To my readers: this edition of the Hale China Report was sent to EconVue+ subscribers on September 19th. I’ve removed the paywall, so now the full post is shareable if you have friends with an interest in China’s economy. To receive my upcoming China reports as they are published, please consider becoming a paid subscriber. The topic of the next edition-China & Energy. Thank you! Diplomacy is BackOver the weekend, and unannounced, National Security Advisor Jake Sullivan and China’s Foreign Minister Wang Yi met in Malta. The official US readout is here:

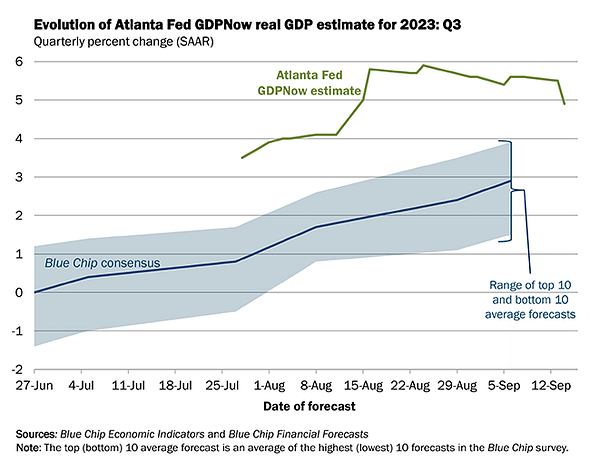

Speculation was that this was preparation for a possible Xi-Biden Summit at the APEC meeting in San Francisco in November. This week Sullivan and Secretary of State Antony Blinken both met with China’s Vice President Han Zheng on the sidelines of the UN General Assembly meetings in New York, providing additional momentum for a summit. Wang Yi will now visit Washington next month, becoming the highest ranking Chinese official to visit the capital since the pandemic began. Following on Secretary of Commerce Gina Raimondo’s successful visit to Beijing, this is all good news, signifying that critical communications channels are functioning. However serious challenges remain for both Xi and Biden. Biden’s weak polling and Xi’s unexpected cabinet shifts mean both sides might not be negotiating from positions of domestic strength. The official revelation that the balloon shootout that scuttled Blinken’s trip to Beijing earlier this year was in fact a false alarm is another signal that tensions have eased. What is fueling US-China diplomatic rapprochement? Economic Growth in the US and ChinaI think the answer is simple. The Chinese economy is not recovering as rapidly as was expected, while prospects for the US economy seem to be improving. Chinese consumers are exhibiting a different behavior pattern than American consumers post-Covid. China’s “Dual Circulation” is not working and dependence on exports has risen. “Common Prosperity” has come to mean less prosperity for everyone. Lack of Chinese consumer confidence could mean that US GDP growth could exceed China’s this quarter. The Atlanta Fed Nowcast on September 14th estimates 3rd quarter US GDP growth at 4.9%. China’s 2023 target is an optimistic 5%.

The US and China face shadow banking risks and are likely to hold interest rates steady this month. Higher oil prices could depress growth in both countries. External Risks & Market DynamicsWhile the dollar is seeing continued strength, the People’s Bank of China is struggling to keep the yuan from weakening beyond 7.3 to the dollar. Amid capital flight currency traders will be watching to see if intervention continues, or if the PBOC is merely shadowboxing to imply that devaluation is unwelcome. A weaker yuan would be a boost to Chinese exports, but China wants to avoid being called a currency manipulator. Chinese equity markets also appear to have government support, even if it only amounts to jawboning. Chinese policymakers realize that they need to revive foreign direct investment, but on balance, government policy intervention has made it tough to invest in China while at the same time making it tough to short. The likely scenario is that the Chinese economy will muddle along within policy guardrails and is why I believe that forecasts of an imminent economic collapse are overdone. However, if one large economy, for example China or Japan, or even a smaller trading partner suddenly and steeply devalues, we could see a wave of competitive devaluation and a race to the bottom, similar to what happened during the Asian Financial Crisis of 1998. All Asian economies are much more intertwined, especially with China, than they were 25 years ago. So the effects could be far worse. China’s relations with Europe seem to be deteriorating. The EU will take action against Chinese electric vehicle makers, claiming that state subsidies amount to dumping. But contradictions, even within the same industry emerge. Ironically, the Volkswagen plant in Portugal, deprived of parts due to flooding in Slovenia, were able to restart manufacturing due to the intervention of a Chinese supplier. Thus providing a perfect illustration of how global supply chains are still fragile. Domestic ChallengesThe property bust cannot be analyzed on a standalone basis. One thing that China needs to get right is local taxation to support local institutions so that local bureaucracies do not become real estate investors or investment houses— which is just what has happened. The implementation of local property taxes on a nationwide basis would be the single most bullish signal I can imagine. Despite some failures, most have not yet lost faith in local banks and trusts, causing Chinese savers to move their money to state banks en masse. As is the case in the US, local lending is critical to dynamism and new business formation, which has fallen off a cliff in China. Root CausesChina is now groaning under the increased burdens of anti-corruption campaigns within its complex economy, inextricably tied to the global macro environment. Entire sectors such as healthcare are at a standstill. Policy chokepoints have proliferated throughout the economy. Corruption is not about ethics in a system that cannot function if the rules are obeyed. It is about inadequate institutions. In other words, when everyone is corrupt, no one is corrupt, and inevitable and universal infractions merely present an opportunity to punish political opponents. However, the rub is that the policy effects are now global not just local, in an interlinked financial system with multinational companies operating across borders. As some observers watch China stumble, they seize upon the failures of communism, or authoritarianism. In my view, China’s current difficulties are not caused by its system of government, which after all existed during China’s great economic boom. Instead they are the result of institutional weaknesses that were masked during a period of high growth as reforms were unfortunately delayed. Critical developmental windows were missed, as detailed in a new IMF working paper, Fiscal Policy and the Government Balance Sheet in China:

Geopolitical ImplicationsDo these economic woes mean that China’s leadership will use economic weakness as an excuse for example, to attack Taiwan? I don’t think so. MIT’s M. Taylor Fravel discusses this possibility, The Myth of Chinese Diversionary War in this month’s Foreign Affairs:

Internal Political DynamicsI take this rather contrarian view one step further. I doubt that the sackings, or rather the disappearances of Defense Minister Li Shangfu, as well as the Rocket generals and probably many others we don’t know about, are directly related to Taiwan. In China’s return to a personality-driven political environment, personnel changes are more probably about loyalty to the current regime. It is more likely that Xi Jinping took these actions to command internal discipline and bolster his own security. His personal safety might also be a factor in decisions about his sparse international travel schedule. Will China Turn Inward Once Again?All of which brings up an under-appreciated risk. Recent reports by the few travelers who visit China say that it is virtually impossible to access the Internet outside the country now. An economic policy that focuses on self-sufficiency reminiscent of Mao also points to China closing itself off to the world. Will it do so in the dramatic way that is has during its history? If so, Chinese passivity could play a bigger part in slowing global growth than the aggression feared in Washington. And in my view, it is also much more probable. Putting the Puzzle TogetherIn order to assess the risks that China poses to global growth, it is critical to understand the interplay of factors in the evolution of its domestic economy. Lack of institutional reform, whose consequences were once confined within China’s own borders, can now impact markets and industry sectors around the world, from commodities to currencies to technology. Although recent diplomatic overtures are positive, leadership changes in both the US and China could play unexpected roles, affecting the health of both the global economy and peaceful geopolitics. It is essential for stakeholders to understand the dynamics of the situation in China today, in order to build a more effective and constructive relationship. This is better approach than saying, as President Biden did last month, that China is a ticking time bomb waiting to lash out. Fravel ends his Foreign Affairs piece with a proviso:

Hopefully, the Xi-Biden Summit in November can set a new tone for the relationship between the world’s two largest economies that will benefit rather than hamper global growth. Invite your friends and earn rewardsIf you enjoy econVue + , share it with your friends and earn rewards when they subscribe.

|