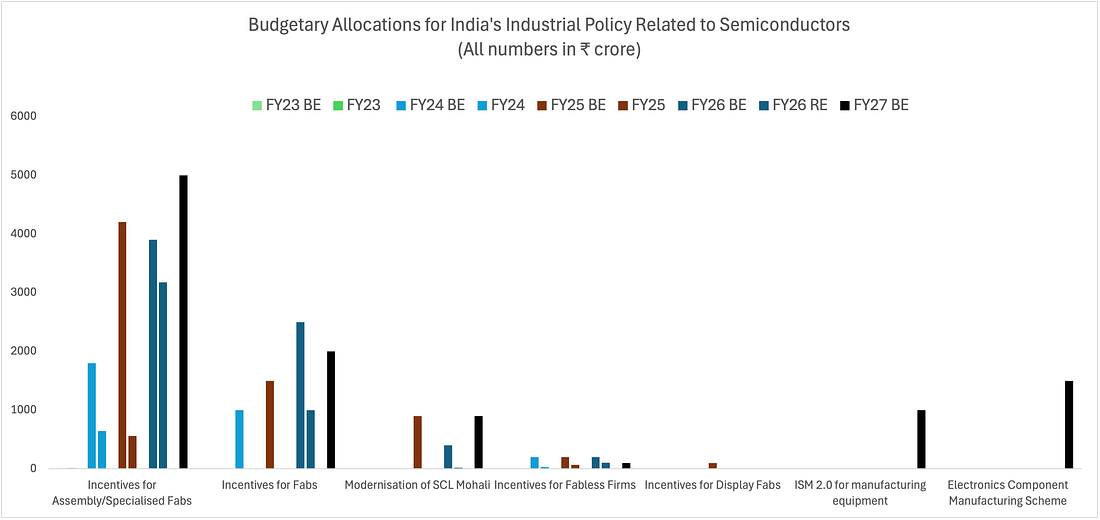

India Policy Watch #1: Remarkably RemarkableInsights on current policy issues in India—RSJA long-revered tradition in India, which has only accelerated in the past decade, is to rate the Union budget 11 on 10 (Spinal Tap copied the idea from us). So, I raised my left eyebrow by an eighth of an inch when I read through the opinion pieces about the record-breaking ninth consecutive budget presented by FM Nirmala Sitharaman. Apparently, the remarkable thing about this budget, according to the talking heads and other worthies, was that it was unremarkable. That’s what India needed, it seems, in this world full of geopolitical tumult. Like modern-day Sherlock Holmes in the Budget version of Silver Blaze, these columnists were explaining to us, the lay readers, the curious incident of the dog in the night-time. The dog did nothing. The unremarkable was therefore the remarkable. Now, I am all in favour of the Union budget becoming an unremarkable event in our economic and political calendar. Policy-making is a round-the-clock, year-round exercise. The annual budget should just be a statement of accounts and a revenue, spending and borrowing plan for the year ahead. Yet, despite gradually going up the maturity curve on policy-making over the years, the annual budget speech is still an important event in signalling or reaffirming the policy intent of the government and announcing big-ticket schemes to support that vision. It retains its salience. There has, of course, been no dearth of schemes in the recent past from the government. In the past few years the budget speech has included among other big announcements, a national manufacturing mission, an employment linked incentive scheme promising 4 crore jobs in 5 years, an internship scheme that would have seen over one crore internships in 5 years across top 500 companies, a variety of start-up India initiatives and multiple urban development schemes (something called urban challenge fund of ₹1 lakh crore was set up for new age cities last year, if I remember right). No one is wiser on what these schemes have achieved because we have since moved on to the next scheme. Given this track record, I’m naturally predisposed to a budget that’s somewhat low on big schemes, to the point and unremarkable. But even with that bias, this year’s budget was so unremarkable that it left me wondering if, in its 13th year of being in power, this government has concluded that letting the economy run its normal course with a few fiscal, monetary and, crucially, statistical tweaks is the best it can do. If that can deliver 7 per cent growth and help us with the crown of the fastest growing major economy in the world, with periodic updates of going past the size of economies of the UK or Japan, that should be good enough for people. Throw in a few aspirational, feel-good taglines (Amrit Kaal is behind us, Viksit Bharat is on now with three kartavyas anchoring it, if you are keeping track), and we are done till it is time for the next budget. Returning to the budget presented last week, there are a few points worth discussing. First, there is no abatement in public capex that’s planned at ₹12.2 lakh crore which is more than double the ₹5.7 lakh crore of capex in FY22 when we were emerging out of COVID-19. There’s a significant allocation set aside for road transport and railways (about 45 per cent) with dedicated freight corridors, new waterways, infrastructure improvement in tier 2 and 3 towns and logistics efficiency as areas of focus. There’s also a sizable jump of over 17 percent in allocation of ₹2.2 lakh crore to the defence sector. The usual argument in favour of public capex is that it eventually “crowds in” private capex as the confidence in the economy builds up, and that such spending creates a strong multiplier effect in the economy, leading to more jobs and wider economic growth. The sustained increase in public capex over the past four years doesn’t seem to have done either. The private capex is still waiting on the sidelines with corporates continuing to deleverage, buyback shares and improve their return on equity rather than go on a greenfield expansion spree. The reasons for lack of confidence are many - from scepticism about real domestic growth opportunities to the fear of China building up significant capacity and a lack of export competitiveness. Also, a significant part of public capex is in sectors where there is clear market concentration (the usual conglomerates) among private players, which has its own dynamics in terms of need to scale up, price discovery and value for the end user. I haven’t seen any study that has gone deeper into the reasons why the multiplier effect hasn’t worked on the back of the public capex spike we have seen in the past 4 years. Second, while the government has stayed on the path of fiscal consolidation (market was expecting a bit more), the gross borrowing requirement of the union government came in at about a trillion more than planned at ₹17.2 lakh crore. Add to this about ₹12 lakh crore of planned gross borrowing by the state governments, we will have a significant supply of government paper to be absorbed next year. The 10-year GSec rate that has stayed high despite a cumulative 125 bps repo cut in the past 12 months will not come down with that kind of oversupply. The 5.7-5.8 per cent range that it has operated within has meant there’s not been a real transmission of the rate cuts. And, this isn’t likely to change given the current dynamics playing out in the economy. This oversupply will continue to crowd out other players looking for credit, which will feed into the problem of private capex waiting on the sidelines. This is also a good time to segue into the other big news of the week - the announcement of the Indo-US trade deal that was done in his customary way by Donald Trump on TruthSocial. If someone had told me around this time last year that by Feb 2026, the US would have hit India with a tariff of 18 per cent, along with restrictions on the purchase of Russian oil and some random US$500 billion committed (?) purchase of American goods, I’d have sat down to steady myself. Yet, it is in a way a tribute to the genius of Trump that most of us are looking at this outcome as some kind of a win after the scenic route he has taken us through in these 12 months. The way media outlets have reported about tariffs being slashed from 50 per cent to 18 per cent would suggest we have been at that high tariff regime for decades. As a reminder, average US tariffs on Indian goods were around 2.5 per cent in March 2025. Maybe the details of the deal that are elusive now (an interim document is out as I write this) will show all the benefits we are getting from this deal. But right now, all I see is India committing like Japan and South Korea to all sorts of purchases and investment in the US, reducing duties to zero on a vast set of US goods, including farm products (as claimed by Trump and US trade representative Jamieson Greer) and getting very little incremental gains in return. Access to the US markets was already available to India with almost zero tariffs for most sectors. Perhaps some incremental opportunity will open in the farm and dairy sectors, but that space in the US is already crowded and reasonably self-sufficient. The thing that worries me the most is whether the upshot of the trade deal is a reduction in the US trade deficit with India, which was around $46 billion in 2024. Because it will hurt the one thing that’s turning out to be the biggest impact player in the Indian economy of late - liquidity. As I have written before on these pages, the slowdown in the economy in most of 2024 was on account of the tight liquidity kept by the central bank in its effort to contain what looked like an asset bubble building up in the unsecured loan segment. It went a bit too far on this tightening, thus squeezing the system out of credit and slowing down GDP growth. The new governor who came in early 2025 committed to keeping liquidity in surplus. That’s what the central bank has done for most of the last 12 months, except they have had a new problem to deal with since Trump took over - capital outflow from India. I have dealt with the structural and cyclical reasons for the outflow in previous editions. The upshot of this has been an unrelenting pressure on the Rupee that has required some stout defending from the RBI in the form of open market operations (thus depleting the forex reserves). If there is a significant rebalance of trade with the US and an increase in the cost of oil imports after delinking from Russia, the capital outflow problem could persist, along with the need to defend the Rupee and the attendant problem of tight liquidity. This could then impact credit offtake as the deal moves into the execution phase. Lastly, the general impression I take away from this budget is the realisation of a party in power which has figured out a way to win elections in India that’s not contingent on strong economic performance. So long as you don’t screw up the economy badly, a combination of emotional issues and timely welfarism (direct cash transfer just before elections is a new, powerful tool now) should see you through most elections. Therefore, a 6.5 per cent growth and a 4 per cent fiscal deficit in a world that’s volatile and unpredictable is good enough to keep the global investors mildly interested while keeping the winning machine going domestically. That may not be enough for us to get out of the middle-income trap or lose out on the narrow window of demographic dividend we had. But the willingness to take bolder bets to address such structural challenges seems to have dissipated. More of the same is what we have settled for. India Policy Watch #2: Budget TakeawaysInsights on current policy issues in India—Pranay KotasthaneAs I have done for the past three years in this newsletter, I analysed the budget data from the lens of two sectors: semiconductors and defence. Here are some key points. SemiconductorsThe latest union budget speech mentions that the government plans to launch a second version of the India Semiconductor Mission. As four years have passed since the launch of India Semiconductor Mission 1.0, now is a good time to assess progress using the government’s own spending data. And to make a fair assessment, we must go beyond speeches and announcements. Thus, I looked up the budget data for all the years since the policy came into effect, and the results suggest a huge gap between promise and delivery.

The chart above shows all budgeted and disbursed amounts to date. Every financial year has two bars of the same colour. The first bar shows the expenditure forecast for the beginning of that year (also called budgeted estimates, or BE). The second bar of the same colour shows the actual disbursements at the end of that financial year (actuals). The difference between ex-ante budget allocation vs actual spending is especially important because the policies have front-loaded the disbursement on an equal footing basis during capital acquisition and construction stages, instead of tying financial support to production. In FY27, the government expects to spend ₹8000 crore (~10 per cent of the total outlay) for the already approved projects under ISM1.0. Breaking down this overall number indicates the health of each sub-scheme.

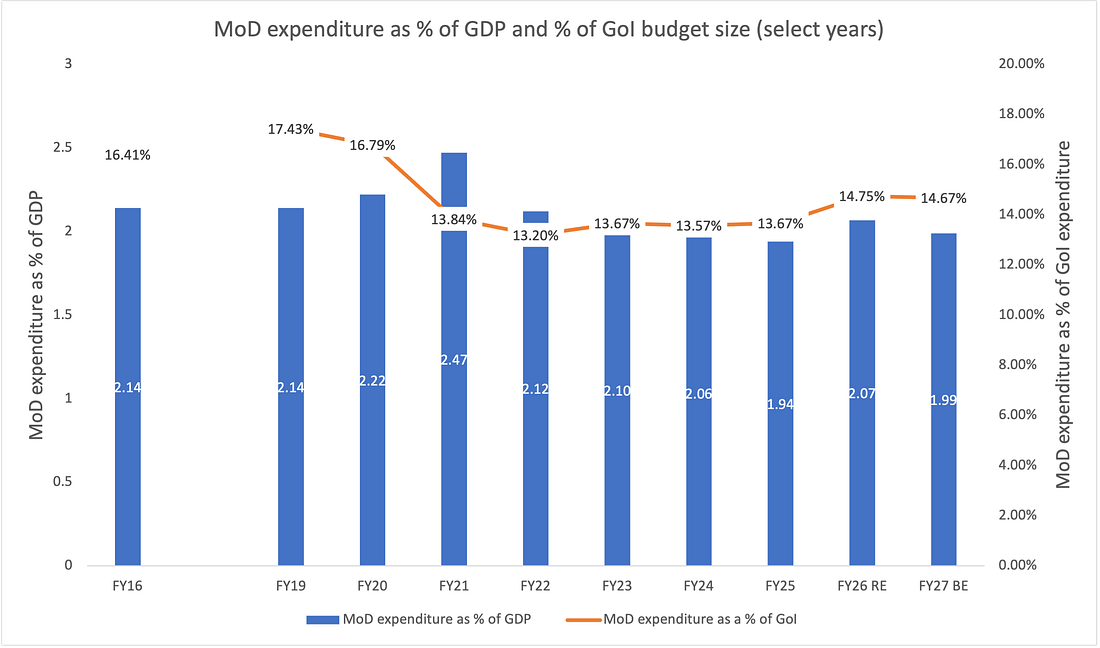

To summarise, India’s semiconductor journey remains a work in progress. The assembly segment shows genuine momentum, but fab construction is behind schedule, SCL Mohali modernisation remains more promise than reality, and the design ecosystem—where India has natural strengths—continues to be let down by poorly designed incentive structures. ISM 2.0’s focus on equipment and materials is strategically sensible, but execution will be key. As with previous years, the gap between announcements and allocations, between budgeted amounts and revised estimates, tells the real story. DefenceBetween the previous budget and the latest one, there was Operation Sindoor. So, you would expect defence capital outlay to rise to account for new purchases. Though the data does show an increase in capital outlay and overall defence spending, there doesn’t seem to be any step jump in terms of procurement plans. The chart below shows defence expenditure as a proportion of GDP and as a proportion of government expenditure. A rise in the former would indicate a move towards rearmament, while a rise in the latter indicates defence being prioritised over other governmental expenses.

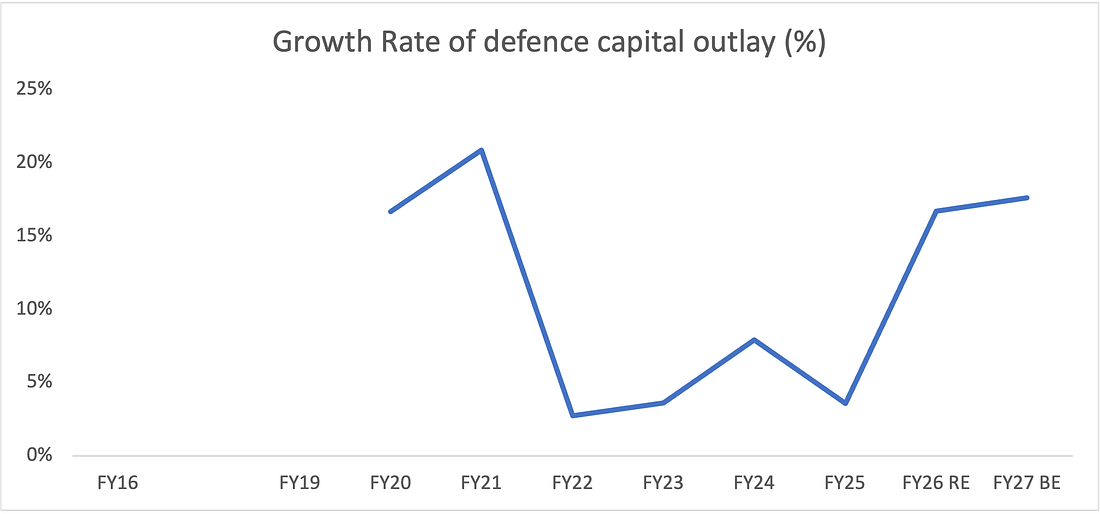

As the chart shows, there is a marginal increase in the defence expenditure as a percentage of GDP over the current financial year, and no substantial change is planned for the next. Defence expenditure as a percentage of total government expenditure does show a hike. The good news is that defence spending on equipment has found its mojo back. Capital outlay now accounts for nearly 28 per cent of total defence spending, up from a low of 23.6 per cent in FY19, back when the spending on defence pensions exceeded the spending on equipment purchases. This is also reflected in year-on-year growth rates of capital outlay as shown below. As a result, we can expect some platform purchase announcements or deliveries in the coming financial year.

HomeWorkReading and listening recommendations on public policy matters

|