Editor's Note: Tech legend Jeff Brown — the same man who picked Tesla before it soared 2,150% — says while everyone thinks Elon's empire is crumbling, there's a $25 trillion revolution brewing that could 10X Tesla's past success. Click here to see what he uncovered or read more below...

Dear Reader,

While everyone obsesses over Tesla's car sales plummeting...

Jensen Huang — CEO of Nvidia and arguably the most powerful man in AI — just made a stunning declaration about Tesla's future.

He said Tesla's work on what I call “Manifested AI” could be part of a "multi-trillion-dollar future industry."

Think about that for a second…

This is the man who built the $4 trillion company that brought forward every major AI breakthrough of the past decade.

He doesn't throw around trillion-dollar predictions lightly.

And yet…

Nvidia’s CEO is telling everyone exactly what I’ve been saying for years now.

While most people think Tesla is just another electric car company…

The truth is: Tesla is the most valuable AI company in the world.

And right now…

Tesla is about to prove it by shocking the world with their BIGGEST AI breakthrough yet…

One that will allow AI to “escape” out of your computer screen…

Manifest itself here in the real physical world…

All while sparking a 25,000% growth market virtually overnight.

The best part of all?

I discovered how you can get in on this brand new 25,000% growth market, with a little-known stock that is 168 times SMALLER than Nvidia itself.

Click here now for my full report.

Regards,

Jeff Brown

Founder & CEO, Brownstone Research

United Parcel Service Transitions to Growth: Accumulation Begins

Authored by Thomas Hughes. Article Posted: 1/28/2026.

Article Highlights

- United Parcel Service has returned to growth sooner than expected, and its stock price looks to be in rebound mode.

- An ample capital return is reliable in 2026, with distributions expected to increase.

- Analysts and institutional data align with a market bottom and reversal, and trends will likely strengthen as 2026 progresses.

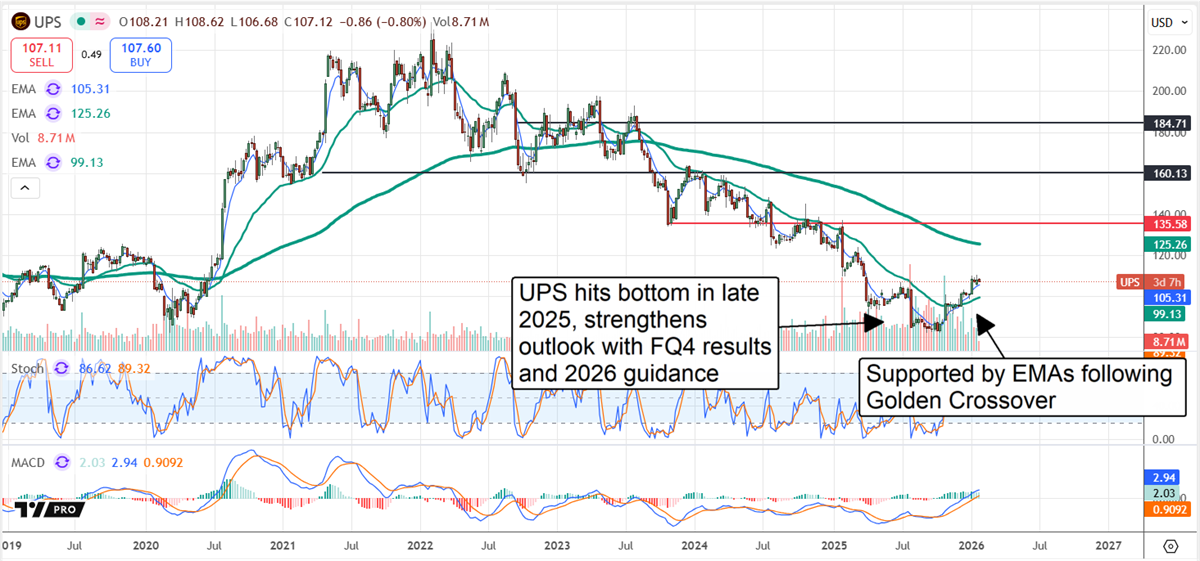

The long-awaited bottom in United Parcel Service (NYSE: UPS) appears to be in, and a rebound is already underway. Backed by stronger results, improving operational quality, and a growth-oriented outlook, the recovery should be substantial for long-term holders. After a period of distribution and downward price pressure from analysts, UPS is returning to an accumulation phase that is likely to strengthen as the year progresses.

Analysts and Institutions Have Shifted to Bullish

The shift is evident in analyst activity: the group rates the stock a consensus Hold and began raising price targets in late 2025.

The Silver Strategy Hiding Inside IRAs (Ad)

In 2000, I told Barron's that a popular dot-com stock was headed for trouble. It dropped 90%. Now I'm making the opposite call on that same company: buy it now. This stock has become the lifeblood of AI data centers, yet almost no one has caught the story. While the media focuses on AI chip wars, they've missed this company's essential role in building out data centers. Their hardware is so critical that a single building uses enough of it to stretch around the world eight times. If you own Nvidia, you might want to pivot. If you missed Nvidia, this is your second chance at the AI data center buildout happening worldwide.

See the under-the-radar play fueling AI data centersThose bullish revisions carried into the first weeks of 2026 and are likely to accelerate now that the 2026 guidance is public.

The company guided to about $89.7 billion in net revenue — roughly 3 percentage points above MarketBeat's reported consensus — projecting growth a full year earlier than previously expected. Margins are also expected to remain healthy, suggesting a leveraged earnings rebound could be at hand.

Institutional activity is supportive as well: institutions own roughly 60% of the stock and were net buyers in Q4 2025. While some selling coincided with earlier lows, a late-quarter shift back to accumulation continued into January 2026 and looks set to strengthen. The Q4 results and 2026 guidance also underpin a reliable capital-return program for investors.

Dividend Strength and Buybacks Reward Investors

Trading near COVID-19-era lows, UPS yields more than 6% and is expected to maintain dividend increases in coming years. The 2026 guide projects payouts slightly higher than in 2025, implying another low-single-digit raise. Share repurchases reduced the share count by approximately 0.7% in 2025 and are expected to continue trimming it in 2026.

UPS Accelerates Stock Reversal With Strong Results

UPS delivered a solid Q4 despite year-over-year contractions in some metrics.

Revenue declined 3.2% year-over-year but came in better than expected — nearly $500 million ahead — as higher revenue per package and strength in international markets offset soft domestic volume and reduced supply-chain solutions demand.

Adjusted operating margin also contracted as anticipated, but matched forecasts, leaving adjusted earnings above consensus by a similar margin.

For investors, the opportunity is to enter early in the rebound.

The outlook for earnings, the potential for outperformance, and the shift in analyst sentiment all point to a cycle of positive revisions and relative strength.

In that scenario, UPS shares could move toward the high end of early-2026 target ranges — a gain of roughly 40% from the pre-release close — as upgrades and bullish target revisions attract demand.

UPS Advances Following Strong 2026 Guide

UPS stock rose following its 2026 guide, finding support near the 30-day exponential moving average (EMA). The 30-day EMA is trending upward, along with the 150-day EMA, after a Golden Cross formed in December 2025. That technical signal, together with evident accumulation, suggests durable support. If these EMA levels hold, a more substantial price rebound is likely.

Key catalysts in 2026 include persistent growth, outperformance, and margin recovery. UPS's investments in digitization, automation and AI should gain traction and compound as business quality improves. The decline in Amazon-related volume is expected to stabilize as the business mix shifts toward higher-margin consumer and commercial traffic. Industry verticals such as healthcare — where UPS targets specialized, time- and temperature-sensitive transportation solutions — should also bolster revenue and margins.

This email is a paid advertisement for Brownstone Research, a third-party advertiser of MarketBeat. Why did I receive this email message?.

If you have questions about your account, feel free to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place #620, Sioux Falls, SD 57103-7078. United States..