Ticker Reports for January 5th

3 Stocks Delivered +10% Buyback Yields in 2025—What's Next in 2026?

Share buybacks are one of the key ways that companies return capital to shareholders. Buybacks do this by reducing a company’s outstanding share count, allowing each remaining share to account for a larger percentage of a company’s value. All else equal, this puts upward pressure on share prices.

They are also often a signal of management confidence. When a company buys back shares, it is essentially investing in itself. Thus, buybacks can indicate that a company believes investors are undervaluing it.

Buyback yield is an important metric for understanding the magnitude of a company’s repurchases. It shows how much a company spent on buybacks over the last 12 months (LTM), relative to its market capitalization. Buyback yield is calculated like this:

(LTM Buybacks – LTM Share Issuance) / Market Capitalization

This metric allows investors to compare buyback spending between companies of different sizes. Below, we’ll detail three S&P 500 stocks that ended 2025 with LTM buyback yields above 10%, among the highest in the index. This analysis will include repurchases made in Q4 2024, as most companies have yet to report Q4 2025.

GM Makes Smart Use of Buybacks as Shares Gain +50%

First up is U.S. automobile stock General Motors (NYSE: GM). The company’s LTM buyback spending was $8.2 billion, and it issued no shares. Ending 2025 with a market capitalization of $76.2 billion, the stock’s LTM buyback yield comes in at 10.8%.

Notably, $4.7 billion worth of the firm’s buyback spending came in Q4 2024. Overall, the stock rose nearly 53% in 2025. Thus, GM purchased a huge number of shares at a significant discount.

The company’s Oct. 21 earnings report greatly impressed investors as GM significantly raised its guidance for the full year. The stock gained 15% that day and has climbed another 22% since.

The consensus price target on GM of $75.76 implies 6% downside in the stock versus the Jan. 2 close. However, targets updated in December average out to $85.50, suggesting that shares could rise 6%.

Buybacks Boost LUV Even as Market Cap Growth Stagnates

Southwest Airlines (NYSE: LUV) was another buyback yield standout. The company’s LTM buyback spending was $2.75 billion and it issued only $60 million worth of shares. Ending 2025 with a market capitalization of $21.4 billion, the stock’s LTM buyback yield stands at 12.6%.

Southwest’s buyback spending peaked in Q2 2025, when it spent $1.5 billion.

The company appeared to act opportunistically in April, as most stocks sold off amid concerns about Liberation Day tariffs, including LUV, which was trading around $24 in late April. Since then, the stock is up nearly 75%.

Notably, Southwest’s market capitalization rose just 6% in 2025. However, the stock rose 23%.

This highlights how buybacks can add value on a per-share basis by reducing a company’s share count.

While the company’s total value changed little, buybacks concentrated that value over a smaller number of shares, helping each one appreciate.

The consensus price target on Southwest of $39.44 implies 4% downside versus the Jan. 2 close. However, the stock received numerous upgrades in December. December price targets average to $42.73, implying 3% upside.

TPR Nearly Doubles in 2025, Spends Almost $3B on Buybacks

Last up is consumer discretionary stock Tapestry (NYSE: TPR). Tapestry owns the handbag brand Coach, which has been driving strong growth for the firm. Overall, Tapestry had an extremely impressive 2025, with shares rising 96%.

Tapestry also bought back shares hand over fist during the last 12 months. In total, the company spent $2.8 billion on buybacks, while issuing around $184 million worth of shares.

Ending 2025 with a market capitalization of $26.1 billion, the stock’s LTM buyback yield was almost exactly 10%.

Tapestry repurchased $2 billion worth of shares in Q4 2024, investing in itself at a favorable time.

The consensus price target on Tapestry of $122 implies 6% downside versus the Jan. 2 close.

However, targets updated after the company’s latest earnings report on Nov. 6 paint a different picture. They average nearly $137, suggesting 6% upside.

Buybacks: An Important Tool if Used Appropriately

Southwest is a good illustration of how buybacks can boost per-share returns. But markets don’t automatically reward repurchases. If investors believe buybacks are crowding out critical investment—like fleet upgrades, technology, or long-term product development—sentiment can turn quickly. Buybacks funded with excessive debt can raise the stakes even more.

The bottom line: buyback yield is a powerful starting point, but it works best when paired with business quality, balance-sheet discipline, and credible reinvestment in the core franchise.

Executive Order 14330: Trump's Biggest Yet

Executive Order 14330: Trump's Biggest Yet

These 3 Stocks Trade at Discounts the Market Won't Ignore Forever

The S&P 500 wrapped up 2025 with a total return of about 18%, the third straight year above historical norms but a lower figure than the gangbusters 25% returns of 2023 and 2024. AI euphoria is still the strongest market trend entering 2026, and the usual suspects like NVIDIA Corp. (NASDAQ: NVDA) and Alphabet Inc. (NASDAQ: GOOGL) are up once again on the first day of trading. If you’ve ridden the AI rally since the market bottomed in 2022, you’re likely sitting on substantial gains and may feel compelled to diversify, especially if you have a tech-heavy allocation.

The S&P 500 is entering the year trading at 26x forward earnings, a stark elevation above its 20-year average of 16x forward earnings. When valuations are this elevated, investors become ravenous for earnings growth, and high-multiple stocks can fall out of favor quickly if growth slows even a little. And if rates remain high, 2026 could be the year value investing makes a comeback.

Today, we’ll look at ways to de-risk a portfolio by investing in stocks that enter the new year undervalued and overlooked. Each company discussed here trades at a substantial valuation discount to its industry average, but fundamental and technical tailwinds suggest this discount may not persist for much longer.

Comcast: Strong Balance Sheet and Sports Expansion Enhance Outlook

The Comcast Corp. (NASDAQ: CMCSA) was one of the biggest victims of the cord-cutting revolution, as customers fled expensive cable packages for a la carte streaming services.

A lost decade is always an investor’s worst nightmare, and CMCSA is about five months from completing this dreaded milestone, trading at about the same price it was in May 2016.

But now, customers are getting cord-cutting fatigue; streamers are raising prices and getting into costly disputes with major networks.

Meanwhile, Comcast has quietly built a sturdy balance sheet with a variety of revenue streams and its forward price-to-earnings (P/E) ratio of 6.84 is well below both the communications industry average (16.5) and that of major competitors like The Walt Disney Co. (NYSE: DIS) and AT&T Inc. (NYSE: T).

Comcast’s broadband business is a steady, high-margin cashflow machine. Despite Connectivity and Platforms revenue slowing 1.4% year-over-year (YOY) in Q3 2025, the EBITDA margins of the residential and business segments were 37% and 56% respectively. The advertising business also expects a boost in 2026 as NBCUniversal has the rights to Super Bowl LX, the FIFA World Cup, and the Winter Olympics in Italy.

The company generated $4.9 billion in free cash flow in Q3 as well, continuing to support its 4.4% dividend efficiently. Comcast’s value story might not be a secret much longer as the stock is up nearly 10% in the last 30 days, and some technical signals are hinting at further upside ahead.

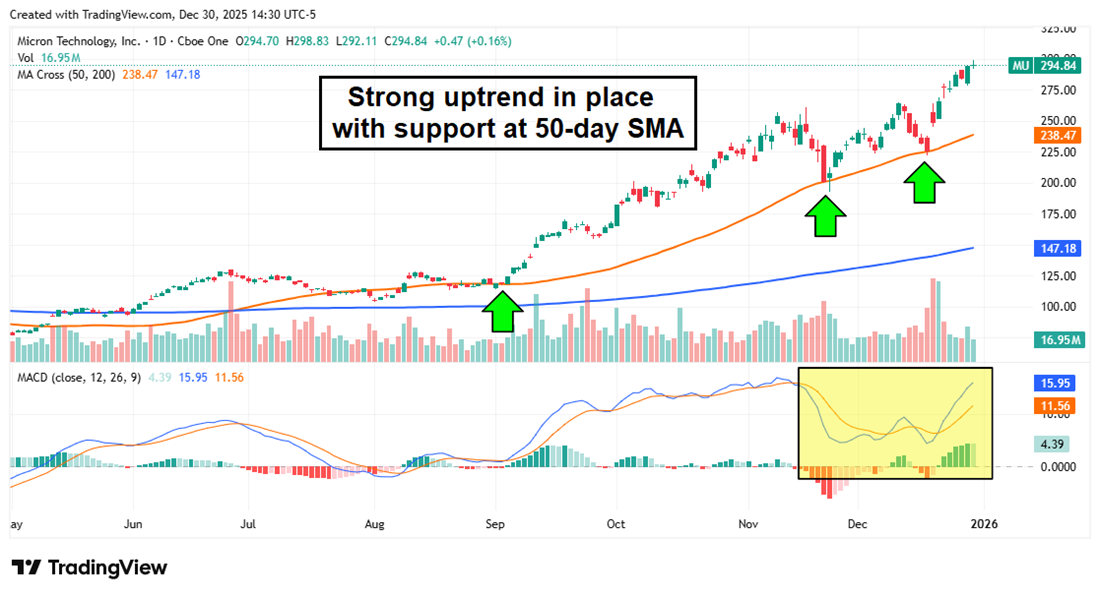

Micron: An Essential AI Stock Trading at a Deep Discount

How can a stock that just wrapped up a 200% year still be undervalued?

Despite its parabolic 2025, Micron Technology Inc. (NASDAQ: MU) remains one of the more undervalued players in the AI industry, trading at 29x earnings while the tech sector sits at close to 75x earnings.

A P/E ratio of 29 isn’t exactly cheap compared to the rest of the broader market.

Still, it's a great deal for a company generating 57% YOY quarterly revenue growth, 57% gross margins, and boosting guidance projections every conference call.

Memory stocks are high-margin businesses, and Micron management has stated it is struggling to keep up with insatiable demand from data centers. The chart shows a healthy stock in a strong uptrend, with support along the 50-day simple moving average (SMA). This matches the TradeSmith Health indicator, a new feature that measures a trend's viability. In this case, MU shares are in the Green Zone, which indicates a strong uptrend with healthy pullbacks.

Pfizer: Fueling Pipeline Innovation Through Acquisitions

Shares of healthcare giant Pfizer Inc. (NYSE: PFE) have struggled now that the COVID-19 pandemic is in the rearview mirror; the stock is down more than 30% over the last five years.

Competitors like Eli Lilly and Co. (NYSE: LLY) have soared past PFE thanks to obesity drugs like Mounjaro, but now Pfizer is trading near historical lows in valuation (8.4x forward earnings) and is far cheaper than most large-cap peers in the pharmaceutical sector.

The company’s Seagen acquisition is also beginning to pay dividends in the oncology division, adding more than $6 billion in revenue since the deal closed in 2023.

Despite a slow pivot into the growing obesity drug market, Pfizer now has a strong pipeline there as well, acquiring two smaller drugmakers with oral and injectable treatment options. The market has basically left Pfizer for dead in this space, hence the vast valuation gap. But low expectations often create opportunities; the stock hasn’t priced in Pfizer making successful inroads into the GLP-1 market. Additionally, Pfizer makes an excellent defensive investment thanks to its cheap valuation and history of dividend growth.

Best $19 you'll spend this year.

Best $19 you'll spend this year.

These 3 Turnaround Contenders Could Be Set for a Big 2026 Break

2026 could be a breakout year for several companies that have previously spent time patiently rebuilding or preparing. Years of headwinds related to reduced demand, pandemic travel disruptions, delayed launches and other factors have threatened the companies below in their ability to maximize their capital appreciation and appeal to investors.

These turnaround contenders—some of which have already performed quite well in recent quarters, despite the challenges—could deliver in an even bigger way this year if the circumstances are favorable.

Post-Pandemic Return to Travel Demand and Spending Trends Could Boost Royal Caribbean

Like all cruise companies, Royal Caribbean Cruises (NYSE: RCL) was once hit very hard by COVID-related travel stoppages and depressed demand. However, in recent years, Royal Caribbean experienced the return of healthier demand, with shares climbing by about 275% in the last five years. Driving this share growth is an increase in bookings, which for the latest reported quarter grew year-over-year (YOY) at "the high end of historical ranges," according to management.

Key to Royal Caribbean's continued turnaround success in 2026 will be sustained consumer spending, not only in terms of cruise bookings overall but in on-board purchases, which have also climbed in recent years. This will depend, of course, on consumer sentiment more broadly, which has struggled in the face of economic uncertainty. It will also depend on interest from younger spenders—in this way, Millennial and Gen Z travelers prioritizing experiences over traditional large purchases like homes may continue to drive Royal Caribbean's growth.

So far, it appears Royal Caribbean is on track for just this type of growth. The company boosted its full-year 2025 guidance for adjusted earnings per share (EPS) to a range of $15.58 to $15.63, up about a third YOY. Near-term operating cash flow should reach a healthy $6 billion, according to management, although higher tax and fuel costs could dampen this.

After reinstating its pandemic-paused dividend in 2024, Royal Caribbean now pays a yield of 1.44%, which may be another reason why 20 analysts are optimistic about its prospects going forward and why the firm has expected upside potential of almost 15%.

Take-Two’s Next Blockbuster Could Drive Strong Growth Into 2026

Take-Two Interactive Software (NASDAQ: TTWO) is one of a small number of pure-play video game companies available to investors. The industry has experienced turbulence in the last several quarters, including a right-sizing that many firms completed after expanding too quickly amid pandemic-related demand boosts and a series of major acquisitions and consolidations. Take-Two has managed to navigate these headwinds fairly well, despite questions about game release timing and is now expected to continue its recent trend of strong net bookings growth.

In its fiscal second quarter, ended in September 2025, the company saw record second-quarter net bookings close to $2 billion and raised guidance to a range of $6.4 to $6.5 billion. The firm's revenue mix is also improving thanks to recurring consumer spending on live services and strong performance from its NBA 2K franchise.

The reason why 2026 could be pivotal for Take-Two, however, is due to its latest offering in the popular Grand Theft Auto (GTA) franchise. Despite delays, the release of GTA VI is still expected in November 2026 and is widely anticipated among both players and investors. If GTA VI matches or exceeds these expectations, it could boost both live-service revenue and upfront sales, improving Take-Two's margins and continuing the growing booking trend.

Improving Fundamentals Could Drive Resurgence in ABNB Shares, But Caution Is Warranted

Shares of short-term lodging marketplace Airbnb Inc. (NASDAQ: ABNB) had a tumultuous 2025 as the company navigated shifting regulations in some of its major city hubs, external pressures on travel habits, and concerns about brand trust. The company ended 2025 with shares up only about 3% for the year. However, despite a recent miss on EPS predictions in its latest quarterly report, 10% YOY revenue growth and record adjusted EBITDA alongside a healthy $1.3 billion in free cash flow point to fundamental strength.

Airbnb could see a turnaround in 2026 as it invests in new ventures to strategically expand its operations, including through bundled services that could increase revenue potential beyond its traditional lodging offerings. Analysts project almost 16% in earnings growth for the year and continued modest upside potential of around 6%, although they are generally cautious about ABNB share ratings. ABNB may be worth a closer look for investors willing to accept a greater degree of risk in the new year.

How the Rich Retire

How the Rich Retire

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.