version, the Trump administration still chose to go back to this tired old strategy of restricting AI chips. Thankfully, it has shelved the draft for now. TACO FTW. India Policy Watch #2: Energy InsecurityInsights on current policy issues in India—Pranay KotasthaneIn my talk on critical mineral geopolitics, I have this slide comparing critical minerals and oil, through which I explain that rare earths are NOT the new oil.

Well, who knew that we would see a crude demonstration of this reality so soon? Within days of the war in West Asia, ATF prices have risen, and panic-buying at petrol pumps has begun. Commercial LPG is also in short supply, resulting in restaurants and textile plants shutting down. The negative impact is immediate and widespread. This situation is a cruel reminder that, despite previous instances of such disruptions in West Asia, India was found woefully underprepared. Things have somewhat improved from where India was during the last Gulf War. There are three conventional energy input streams now—LPG, LNG, and crude oil—each serving different sectors. The uptick in renewable energy has also taken some pressure off gas-based power plants. The strategic petroleum reserves also provide some cushion. Nevertheless, it is clear that this isn’t enough. And the frustrating part is that this inadequacy was well-known. Over a decade ago, in 2014, my colleague Ameya Naik wrote a policy brief proposing six reforms for ONGC Videsh, built around a four-part framework: securing deposits, securing extractors, securing supply routes, and accessing technology. It proposed six reforms: build technological competencies through joint ventures, use swap deals to bring international oil companies (IOCs) to India, invest where India has a comparative advantage, use bidding consortia to avoid price wars with Chinese nationalised oil companies (NOCs), cultivate alliances with private and foreign players, and incorporate political risk comprehensively into overseas investment decisions. Twelve years on, the scorecard is grim. Technology JVs with BP and ExxonMobil materialised, but a decade late. OVL’s biggest overseas bet in Russia became a cautionary tale, with billions in dividends stuck due to the war between Ukraine and Russia. Crude import dependency didn’t improve, and it hit an all-time high of 88.2 per cent in FY2024-25. The political risk recommendation was vindicated in the worst way possible. The LPG problem provides a stark illustration. India’s LPG import share rose from 47 per cent in 2015 to 67 per cent in 2024. Over 90 per cent of those imports come from West Asia, with ~80 per cent transiting the Strait of Hormuz. While the Ujjwala Yojana expanded LPG connections from 15 crore to over 33 crore, the government did not build supply resilience to match this new demand. Nothing much was done on reserves either. India reportedly maintains crude oil reserves covering about 74 days of consumption. For LPG, which is much more costly to store, there are hardly any such strategic reserves to serve as a buffer. The natural gas transition could have eased this, but we didn’t do that well either. Only about 1.4 crore households have piped natural gas connections, compared with 33 crore on LPG. CNG stations for vehicles exceeded targets, but household Piped Natural Gas has failed miserably. PNG requires last-mile pipelines to individual households in cities, an exercise made impossible by our dysfunctional urban governance. Meanwhile, the government was also subsidising the import-dependent fuel at scale, while PNG had no comparable consumer incentive. Nor have we done anything significant on nuclear energy, which could have reduced the demand for gas-based power plants. The underlying pattern is that India has been strong on access infrastructure like Ujjwala connections, CNG stations, refinery capacity, etc. These are visible and politically rewarding. But it has been systematically weak on supply resilience: strategic reserves, domestic production, feedstock diversification, and chokepoint assessment. Oil and gas remain the most strategic commodity. While getting into shiny things like chips and rare earths, we first need to solve the same old energy security equation. HomeWorkReading and listening recommendations on public policy matters

|