|

Editor's Note: Louis Navellier has been managing money for over forty years now. In that time, he's met U.S. presidents... been profiled by the New York Times, Barron's, and Forbes... and recommended over 675 stocks that went up 100% or more. Now he's staking $358 million of his own firm's money in an AI phenomenon with world-changing potential. Click here to find out why he's going "all-in" on this 70X boom... Dear Reader, Elon Musk has built the most powerful AI supercomputer in the world... Partnered with the Department of Defense, Oracle, and Palantir... And created a breakthrough that could make ChatGPT obsolete (click here for the live demo). But here's the catch... If you want to invest in Elon's game-changing AI company, you're probably out of luck. Unless you run a major tech company... A venture capital firm... Or a sovereign wealth fund... You're stuck on the sidelines – watching the rich get richer. By the time this firm goes public, it'll be too late to see any serious gains. But I just sat down with $1 billion fund manager Louis Navellier... The 47-year Wall Street legend who's been profiled by the New York Times, Barron's, and Forbes... met U.S. Presidents Trump and Reagan... and recommended over 675 stocks that went up as high as 100% or more. And he's found something extraordinary... A way to potentially profit from Elon's AI lab ahead of its rapidly approaching IPO day (Elon just filed the confidential paperwork). And — to prove it — he's put $358 million of his own firm's money on the line. It's an extreme vote of confidence in perhaps the biggest opportunity to create generational wealth this decade. Click here for the full details... Regards, John Burke Host, InvestorPlace P.S. Goldman Sachs predicts that this technology could soar an extraordinary 70X in the next ten years. But if you want to profit from it, you must move quickly. Elon is quietly putting the finishing touches on an AI breakthrough that could accelerate this megatrend in a major way. Get the full story here.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. Today’s editorial pick for you A Hantavirus Outbreak Boosting Moderna (MRNA) Stock? Don’t Bet on It.Posted On May 13, 2026 by Joshua Enomoto

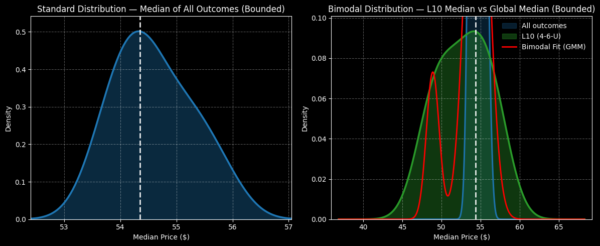

With lingering memories of COVID-19 still in the air, it’s only natural that the latest hantavirus scare is accelerating positive sentiments for Moderna (NASDAQ: MRNA). On Friday, MRNA stock jumped nearly 12% on hantavirus vaccine research. That brings the security up over 84% on a year-to-date basis. While it’s tempting to jump on the Moderna bandwagon, considering the COVID catalyst, traders will want to exercise healthy skepticism. Table of ContentsTo be clear, I’m not suggesting that Moderna is an irrelevant pharmaceutical enterprise. Far from it, the company enjoys several promising therapeutic pipelines. However, I believe it would be a mistake to bid up the mRNA stock simply on the basis of the hantavirus. When looking at the facts, a mismatch exists between the fear of the virus and the probabilistic risks to the general public. According to the UN World Health Organization (WHO), the risk of hantavirus spread to the general population is “absolutely low.” Indeed, the threat is a nuanced argument. While the virus has a high mortality rate, the risk of exposure to the average person is extremely limited, in part because of transmission difficulty. The Andes strain that’s in question here requires very close, prolonged contact to jump between people. In other words, unless you are cleaning out a long-abandoned shed or going on a birding expedition in rural Argentina, your exposure risk is negligible. Better yet, one of the best ways people can help prevent infection is to address rodent infestations. Basic cleanliness and hygiene — along with other common-sense practices — can go a very long way. That also segues into another concern about buying MRNA stock simply on the basis of a possible hantavirus outbreak — the convenience factor. Because the transmission risk is low to begin with, the preventative measures are convenient. Generally speaking, getting pricked with needles isn’t an enjoyable experience. Therefore, a vaccine may be considered an overkill solution. Bid Up MRNA Stock? ‘No Thanks’ Says the Smart MoneyObviously, no one knows for sure what the future may hold regarding potential public health crises. And given the fiasco of the global COVID-19 response, it’s understandable that many people are skeptical about the assertions coming from even respected health agencies. That said, it’s interesting that the smart money isn’t biting on Moderna stock. How do I know? When looking at the volatility skew for the June 18 expiration date, the positioning of implied volatility (IV) readings across the strike price spectrum tells the tale. From the current spot price to the right end of the axis, IV for call options rises in an almost linear fashion. Basically, bullish traders are paying a higher premium than they would be under normal circumstances. Fundamentally, we’re talking about simple economics here: there’s more demand for call options and thus call sellers are more than happy to collect the exaggerated premium. However, these call sellers are most likely covered call sellers by institutional investors who are long MRNA stock. They believe in Moderna but not in the hantavirus hype. Subsequently, the smart money is using the premiums to buy protective puts on MRNA stock. You’ll notice that in the volatility skew for June 18, put IV stands above the equivalent call IV. Technically, this dynamic usually occurs when a security is hard to borrow or when there is a high cost of carry. In my assessment, these sophisticated traders are betting that the hanta hype will fade. It’s also worth pointing out that the put skew for strike prices right below the spot is extremely flat, with the skew only rising sharply on the extremely low end. While it’s impossible to make absolute pronouncements about trader sentiments, this chart signals that the smart money likely doesn’t believe MRNA stock is going to collapse. Sure, the far out-the-money (OTM) puts are in place in case stuff happens. But the most likely outcome — at least what the institutional folks are showing — is that MRNA stock will soon revert to the mean. Avoiding the CrowdOf course, the temptation right now is to buy Moderna stock, especially with how MRNA performed during the height of the COVID pandemic. However, the quantitative landscape doesn’t really look that appetizing for the bulls. Using a dataset going back to January 2019, the odds that a random 10-week long position in MRNA stock will be profitable are 53.3%. That’s decent, but the aggregate reward would likely be limited. Under random conditions, you’d expect MRNA to land between $52 and $57 (assuming a starting price of $54.35). It’s a bit better than a coin toss, but not by much. However, when isolating MRNA stock to its current quant signal, the projected outcome delivers a mixed inductive view. In the last 10 weeks, MRNA printed only four up weeks, but with an upward slope. This contrarian signal statistically improves the exceedance ratio to 66.7%, but there’s a major catch.

Under 4-6-U conditions, the forward 10-week distribution of Moderna stock would be expected to range between $40 and $65. However, the bulk of the distribution sits south of the current spot price — and that’s because during the middle portion of the period, MRNA tends to tumble. It’s only in the latter weeks does MRNA pop higher. Now, we are talking about an inductive observation, meaning that it’s not logically determined that Moderna stock will follow past observed pathways. However, it’s risky to go rogue against the data when the smart money is also hedging for a pullback. If I had to guess what a viable debit-based trade might be, I’d probably only stretch as far as the 50/48 bear put spread. Actual trading data shows that there would likely be a high concentration of activity around the $48 and $49 price range. However, the maximum payout for this bear spread only tops out at 72.41%. Personally, I don’t like the risk-reward proposition, and I would really wait for a more confidence-inspiring signal if I’m on the debit side. On the credit side, there’s too much risk of the public money doing “stupid stuff” that could result in unpredictable behavior for MRNA stock. Yeah, I hate writing wishy-washy articles like this, but for Moderna, the easy money may have already been made. Likely the best idea right now is to avoid taking the bait. This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe. StockEarnings, Inc |